That Was The Week We Tested Support

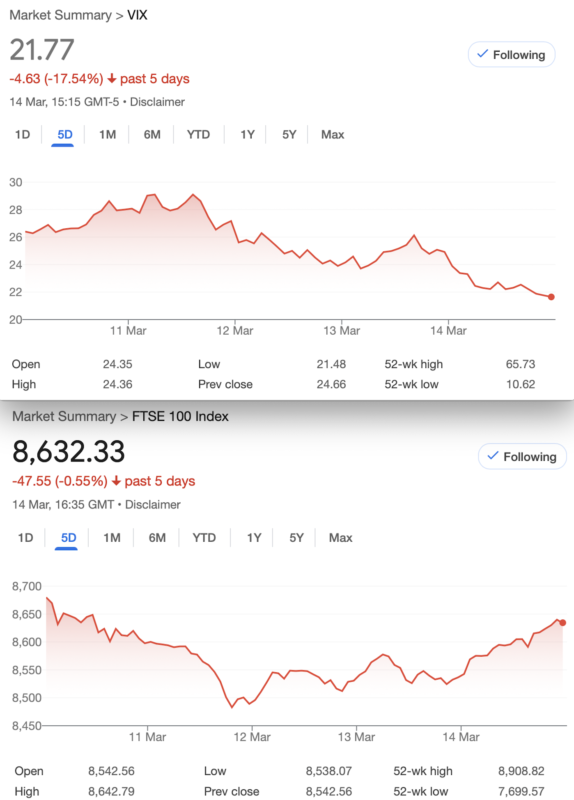

A rising tide lifts all boats but especially when the tide rises in the US. We saw some major buying on Friday, but volumes have been dropping in the last few days. However the market is always changing and the trading volumes we’re told are substantially larger in the derivatives world. The UK economy, we’re told is growing/not growing https://www.ons.gov.uk/economy/grossdomesticproductgdp Fans of stats may find this too tedious to explore further. The real world ‘man on the Clapham omnibus’ picture tells us everyone is struggling. When you look back to when we were all poor, at least we could afford a bus ride, a packet of cigs and a pint. Nowadays that is about 1/3 of the weekly Jobseekers Allowance. Quite how people survive the £15 daily congestion charge for London is a puzzle too. (Of course if you’re on the bus you don’t pay!) Interesting that New York’s proposed congestion charge was scrapped by Trump, it seems a tax on working people, the irony.

So the real economy is in a pickle and this has been a long time coming after there seemed to be no real repercussions from the bank bailouts in 2009. QE had no effect on inflation and interest rates were perversely low. There are natural levels but there was a deliberate policy of financial ‘easing’ for too long. Remember Alan Greenspan and the irrational exuberance? Markets are attractive as investors are repeatedly told that in the long term the stock market outperforms cash. It depends how you cherry pick the data. So we cannot know all the risks but buying a portfolio today in FTSE stocks would give you less of a chance compared to buying in Oct 2008. That received wisdom may not hold water now.

In The Inbox

Again I was reminded of this. https://events.masterinvestor.co.uk/master-investor-show/about-the-show/ March 29th. OK people are trying to sell you stuff, but there are always little gems of information, and opinion from the wise.

I was very late to this but didn’t find it particularly relevant to UK options index trading: https://mailchi.mp/technicalanalysts.com/sta-agm-papers-4965047?e=4e8dea4756 However STA is a noble institution and I’d recommend signing up for their emails.

Not technically in the Inbox but this was recommended to me https://youtu.be/A1_SUlwsWVk?si=5wax4x4YvILqq6M8

Now, I almost celebrated his views on back testing, being quite lazy, error prone and highly suspicious of historical options data. I’d urge anyone to ‘paper trade’ and keep testing, but bear in mind that backtesting tends to be over optimistic*. For our trades here we use the closing prices as those are ‘good enough’ for educational purposes and in real world trading they fairly accurately reflect the relationships between options.

*I used to keep track of ‘missed trades’ -trades that didn’t hit my criteria or limit orders. Nowadays I get a fill as I’m more pragmatic and feel it’s better to be in the market than getting itchy feet and taking the ‘boredom’ trade.

Freebie, A Vital Resource

I was fortunate enough to be directed to a resource for a free trading book. If anyone would like a pdf of Sheldon Natenberg’s classic ‘Option Volatility and Pricing ‘ Email: surreyhantstraders@gmail.com. This is a highly respected and recommended tome and in effect tells you everything you’ll ever need to know to trade wisely. It’s free like everything here and your email address will not be used for soliciting anything whatsoever.

Distraction Trades

ADA was $0.8104 now $0.7447

XRP was $2.3444 now $2.4210 If Trump gets his trotters further into crypto, it may not go well. The US government has made $$$ from the Bitcoin seized as proceeds of crime(And Oligarch super yachts!) .

DAX : Monster Week minus another 330. Stopped out by a whisker on Friday. 6 trades in all 1 loser 1 break even 850 -brilliant week, but remember this is demo trading.

UK Gilts were £16.05 now £16.02 This is based on the Vanguard ETF (not a recommendation) A rocky ride as £17 is now a distant memory, but this is a back burner investment.

Legacy Trades and Challenging Trade 406

Trade 396 Calendar/Time Spreads( Running Having Rolled )

Expiry at 8685 gave us 485, and 385×2= 285 LOSS

Dare we roll? We are here to educate by doing so here we go: Rolling to March 8200/ 8300 would give us 273.5, so we have a rather ugly cost of 11.5.

Now –Yikes! 596 and 498.5×2= 401. This is purely for academic purpose and we would not suggest/recommend or in any way approve of such action/inaction. However to see how this pans out we will run it.

This week 497 and 401×2= 303. So it’s an improvement but horribly deep in the money, we’ll keep it going and rolling purely for punishment!

At close on Friday 444 and 346(x2)=248 355 , 261(x2)= 167 on Thursday (We’d take that all day long) We continue to roll

Trade 401

We went with the esteemed Professor’s straddle, and February worked well, remember .Now we have:

Previous week : March: 8700 call 71, 8700 put 124.5 Our initial credit was 239 thus we have 239-(71+124.5), gives us 44.5 WIN

Last Week: 8700 call 142 8700 put 51.5 =193.5 (initial; credit 239) 45.5 still winning

This week 8700 call 74 and 8700 put 86.5 =160.5 (Winning as initial credit was 239) WIN 78.5

Now we have 31.5 and 91.5 =123 WIN OK It’s been a nice run but we’d definitely take this 239-123= 116

Trade 402 We Use March Prices

An old chestnut and a safe trade with fair chance of doing ok. It’s the iron condor. We sell both side of the market but with short spreads. So the prices nearer the money are the options we sold. And here we choose 50 point spreads. Calls: short 8850, 47, long 8900, 34.5. Puts: short 8550, 59, long 8500 47.5. So as a credit trade we take in 12.5 for the calls and 11.5 for the puts. We take in 24 and our risk is 50-the 24 credit It is a dull trade with limited potential as it ideally needs to see both sides at expiry got to zero, avoiding costly commissions.

However there is an ex-Harvard man, Jared somebody, who made his first $million in his early 20s with these. He may still be in the same business, but these went pear shaped for a while as risk/reward no longer stacked up.

Calls: 8850 25, 8900 17 = 8, Puts 8550 62 8500 49= 13. Rather uninspiring, but ok.

Was : calls 57, 39.5= 17.5 puts 23,18=5 Gives us 22.5 (initial credit 24)

Was calls 19.5, 11 = 8.5, puts 39,31= 8. 16.5 against credit 24 Boring and a bit ugly

Now: calls 4.5 and 2 = 2.5 puts 28.5, 19.5= 9 WIN It’s made 24-11.5=12.5 which is 50% of max possible profit -we’d close out but run for fun

Trade 403 How to be Bulletproof For Next to Nothing(March Expiry)

Futures point to a very likely drop on Monday but we have Friday’s prices as always. So, swings and roundabouts, we place the trade which is a ladder/condor/Xmas tree. It’s a combination of 2 ratio spreads as follows: Long 8600 put 78.5, short x2 8450 put 39.5, long 8300 put 22, short x2 8000 put 9.5. Here’s the arithmetic: 78.5+ 22, minus (39.5+9.5 x2)= 2.5.

So for a cost of 2.5 we get nice downside exposure at 8600 and risk is very far away at 8000. These kind of trades have a very wide profit range no upside risk but possibly only a moderate chance of profit.

Those prices were 29.5, 14.5×2 and 9, 5×2. This gives us overall minus 0.5 Early doors

Was 50.5,- (24.5×2), 14.5 -(10.5×2) = Minus 5

Now: 42.5, 14×2, 6.5 and 2×2 gives us 17 WIN We’d take that although on Thursday it was 28 which we’d have taken even more happily.

Trade 404 Long Shorts

Fuelling the bear position, remember? https://worldperatio.com/area/united-kingdom/

What if we decide to get short with a short call and a long put spread? 8900 call 39.5 long the 8800 put and short the 8700 put 89.5, 51.5 =38. We have 1.5 Credit and a massive dose of ‘Hopium’. I doubt this is a good trade given the epic run of the Western stock markets, but let’s view it as a bit of downside protection, with maximum reward 101.5.

Now 8900 call 11, 8800 put 144.5, 8700 put 86.5 Gives us 58-11= 47.(1.5credit at open) WIN Almost 50% of max reward, we’d close out. Run…for fun

At close on Friday 75.5. Thursday’s close: 88 Exits are 90% of the process but we’re always happy to take what is ‘reasonable’.

Trade 405 Time to Get a Calendar Trade

We are selling the March 8650 put for 66, and buying the April 8800 put 196 and selling the 8650, 123. Thus we have a long spread in April with max reward 150. This is a small debit trade, we pay 73-66= 7.

Now: Mar 8650 put 63 April 8800 put 218, 8650 put 132.5 Gives us 85.5- 63= 22.5 A profit. Expiry may see the 8650 put go to nothing, so we run it. Of course it could get crazy, that’s all part of the game.

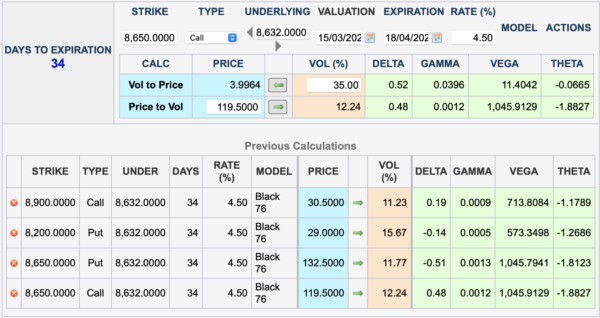

Trade 406 Straddle Versus Strangle(April expiries)

Here’s a bit of fun and each week we’ll update what’s winning and what isn’t. So….. the 8650 straddle: call 119.5 and put 132.5 =252. Strangle: 8900 call 30.5 8200 put 29. To keep premiums level we sell 4 strangles against 1 straddle, which then gives us 252 against 238

Remember we use: https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html

What’s YOUR prediction?

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.