That Was The Week -A Strange Friday -Late Up Move

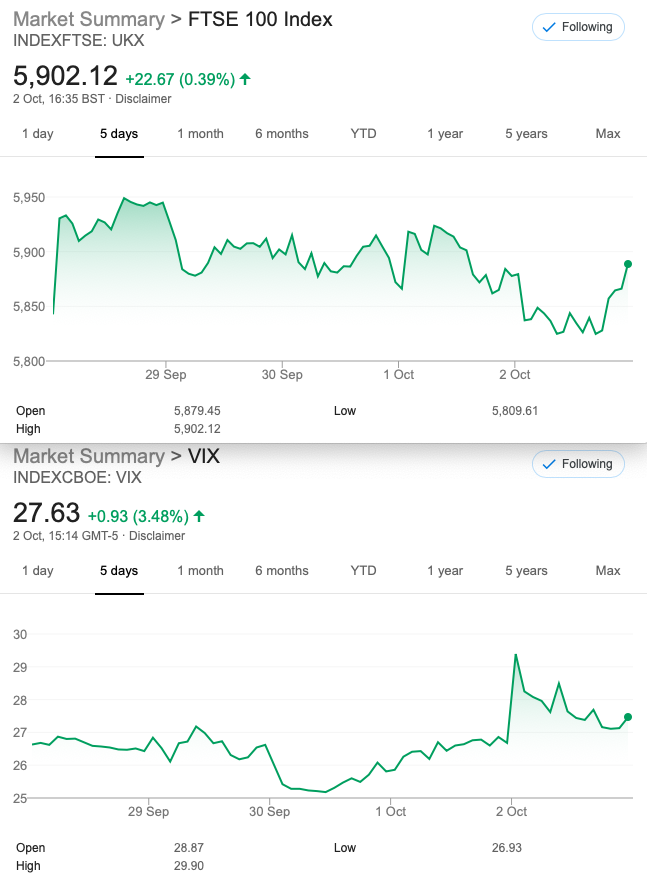

FTSE looking like it’s firmly stuck in a tight range, and of course the cynics among us expect a breakout any minute. Some interesting things came to light this week regarding valuation. This week brought us non-farm payrolls, Brexit lawsuit, and of course the Covid news so while the US has seen some intra day moves there’s no fire under FTSE.This of course serves options traders very well as we don’t rely on the old buy-and -hope strategy. Robin Hood traders, however have made out like bandits out of simplistic call buying.

Many options courses start out with this strategy- great if you are a technical analyst or have some clue about a stock’s future. Citing the old adage of risking 7.5% of your cash to make the same return attracts a fair few. Naturally you can stay solvent for a long time doing this, but good luck with finding those positive looking stocks. My introduction to options was the covered call strategy. And yes, I bought my stock portfolio in 1999 with the market at all time highs.

Taking Another Look At Valuation

Pointed out to me this week by another trader https://www.gurufocus.com/global-market-valuation.php?country=GBR

This site is fascinating though one might wonder if such rampant optimism has any basis in reality. To quote: Ratio of total market cap over GDP: Recent 20 Year Maximum – 184.45%; Recent 20 Year Minimum – 72.42%; current – 89.59%

Expected future annual return: 11.1%

Yes that last sentence…….. really?

FTSE P/E historically has been fairly valued around 14 or so -but now https://markets.ft.com/data/indices/tearsheet/summary?s=UKX.P:FSI

19– That number seems to crop up randomly the same as the much vaunted…. 38 (Was pointed out to me by a certain drummer of notoriety). Whenever there is a random number of items in the news it is frequently 38. I believe this is akin to an ear worm.

Making sense of all the above is fun but we’re just adding more information that may not even be relevant. When we know what to do when a trade goes against us. When our trade choice means not worrying about risk or direction, this reinforces the logic: Options are the best trading vehicle

VERY IMPORTANT MESSAGE FROM ICE.COM PLEASE TAKE NOTE

Intraday Delayed Equity Options Data

For users using the following links:

https://www.ice.if5.com/ViewData/EndOfDay/LdnOptions.aspx https://www.ice.if5.com/ViewData/EndOfDay/LdnFutures.aspx

You can access Delayed Equity data via these links respectively

https://www.theice.com/marketdata/reports/265

https://www.theice.com/marketdata/reports/264)

The above links work now and the old site will be around for a while yet. However, while we have such a paucity of data more appropriate for the 18th century, it’s vital we at least have option premiums. The 15 minute delay? A fellow might ask if a jealous child is in charge of the data. Come off it ICE.COM give us 1 minute delayed and the Greeks, the new site looks terrible.

Legacy Trades, Directional, Delta Neutral, Disconcerting!

Weekend strangler (Remember these close out on Monday)

Last week’s dangerous offering 6050 call 39 5450 put 36 gave us 75

On Monday 65.5 and 17 = 82.5 loser!!!

This week. In light of events in the US we suspend the weekend strangler. Mayhem Monday beckons.

Distraction Trades

As another week passes and the system chucks up excellent trade entries it’s clear that DAX and the DOW are so much easier than sleepy forex. Though I’ll admit to a foray into GBPJPY which just seems to go up! What is even more likeable about the indexes is the obvious times to trade for us UK traders. 7-9 am, 1.30-3.00 pm, around 4.30 and possibly late in the evening when the US is getting ramped in the last 30 minutes. Still a way to go for 100 meaningful events but enjoyable witha demo platform.

Trade 189 -One Trade 2 possible Routes.

We were selling 3 Oct 6200 calls at 45.5, buying 1 Nov 6200 call at 114.5

Then part 2 Delta neutrality, by selling a 5700 put for 43 and buying a 6250 call for 32.5. (Overall credit of 30 something)

So in its original form a three by one….. we had 62.5 -(12.5×3) =25. A credit of 22 to open and a lucky winning trade. Now 38+22= 60 Bigger WIN

We then had to mess with it and the long 6250 call was worth 8.5 but that short put was 86. Thus we had 47 credit+8.5 minus 86 which gave us 31.5 loss Now….. Credit to open of 30 plus a new credit to close of 2.5 a WIN ( let’s persist though!)

Trade 190 Puts Again but a Debit Trade

Here’s the plan…. we bought the 5800/5700 put spread 120.5-86= 34.5. We paid for it in part by selling a 5400 put for 30.5. Our risk is thus at 5300 and we make money anywhere below 5796 at expiry, and it only cost us 4 Now…. 65.5-(40.5+10.5)=14.5 Modest win but we run it again.

Trade 191 Revisiting the Jade Lizard

14 days to expiry so theta is savage. We sell a call spread and an OTM put. But…. the total premium must equal the short call spread (50 points). No risk therefore to the upside, downside risk (see below) max profit 50 with FTSE above the put strike and below the lower call strike . Risk is thus the put strike plus 50, in our case therefore 5625. See below

Thus we sell the 5675 put 36, and sell the 6000/6050 call spread (47.5-32.5) =15. Total premium therefore 51.

189 41+ 22 for the original, and for the Delat neutral 31.5 plus the original credit 30. Deffo a nice win.

190 Debit 4 now it’s…. 24.5-(12 +3)= 19.5. Well you have nearly quintupled your stake!

191 The Jade Lizard … now 25 to close- we took in 51, so let’s say we close out and take 50% of max profit. Happy?