[see bottom of page if you are a newcomer here, 300+ trades in, we foolishly assume everyone is up to speed]

That Was The Week. A Real Shocker!

I have often expressed the view that markets rise on ‘untruths’ as regulars here will know. ‘Gut’* told me that long trades were not going to do well, and Wednesday evening I had honestly forgotten to message, so Thursday morning at 08:27 I stated my concerns and advised closing out of at least one of the trades. Now this all looks pretty much like standard BS but I do not claim to be that proactive trader. What we do here is educational, and trading with a reason for the trade is how we select. It is not possible to keep up the stream of constant winners, though it’s nice to show how anyone can do this.

Had we stuck to the knitting with the nutty 306 straddle dilemma, we’d have been super happy. Remember that trade benefits from owning 2 straddles versus selling one, so big moves make £££. Correctly placed this is always long x2 the near month short x 1 the far month.

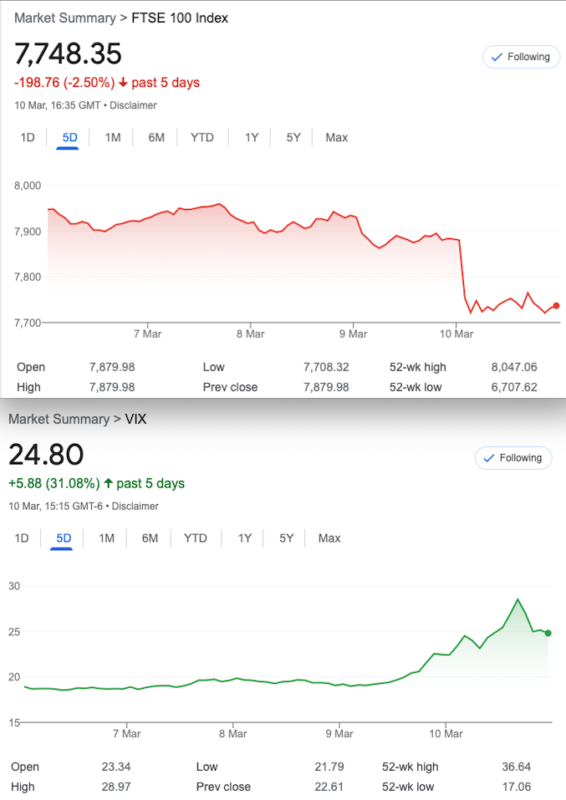

Failure of SVB- Another New Paradigm.

I have mentioned before that I feel constantly lagging behind the market by a month(or maybe ahead 11 months!). This left field event was no great surprise and, there is always smarter money than the mainstreamhttps://blog.argonautcapital.co.uk/articles/2023/03/10/silicon-rupture/ For all those who think shorting a stock is evil, it’s an absolute necessity. This is how people can be kept honest, eventually. When it’s too good to be true………

In other news, why did other banks plummet? You’d think if they have nothing to hide, they’d simply shrug off the failure of a large, but niche bank.

*Oh wait- here was the canary in the coal mine: https://uk.investing.com/news/stock-market-news/credit-suisse-shares-hit-new-alltime-low-as-banks-hit-by-us-fallout-2945589 When it became Debit Swizz!

Distraction Trades- How did We Do?

ADA $0.3058 Doldrums- not just a piece of ocean.

XRP $0.3616 Looking more healthy and some chatter about Ripple in the financial media.

DAX 3 no entries 1 win +80 1 loser -30 All that turmoil but DAX was benign and our system did not capture the juicy stuff.

Legacy Trades 304 – 306 and 307

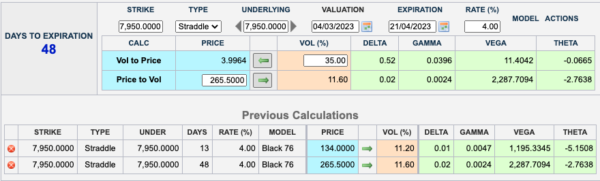

Trade 304 Starting with a Debit of 160

We are told there’s no downside hourly daily or monthly. Let’s put that to the test. We will sell for 173 the March 8100 put. As a little insurance we will also, have a call ratio spread 7800/7950 for cost of 215- 107.5×2 = 0

This is breaking some new ground and we will be in a bit of a pickle if the FTSE takes off upside again, but we have taken in the big premium from the 8100 put. This may need some adjustment but if we don’t break stuff, to quote Mr Musk, we’re not trying hard enough.

Last week we saw this:

Where are we now?

Where are we now?

So, no change- they say it’s a buy on a monthly basis,on a TA basis.

Last Week: 8100 put was 242 ouch! However some mitigation from our call ratio spread which was 144.5- (57.5×2)= 29.5 in credit.

This Week 166.5 for the put, and that call ratio 171.5 and 64.5×2 =42.5 Credit – Overall position thus 124

Adjustments? Monday we buy back the put for 196.5. Tuesday we sell it for 246.5 reducing our deficit by 50 (Easy in retrospect, but I will try to update in real time) However our liability drops to 74

SEE MY MESSAGE:Aaaaaah Dammit. Last night I was reviewing the day’s action and thought it was time to close out, but at the screen late! – the 8100 put was 178 and the call ratio was 65, cost 113 and a clean slate for a drop.

Our trade if we’d used the adjustment from the previous Monday we’d be peachy.

Trade 305 30 days to Expiry When Theta is our Ally [not 30 days, but 23 as mentioned]

We are again in the sweet spot of theta, the edge that makes this idiot look moderately impressive! We therefore need to sell more options than we buy. Let’s get spicy with a short iron condor. We BUY the body and sell the wings. Here, our body is the 7900 straddle, the wings: the 8000 call and 7750 put. BUT we do a ratio, by selling twice as many wings. This means we pay 82 and 110 for the body, and we receive(x2) 38 and 59.5 for the wings= 195. This gives us a tiny credit of 3. Risk is at 7600 and 8100

Those prices now: 95 and 40×2 for the calls 50 and 20×2 for the puts Giving us a credit of 15+10= 25

We run this again but note we have a healthy profit

Despite themassive drop this is still in profit as the 7900 straddle is 189.5, the 8000 call 3 the 7750 put 78.5. Gives us 189.5-(3+78.5)x2 =26.5

306 Straddle Dilemma

So it’s almost exactly half price to buy the near month(March expiry) straddle(put and call at same strike) compared to April. Should we be headed for serious moves and an uplift in volatility, we’d be buying 2 of the March and selling 1 April straddle. I see too much theta for one thing. I also don’t expect a mighty downside move which we’d need. We need to be on the right side of this so we will cautiously sell 2 March straddles, and buy 1 April.

Murphy’s law of options states: When using theta as the sole reason for the trade, it may come back to bite ones rear end!

LOL!!!!! 305 for the April straddle and 230×2 for the March.155 loss if we’d taken the perverse route reliant solely on theta. See the above statement- if selling it on Friday it came back to bite yer bum big! However, we talked about the massive time decay and if closing out on Wednesday(when yours truly got a ‘GUT’ feeling about the impending drop) You’d have made 237-211=26

Let’s get even crazier and see what happens when we run this to expiry. We are back in the Wild West.

307 Big Vol Short Time as Expiry Looms.

A relatively safe play. A one for one calendar spread as near month vol is not too rubbish for once. Reasons for the trade? Vol does not tend to linger -see the hourly chart

April : 7900 put 227 and March 7900 put 179.5 our cost: 47.5

OK I will level with you. Many years ago a hedge fund trader told me to look at Bollinger bands on VIX. https://uk.investing.com/indices/volatility-s-p-500-advanced-chart Can you imagine just trading on this one piece of the picture? Well you could argue that when it’s bumping along the bottom you take a long VIX position with a far dated call spread, which would be cheap to buy and fun a joy to sell!

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com