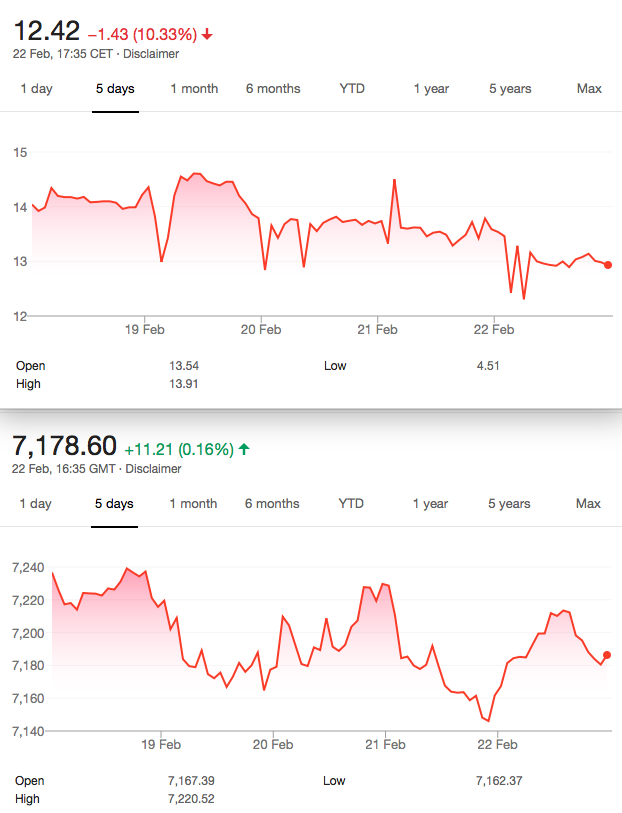

FTSE down a miserly 58 points on the week, as vol drops big time.

That Was The Week

So….nothing troubling, just another uppy downy week in the face of so much impending chaos. As per usual I get a great deal of emails but here’s something that challenged my ideas and bias:

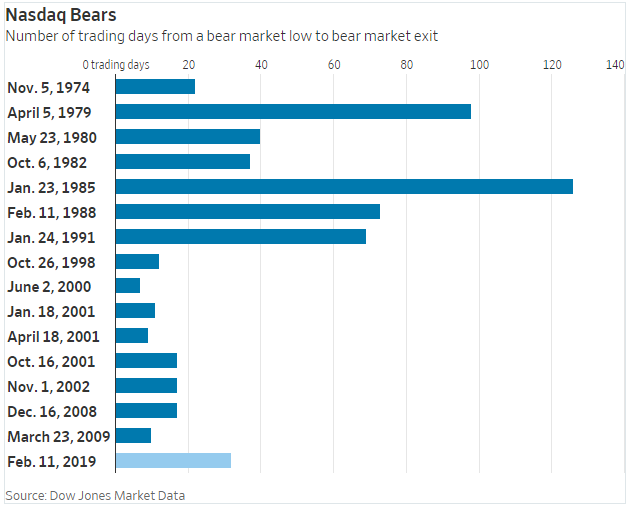

I Also noted this:

I Also noted this:

What does this mean? Simply that when the market-and I use Nasdaq as a proxy, drops 20% the time it takes to recover is measured in a modest number of days. I say ‘recover’ but it’s only a rise of 20% from the low-so we are still 10% off the all time high. We note the chart describes a ‘V‘ bottom this is when we, the nasty put owners have made the big bucks. Fund managers then allocate the new money. We are assuming they are still solvent! Us traders can easily get caught up with the doom and gloom. It’s worth bearing in mind the strength of these rebounds.

Chartists or ‘technical analysts’ often come in for some stick, but the graphic is a great aid to trading. Personally I like numbers and a chart. As a watcher of VIX/VFTSE, volatility is the big number for me. You know by now-the golden rule that you never buy high volatility. Readers here know we do not just sell as vol is high. Some insurance though is always a smart idea. Naked is what we do in a private pool or beach.

Trade 120 Getting close To the ‘B’ Word

Here’s how the current positions are doing:

Trade 118– we are looking at (again not my favourite) an Iron Condor. We were selling a 6750/6700 put spread and selling a 7300/7350 call spread for a total credit of 6.5+7.5=14. Currently 11

Trade119, the call butterfly giving 100 point wide strikes would be 7150=123, 7250= 70, 7350 =35. The maths 123+35-(70×2)= 18. Currently 23.5

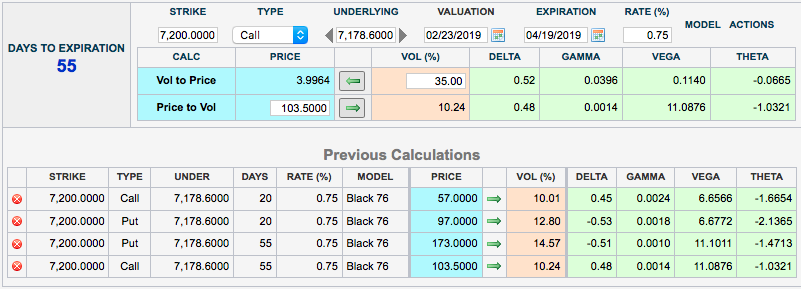

Trade 120 – I need some inspiration, but caution has to be the watchword. I want to be long both puts and calls after 29th March. Until then I think we are virtually moribund, as news does not seem to be much of a mover. Yet again there is political upheaval and the market says “So what?” Which brings me to: Mar/Apr calendar straddle, but not a ratio. This is one for one.

What can this mean? We are selling the 7200 put and call in March and buying the 7200 put and call in April.

Logic of the trade:

We want to own a straddle but want it at a discount. ( 276- 154)= 122 debit.Theta tells us we are 1.3205 better off daily thanks to Theta. We are assuming the FTSE goes nowhere much. We hope the March straddle expires in 20 days for a lot less money than its current 154. However this trade is expensive, and risk is that a big move wipes out much of the difference in premiums, should FTSE go to say 7450 or 6800.

We’d be nursing a loss around 50. That sort of debit could buy us a nice couple of spreads- calls or puts.

We Need To Show A Trade Weekly

Gun to head time- I have no good ideas relating to Brexit but I think we need some long option positions, and if there is a volatility explosion, we will clean up. My problem is £sterling. It could go to parity with the US$, or to 1.5.

What we have each week is a simple, digestible approach, managing risk. Thus showing the difference between trading as a business, and investing for the long term. Happy to be challenged on any content, and hope we all have the good sense to say “We do not know where our risk is, so we’ll sit on our hands” Price Headly reckons he’s made as much money doing precisely that.

Note: Please look at theta in context– the other Greeks are highly relevant-we are positive delta, negative gamma and vega.