That Was The Week -What The Actual????

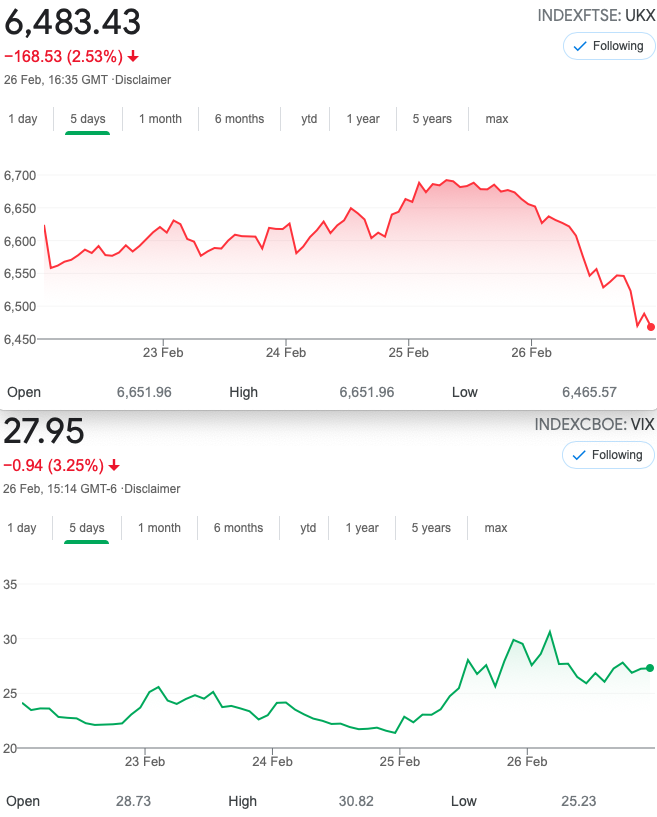

So, my understanding of bonds versus stock market is that when one is out of favour, the other one gains. Marketwatch helps out a bit: https://www.marketwatch.com/story/dow-futures-point-lower-after-rising-bond-yields-spark-tech-rout-11614343092?mod=home-page

This concerned trader would like to know, if bonds are now cheap, who sold them and who are the new buyers? I’d venture to suggest there must have been some massive losses for bond traders, yet the stockmarket- specifically FTSE was clobbered. We are supposed to be concerned about inflation, but that has been trotted out for decades. Markets move and often nobody really knows why. We hope this does not signal another sell off. Optimists were beginning to emerge and almost nod sagely as Boris trotted out the road map speech. The one way street!

Distraction Trades and A New Insight Into TA

Wednesday, bang on 08:00 am the DAX gave a great long entry. Thursday at 8…. a short. Our trades both doing >100 pts. In fact we closed out that short early and it could have made so much more. Signals are signals. Rules are rules. We thus persevere with a flawed but functioning system.

My attention, this week, was drawn to this, from a TA website

This trader loves ‘Gold & The Vomiting Camel’ A worthy title for an episode of Hergé’s Adventures of Tin Tin. Who uses charts, and how does TA work? Charts can be seen in every trading room on trading screens, so they cannot be ruled out. But patterns? We can easily see heads and shoulders, wedges, flags and pennants. Though we are assailed with so many interpretations of the visual image. In my own trading I tend to look for areas of support and resistance. Caveat: as a self confessed terrible trader this may be way off beam. Personally my view of that chart would not be a ‘pattern’ but another visit to the last recent low. This bargain hunter would be a buyer, albeit tentatively. Providing I were unafraid of the vomiting camel. The jury’s still out on that one!

FTSE Options Prices From ICE.com

So, the old link has now been terminated in favour of https://www.theice.com/marketdata/reports/265

The new style is actually very functional and saving the day’s prices in pdf is very friendly. Trades posted here will of course always use the settlement prices shown there. The ‘Mr. Magoo’ setting takes some geting used to, however. Adjustment is simple enough on screen.

Those Legacy Trades

207 Something Bold? Unseasonal Strategy For March Expiry

A debit trade….. hmm spending money is always a concern. So here’s a christmas tree

6450 put long 6300 short 5950 short 5800 long 5600 short. In effect a condor with an extra short

Those prices 97.5 61 24 17 11.5 Thus we have 2 longs 97.5 and 17 and 3 shorts 61 +24+ 11.5 A debit of 18 Max profit 150-18= 132. Risk at 5600, but bulletproof down to 5800

Longs worth 71+15.5= 86.5 shorts 45.5, 20.5, 11=77 now 9.5 (cost 18)

Now longs= 163, shorts =143 Credit 20

Trade208

We seemed to be going nowhere with possible downside risk. My assumptions are mostly wrong but aside from a strangle which annoyingly has done well recently, what else can we see?

I am drawn to this- a long straddle financed by a 2x strangle, Thus we BUY 6600 straddle, and sell– well you figure it out!

That straddle costs 123.5, and 118. So we have to sell 2x 6725 calls (63×2) and 6400 puts (60.5×2). This gives us a 5.5 credit. The point is our cost is negative, and now our risk is at 6850 and 6200. Reward? A whopping 200 or 125 to the upside.

Now the long straddle is worth 269.5,and the short 2xstrangle =279. A small loss

Trade 209 Melt Up or Melt Down?

Short iron condor anyone? Instead of selling a call spread and a put spread we will buy them to capture any big moves.

These strikes may produce the goods: 6350/6250 (101.5-77) for puts, and for calls 6650/6750 (39-18)

Our cost is thus 24.5+ 21= 45.5. Mitigating cost is one facet of options trading and at some point we can sell something to offset our costs. Downside might give us increased volatility to sell say a 6000 put. Upside could give us a chance to sell 6900. Buying a spread does not eliminate theta but helps, and lowers costs too. Maxmimum profit is of course 100 minus costs. We need to lower those costs.