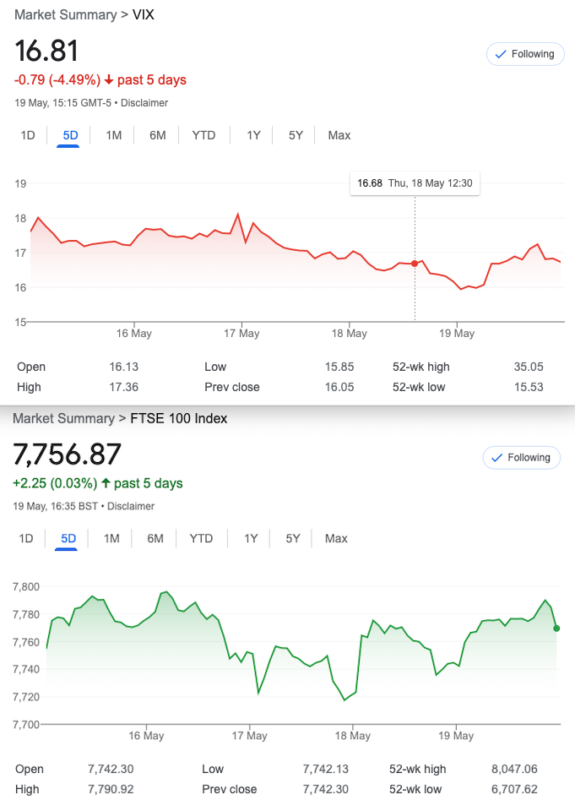

That Was The Week The US Was Positive, FTSE Flat

Us Brits are know for our sense of irony and it was with some degreee of derision, I noted Friday’s headline proclaiming FTSE rising on positive consumer data, so I thought I’d better check. https://www.forexfactory.com/calendar#closed Our trusted resource showed UK consumer confidence :![]()

Yes, minus 27! And, the last time it was positive? January 2016. However the expectation was for minus 30, so it’s a big move into the slightly less hilarious 27. British understatement may well be the cause, but seriously are these numbers really productive use of people’s time?

Our May trades did ok, 3 wins and pretty much as expected the ‘Hail Mary’ trade went the way of all flesh. We will continue to try things out and while the concepts may be fine, the timing may have been off. We hope the market timing gods will give us fair warning, to date they have been absent. Energy costs are on the way down. Interest rates may follow. We hope the world can be a cheerier place though the omens are not great.

While We Use The Term Investing, We Trade and Imply Investing by Being Active

Here is a take on passive invetsment and some of the fallacies around that. I will not dwell on this but have recently been forced (unhappily) to take investment postions in ISAs and pensions. https://fortuneandfreedom.com/stocks/the-end-of-a-20-year-bear-market-in-the-ftse-100/?bsft_aaid=1daf734a-e9f4-4967-890e-127b4eb2f277&bsft_eid=9e6f0390-5d5a-10ec-11c1-37a53746d2f7&utm_medium=email&utm_source=blueshift&bsft_clkid=e8e23ad1-d223-4e17-9f93-886e913af163&bsft_uid=ea5a2f2e-8db8-41e0-aae3-743b43a8354b&bsft_mid=889a4a99-5581-49f3-9d5e-c18495722a48&bsft_utid=ea5a2f2e-8db8-41e0-aae3-743b43a8354b-SB_FAF&bsft_mime_type=html&bsft_ek=2023-05-17T14%3A30%3A41Z&bsft_lx=1&bsft_tv=2&pk=dba462d873d825bf4ee84c32171fa8b7&utm_campaign=FAF_170523_EXCL_BUY&vid2=ef0bbe36e6c5fdc1d40ccf940dcd511c31f0733e3e6828ae2a47ddbfb72854533068262f70bf4373e0c17b18a69b1242

Apologies for the length of the link and the article, but it makes the point rather well. An investment is a trade gone wrong!

Singing the Praises of Options Again

I saw this flagged up recently, not sure of the source, so apologies. However: [It could be argued that not having insurance is a bigger risk than anything else, something BP knows all too well. It had opted to self-insure its operations in the Gulf of Mexico to save money, but in 2010 when the oil rig Deepwater Horizon failed, it was on the hook for all of the resulting losses. Today, BP has paid out $70bn in compensation and clean-up costs, selling valuable assets to foot the bill. If it had chosen to buy insurance, the $70bn bill would have been absorbed by several firms across the insurance industry.] Yours truly sometimes forgets that while options are stage centre for us, they can of course be used as insurance, buying cheap put strategies for example on the Index against a basket of stocks can make perfect sense.

Quite why this cannot be a feature of an ISA shows the lack of sophistication of the powers that be. Once upon a time there was something called portfolio insurance. We who were around for the crash of 1987 saw carnage for the uninsured, but also carnage for the insurers. Those insurers did not insure/hedge with options. Traders like us know options are protected by being exchange traded. Regulators need to get with the programme. I shall not be holding my breath!

Distraction Trades

ADA $0.3651 I had taken a loss and closed out at $0.44 a while ago. It’s looking a bit grim still.

XRP $0.4671 Crypto’s continued cryogenic coasting. Nothing to trade here

DAX 3 no entries, one loser, one break even. A grimmer week we’d be hard pressed to find, given that DAX smashed up 200 point on Thursday.

Legacy Trades, 3 wins, a Hail Mary Loss and 317

Trade 313

As you’re aware, this is not about bragging rights, it’s about learning.We have extensive runs of wins and statistically we were due a run of losers. It’s a ‘cheap’ market, with no expectation of a big drop. However, we can maybe find a trade that is not a horrible loser! We find a long put spread 7850/7750 and a way to pay for it with a 7600 put. This gave us 70-46= 24 the cost of the spread, and we sell the 7600 put for 27, giving us a credit of 3. Thus, the trade can make a max 100+3, and is safe all the way down to 7500. There is of course, no risk to the upside(makes a change!)

Was 70.5-8.5 =62 Big WIN!

Expiry around 7775 gives us 75+3=78 WIN!

Trade 314 -When There’s no Vol

We placed a strangle with May options and 21 days to expiry. Frankly I just like the round numbers, so this may not go well! We sell both of these as it seems that they are at strong support and resistance. 8000 call 15.5 and 7500 put 15.5 . Credit 31 means we break even at 8031 and 7469.

Close out! We make a healthy near 50% in a week. 31-17=14 That’s 45% WIN Again we will run it to expiry for educational purposes.

Was a stonking 26 now, at expiry the max 31 WIN!

Trade 315 Calendar Time -Shall We Get Spicy?

So, the principle here is that time decay works faster for options as they near expiry. Thus we can take advantage of this by selling the May options and as protection we buy the June options. We can sell 1 in May, or 2 or 3 against 1 in June.

Here’s what we did: Sold 3x May 7500 puts, bought 1 June 7550 put.

Note: Deltas 11×3 =33 against 25. Theta : 5.05 against 1.4471 =3.6 Gamma 24 against 8, but not too crazy, with vega not so crazy against us either. We have 2 weeks to get our b*tts handed to us.

Welcome return to Profitville, our home. We sold 3 7500 May puts which are no 5×3= 15. We bought the 7550 June put,and it’s now 47.5. Gives us 32.5, a WIN, but we paid 60.5-(14×3)=42. Which gave us a cost 18.5. Therefore, we make 14 .

This week, run to expiry 36.5 was the best we could do, but Wednesday gave us 49.5- 2×3= 43.5 (minus our cost 18.5) Gives us 25 WIN!

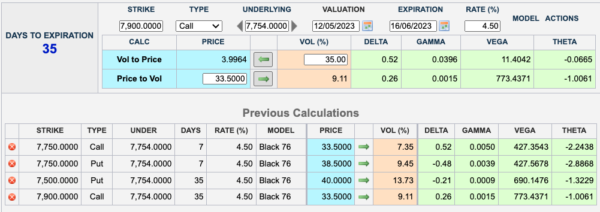

Trade 316, Last Trading Days into Expiry

Firstly I hope it is clear from the graphic that there are 4 options calculations. Secondly, this is untested but we’ll throw it in the mix for fun. We have renewed our winning ways and don’t want to spoil that. However we are here to educate, nothing more. And this is a quirky one. We are buying the May straddle, and selling a June strangle. Why? If we get a half decent move(downside preferred) the near month straddle is far more sensitive to price changes of the FTSE. It is a ‘Hail Mary’ trade as they say in American sports films! In summary we buy the 7500[error!] should be 7750 call and put for May(The straddle). We are selling the 7900 call and 7500 put for June(the strangle). The prices are thus: 33.5+38.5= 72 for the May straddle. We receive 33.5+40=73.5 for the June strangle (7900 call and 7500 put) We therefore have a credit of 1.5.

Apologies for this, It should have read, we are buying the 7750 straddle(NOT 7500) for May selling the June 7900c/7500p strangle (27.7+22.5) LOSER!

We lose at best 10, at worst 25-50= 25 at expiry- though we could run our short strangle to expiry.

Trade 317 A New Expiry Month

A homage to Liz and Jenny once more as we borrow from the esteemed Tasty Traders, the strategy known as the Jade Lizard. This trade has no upside risk, as we perceive the danger may lie that way. June expiry. We sell a call spread: Sell the 7800 call for 68.5 and buy the 7850 call for 45. We sell the 7550 put for 27.5. Maths scholars will note the call spread credits us with 23.5, add this to the credit for the put we sold, gives us 51. Figured out the upside potential loss? It’s the value of the call spread,which is 50. Downside risk at 7550 minus the credit 51= 7499

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.

Yikes! The Jade Lizard looking ugly. Do we let it run, or adjust?

We could buy the 7650/7550 put spread for 35, giving us a little leeway on the downside, and remember we took in premiums amounting to 51.

We are still a fair way off the 7550 level so no cause for panic.

another adjustment might be to look at the upside risk, the7800/7850 call spread, now worth about 8. Buy that back and sell a 7750 call for 40. We now have 51+32 in premiums taken in, and a risky strangle. We know volatility is mean reverting but when it will revert is another matter!