That WasThe Week The G7 Put Up With The Orange Princess

“I’m the boss” proclaimed the World’s dumbest ‘leader’. Threatening to ‘drop bombs on the heads of Iranians’ should have earned him more negative Brownie points, but that score is already below zero. Is this the best the World can do? Unashamedly political but my frustration is that my living depends on a market that, is akin to the quote: ‘ like a madman in charge of the elevator ‘. We saw FTSE buck the trend and then make another gentle step down. The point and figure chart of course needs to reverse when FTSE has made the required 3×50 point move. It’s hit an inflection point of, er, indecision. We’ll put point and figure back in the cupboard, for special occasions! https://www.tradingview.com/chart/ruRQwx7O/

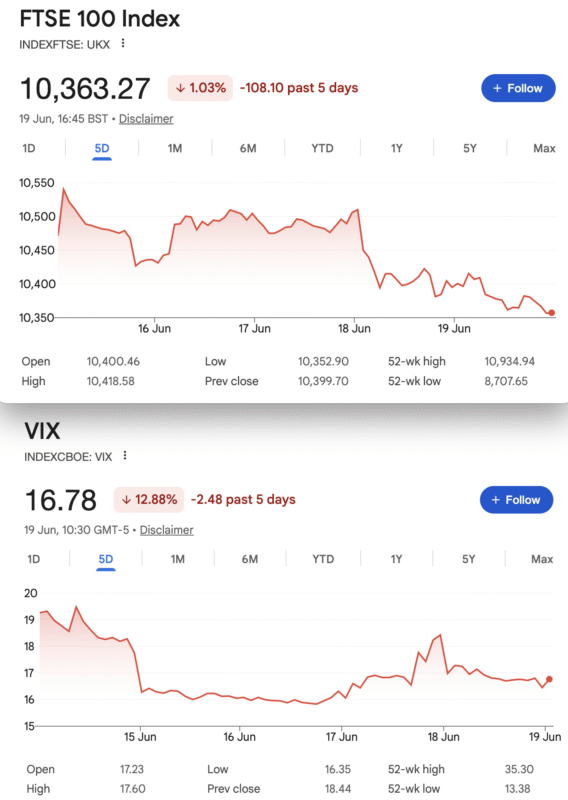

We saw FTSE expiry on Friday at a bizarre 10370

You can make up your own mind about the price action https://finance.yahoo.com/quote/UKXSP.L/ Watching expiry live on a 15m delayed chart is bonkers and at times it seems to go into real time. The trick is not to get your backside kicked by leaving near-the-money options to the mercy of the PIN.

Some Musings on Personal Trades

I do share some of my trades here but never say which ones. I recently watched my trade with a potential max profit of 600, go to 300. This trade was placed at the end of March for this June expiry. I watched it go from the credit I got, 22 to an epic 100 a week later. My first thought- it has a few months to run, no need to panic. During the ensuing Iran/US situation, it then quickly went in my favour. Now: If it’s such a good trade why did I not have some more at 100? Some mitigation, of waiting for cash to bolster margin, but in theory, so many times this has happened, and proven to be a smart move. EXCEPT. The last time I added really big money to a trade because the premiums shot up?…………. 20 February 2020. Utter disaster.

So how did I do? I closed out for 100 when 300 was on the table. And this week that proved to be a rather poor exit as 200 had been on the table in the last week. How can anyone know it’s a good exit? Nobody knows, but my own rule, when 40% of max profit is locked in, take it. Platitudes such as ‘well it’s still an awesome profitable trade’ are worse than being called an idiot. I like to be indulged in misery, so happy to be called an idiot. THAT is the edge the fund managers have. I would relish a proper trading floor, but at my pace. Yes, I’m generally profitable. I don’t have the seasoned mentor who would have helped me make sense of it. But here I am sharing it with you. I am fallible and flawed, options give me a free pass.

In The Inbox

This fellow seems to trade the UK, but is American, don’t let that put you off. I rarely consider these things a waste of time, and this looked interesting

Another of Larry’s presentations, I think it’s 20 minutes of useful content https://optionstrategist.substack.com/p/intensive-option-webinar-volatility?r=p9k8q&utm_campaign=post-expanded-share&utm_medium=web&mc_cid=28894c5c72&mc_eid=5f15d5ff5d&triedRedirect=true

Distraction Trades

ADA was $01724 now $0.1624

XRP was $1.1445 now $1.1459 Crypto has not been convincing lately. I like this source https://coinmarketcap.com

DAX : Under review after poor record lately We are floundering here as volatility hits our 40 point stop even while direction is right – a case for 0DTEs?

UK Gilts Were £15.68 now £ 15.64 This is based on the Vanguard ETF. Not the cheeriest outlook, yields in the short term may be worth a look, current yield 4.78%

Silver: Using Wisdom Tree Physical Silver(PHAG) Went long at $71.31 and last week it was $61.69 now $58.85After the massive 10% rise it crashed back down and hence my entry. Do not follow me this is not a huge position and luckily I have done well this year with Ag.

Legacy Trades and New Trade 471

Trade 424 High Roller, This is a Trade Gone Wrong

PRECIS: We started from a July 2025 losing trade as below. Short calls are rarely a good idea.This is a ratio spread 8450/8650 calls

In summary we have an old trade from July 2025 which is a loss of 1741 against the credits taken in, of 422

Was 1539 big yawn but that’s the point. This will run until it’s no longer in a loss.

then 1912, 1712.5(x2) gives us 1513

then 1771 1571.5×2 = 1372

Crazy time, as our strike( 8450) does not exist for June so we roll from 1914,1714=1514, to the new strikes up 50, 8500/8700: 1875.5,1678 =1480.5.

Our new position therefore is 1480.5 underwater and we have a debit of 33.5 So the running income is now 422-33.5= 388.5

Previously 1984,1786= 1588 underwater

Last, 1939.5, 1740.5= 1541.5 ( Currently rolling to July would give 1579.5 )

Last week: 1,884.5, 1,685×2 = 1,486 ( possible roll to July 1507.5 )

Was : 8500 1963.5, 8700 1764 x2= 1643 Looks like a roll might cost money

So, cost 1606.5 to close, buy to open for July 1640. A credit 33.5 ( Running income 422 )

Trade 466 Shoot ME! It’s NOT a Butterfly

It’s so simple- we use the long spread(June 10100/10000 put spread) from 465 and create a butterfly by selling the 9900/9800 spread for 98.5,78.5= 20. We carry forward the 3 debit

Now this is not only bulletproof but can still make 100 such is the beauty of options, we take a credit every month and sometimes we get the big win. Worst way we still have 17 credit and there is no margin used for a butterfly. In fact it’s a credit in margin.

Now: 48.5,37.5 and 29.5,23.5 =5 And……. it is a C O N D O R !!! Why? The ‘body’ is wider than a butterfly which simply uses the same strike 2x for the body. You know this

Those prices were: 10100 33.5 10000 24.5 9900 19.5 9800 14.5 = 4 That’s a bit rubbish!

Now 10100 23.5, 10000 15.5, 9900, 10.5 9800 8 gives us 5.5 Come on you sellers and uber bears!

10100 8.5 10000 5.5 9900 4 9800 3 =2 Horrible!

Ugh! Well we still had a credit 17 LOSER

Trade 467 Easy Money?

Looks like the 10000 level is easy pickings for Put sellers but as always we like to have something in the back pocket. We sell the 10000 put twice for 37.5. We buy the 10150 put 55.5. So we now have risk as 9850 which strike seems unassailable. We have a credit of 37.5 (x2)- 55.5=19.5. Ideally you’d sell puts when the volatility is high but it’s never that simple. Friday 15th May looked like the start of a bigger move down. Hard to be emotionally neutral these days

10150 39.5, 10000 24.5= -9.5 ( We took in a credit of 19.5 remember ) Sort of winning….

Was 10150 30, 10000 15.5(x2) -1 Is this the roller coaster ride for June expiry?

Now 10150 10.5 and 10000 5.5 x2= -0.5

Well, we WIN our credit 19.5 Sadly not the possible 150.

Trade 468 Ratio Iron Condor – acronym Rico?

Ok, there’s something going on that doesn’t add up. VIX is at the year’s low, markets are hitting highs, FTSE is not. Either it will catch up, or it is ahead of the game and the much flaunted crash will be in a market near you. We don’t always like to take a credit just for the sake of it, but ticking over with small wins is ok. We have a ‘short’ iron condor though on both sides we have ratio spreads. Traditionally the middle strikes (body) is sold and the wings (outer strikes) are bought. Here we buy nearer the money on both puts and calls and sell x2 further out. We have a credit of 12.5 just to keep us turning over. Prices: Calls: 10700 28 10800 14x2 Puts: 10000 24.5, 9900 18.5x2 Risk is at 10900 and/or 9800

Was Calls 10700 9.5, 10800 4(x2) Puts 10000 15.5, 9900 10.5(x2) = -4 Headed, inexorably in our favour. Surely?

Calls 10700 9 10800 3.5(x2) Puts 10000 5.5 9900 4(x2) Yawn……

We keep our Credit 12.5 WIN

Trade 469 It’s That Bonkers Trade Again

So the trick with this is that it’s a gamma play -and as we near expiry, gamma* increases dramatically more in the near month than the far month. In English, a June straddle would move more than a July straddle, but we don’t do one for one. We sell 2 x July straddles, buy 3 (three) June straddles. What could go wrong? T H E T A will bite us. What could go right? Gamma and near month volatility can work in our favour. So here’s the deal: 10400 Jun straddle 88.5, 102= 190.5. July 10400 straddle 176, 170.5= 346.5. This can work in a heartbeat but can drag on for a soul crushing 2 weeks. So we pay 190.5×3= 571.5, we take in 346.5×2= 693. Credit 121.5

While the credit looks spicy, remember we will have to pay big to close this out but the trick is to pay a lot less than 121.5 Did I mention this trade is bonkers but has worked in the past…

On Friday we’d have paid 182 but on Wednesday we’d pay 83 to close. As stated you have to be nimble and so the best was a profit 38.5. You would not leave it to run as shown by Friday’s number. We will not run this to expiry by choice, but to see how ugly it gets

*Gamma rate of change of Delta -you know this stuff!

Picture this: Expiry at 10370 we own 3 10400 puts at 30 x3 =90 but we OWE 2 July puts 130×2, and 2xJuly 10400 calls 120×2=500. Remember we entered for a credit 121.5 There is no way you’d run this to expiry but the reverse trade would have done ok. Remember, theta on straddles bites your b*m.

Trade 470 Risk and Repeat

Cheeky repeat trade, the spicy strangle selling both: 10200 Put 13.5, 10650 Call 15 gives us 28.5 It’s not much reward for high risk, so we may need to get active. However we can add a little downside insurance for not a lot of money buying the July 10200/10100 put spread for 65.5-50= 15.5.

Next week’ s expiry may be a crazy affair either way but promise to find some more interesting trades.

WIN! We get to keep all of our premiums again . Anyone know the track record for these expiry week strangles? (I don’t really like them )

Trade471 A New Month -Seasonality?

Ask AI- https://www.ecosia.org/ai-chat?q=july+stock+market+performance

It seems when July takes a dump it’s of Elephantine proportions! But typically it’s an up month. Should we pay much attention to the past?

I like to think there’s a disaster around every corner, like all good dramas! Let’s buy a cheap handsome looking put spreads and pay for it by selling a put further out. Those strikes and prices: buy the 10100 put, 45, sell the 10000 put 32.5 and sell the 9700 put for 14. Gives us a tiny credit 1.5. Most likely it will go to nothing and we lose nothing. But… it can make 100

Glossary:

There are two types of options: Puts, give you the right but not the obligation to sell the underlying asset . Calls give you the right, but not the obligation to buy the underlying asset.

When you sell those options, the opposite happens, with puts you get stock ‘put‘ to you at an unfavourable price (or not) and calls you get the stock you own taken, or ‘called’ away. If you don’t own the stock you need to stump up the cash, but in both cases with the FTSE index they are cash settled at £10 a point, so losses and gains are uncomplicated.

Please read the links below for a more comprehensive explanation in simple terms. Options are about mindset, only a modicum of intelligence required.(I’m living proof)

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com.

If there is anything you’d like help with, we all started somewhere and yes, it can be baffling. There are no stupid questions, give it a whirl. (AI gets things wrong, remember)

All opinions expressed here are not to be taken too seriously and all of the trades are for educational purposes only.