That Was The Week

Astonishing yet lame. 6 consecutive down days-what the heck is going on? Nobody knows what they should be doing. Including this idiot! I do from time to time mention the skew of the up days outnumbering down days. Recently it hit about 20. So the recent spat of downs has somewhat redressed the balance. However the US was up in the last 4 days making new highs while the FTSE was 48 points lower.Zzzzzzzzzzz

Shock and Dismay- Yet Again UK Traders Beaten Down

https://research.ftserussell.com/Analytics/FactSheets/temp/9e03b0b9-b214-4bc0-b01c-d4a65a6a09db.pdf

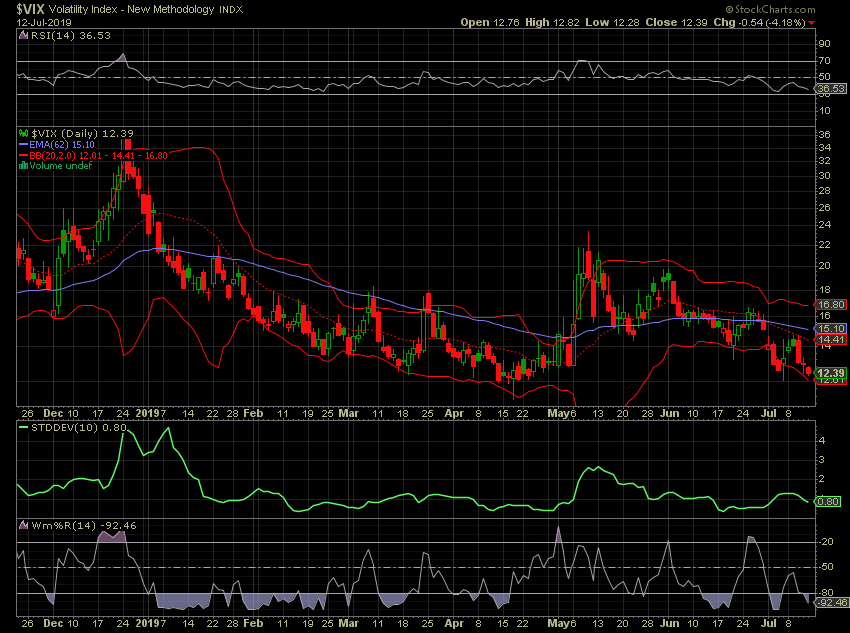

Traders with a keener eye than this idiot will have noticed- VFTSE was killed on 27June. Doubtless nobody made money from the 2 minute calculation required (when you have the data and formula). We have only VIX as a barometer, though this week we have moved out of sync with SPX. We have long since moved out of lock step with SPX. Not so long ago SPX x 5= FTSE, nowadays that would make FTSE 15000.

What Are The Factors In Play Here?

Without clarity of VFTSE I think we can assume that seasonality, forex and politics are all in play. The latter being only very transitory in nature.

Our Three legacy trades:

Trade 136 originally a credit 83 ( ( short7350 straddle 126+36.5) long 7250 put 7450 and call 19.5+ 59.5 ). Now 94– so a losing trade,but in for a penny etc. Now 162.5-(69+2)= 91.5. Still losing

Trade 137 Tiny Loser

So, we bought the July 7150 puts(21) and sold twice the amount of the 7000 put (10). Debit 1. But it’s still worth zero.

Trade 138- Closed Winner

So from a cost of 0,on the 3rd July we could have got (59 – 4.5) = 54.5.( We could have got more)

Trade 139 Closed winner

We sold the 7650 call and bought 7400 put. We thus took in 14.5-12=2.5 so it was a tiny credit. Now call =1 the put=8. Close for 7, but remember we do these in multiples 5-10 lots, so a possible £450-£600 profit.This was at best a win for 10,plus the initial credit with such low volatility.

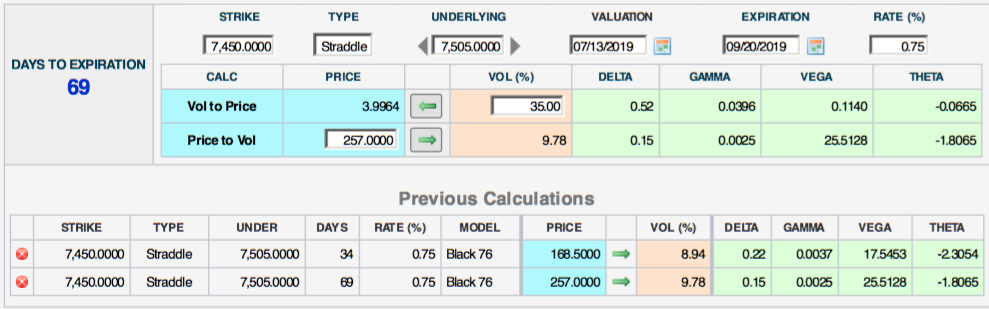

Trade140 That Weird 3×2.

Avid readers may recall that on occasion we have borrowed from some of the great traders. While I never condone taking a stab in the dark these trades can be fun and fairly safe. Theta works against us as we buy 3 near month (Aug) 7450 straddles and pay for them by selling 2 far month(Sep) 7450 straddles. We have delta and gamma, and hopefully vega in our favour. Theta is, however the big party pooper. We need a boost in vol in the market that sees near month prices rocket, while far month reacts more measuredly.

Here’s the trade: Aug straddle 82+86.5=168.5, long x3= 505.5. Sep straddle 122+135= 257 short x2= 514.

As you can see we have a nett credit of 514-505.5= 8.5. However that is not much of a contributing factor. We want to see front month straddles worth say 220 while far month are still only 250-270. Risk is pretty much discretionary but we may see some bigger moves and subsequent rise in volatility to help us. We’d take 100 profit but settle for a quick 40 in a week. again we’d position size -say 15/ 10.

Remember: Options are safer than people understand so in a chaotic market this is not likely to risk much. In fact it could be a monster win.

Trade 140- I think we close for a small credit of 8.5 giving us 17. In real money that’s £170, but if we were doing our standard 5 or 10 lots we’d belooking at about £700. The reason for closing out was the fact that we had 2 up days andthose tend to suck the volatility out ofthe near month. The market had moved over 1% and these only make money on moves of about 1.5%. Sorry this is late but yesterday was a tad frenetic in my other life. We’dbook this as a winner but out of curiousity let’s see how it unfolds