That Was The Week, FTSE Went Nowhere

How often do we see week after week that the market went nowhere? In a pandemic? Thus, this trader thinks it’s still a lucky dip/lottery/ shooting gallery at the funfair. However, Stockcharts.com made these 2 free videos that are of interest to anyone who trades and needs some light relief: https://www.youtube.com/watch?v=aHjkrKFzXq8&list=WL&index=2&t=0s

Whilst this trader still ranks as a total outsider, I think it’s fascinating to see the workings of the financial world. Meanwhile, back to the matter in hand, and some ‘insights’. Off piste there? Yeah something to do with lockdown….

Futures and Options-Why?

We understand that for practical reasons many options are priced against futures, so why trade the future? Stay with me on this, and observe:

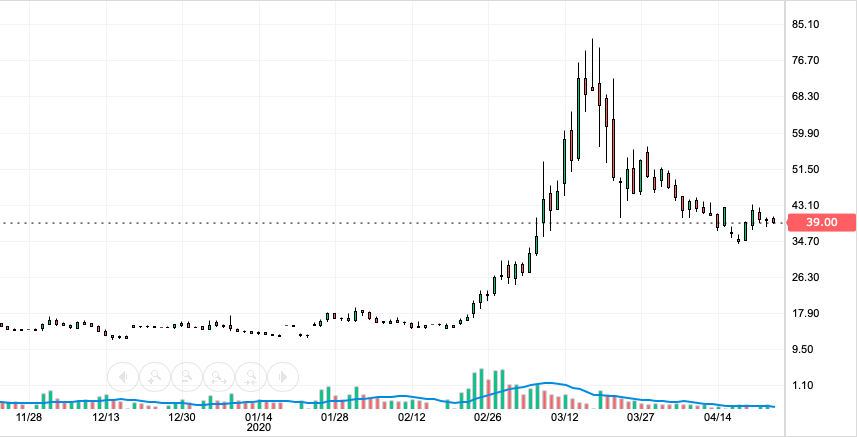

I hope you can see the surge in volume of the VIX futures starting around 21st February. This precedes slightly the catastrophic plummet. Those traders saw the future, so to speak. However while nicely doubling or trebling their money, why didn’t they just buy some puts? I speak not from a position of knowledge here and we cannot know the reasons why, but you could at that time have bought a ftse 7000 put for £150 and collected £20,000 in short order. So, why risk $1000 to get maybe $3,000,when you could get so much more gearing with options? Honestly, this trader has no idea, but I hope it’s made you think about directional 1 for 1 trading. We have our own FTSE futures to trade at £10 a point and one contract used to require about £3,500 in margin.

Hedging Your Bets

My personal take is that we should not look for a hedge in another instrument as they move differently from options. My biggest blunder with hedging with futures, was holding on too long to the hedge while the options trade went right! Hedging is imperfect and it’s only in the options world where you may trade something like a butterfly. Positions thus are 100% hedged and we can only lose our stake. We showed in the last few butterflies that overall they can be highly effective in a dodgy market. Dumb trader that I am I was way too bearish. Doom and gloom are my ying and yang! (apologies yin, not ying)

Traders, we must be trusting our own judgement when basing it on the best information, as that is all we have. Judgements made by yours truly are often ok, rarely followed up in reality. Traders develop fear of missing out (FOMO) and this becomes a big issue. This trader remains sidelined currently and paper trading is a tough discipline. Weekly trades here are aimed at being winners, but that is not always the basis for our trading. Education is the goal and most valuable asset, the track record very much secondary.

Legacy Lunacy

Trade 0.6 The 3×1 call ratio spread. 5800 184.5 6000 (96 x3)= 288. Credit 103.5

Could have closed out for 56 on Tuesday or hung on for: 142, – (62×3)= 44. So we had a credit of 103.5-44=59.5. We’d have taken Tuesday’s 56 credit.

Trade 0.7

3 weeks to expiry putting us in the ‘grey zone’ which is a pain. Planning in this arena means having a view on market direction and relative pricing, plus an idea of how long the trade should be running.

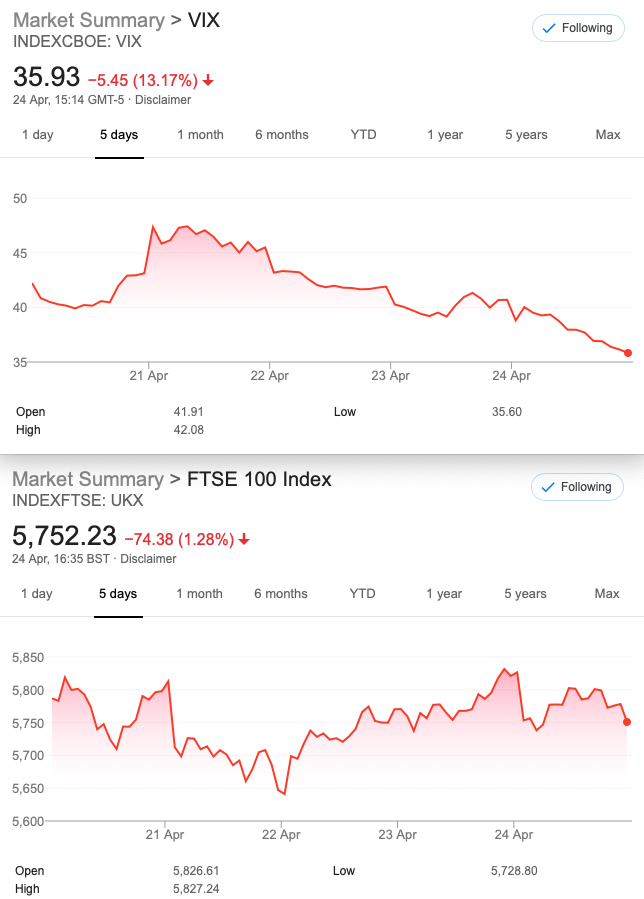

FTSE 5752

![]()

We will go nuts with risk and sell the ATM call and put- a straddle. 168.5+180.5= 349 credit.

Risk, you ask? Well, at expiry we’d be peachy if FTSE is ±348, so 5404 and to the upside 6100

Reason for the trades? Issues with CME options calculator! This will be a pure theta and vega play as we hope both will erode the prices. Delta neutral afficianados will doubtless be delighted! And no, we will not be dynamically hedging, as we have the offsets from both sides.

Apologies for my ignorance- it’s YIN and YANG, not YING.

Karma will doubtless make me pay

289 to close-would you? Profit 60 -comfortable winner with more to go…….

Also the previous weks’ call 3×1 looks rosier too