That Was The Week: Big Ups Met the Big Downs

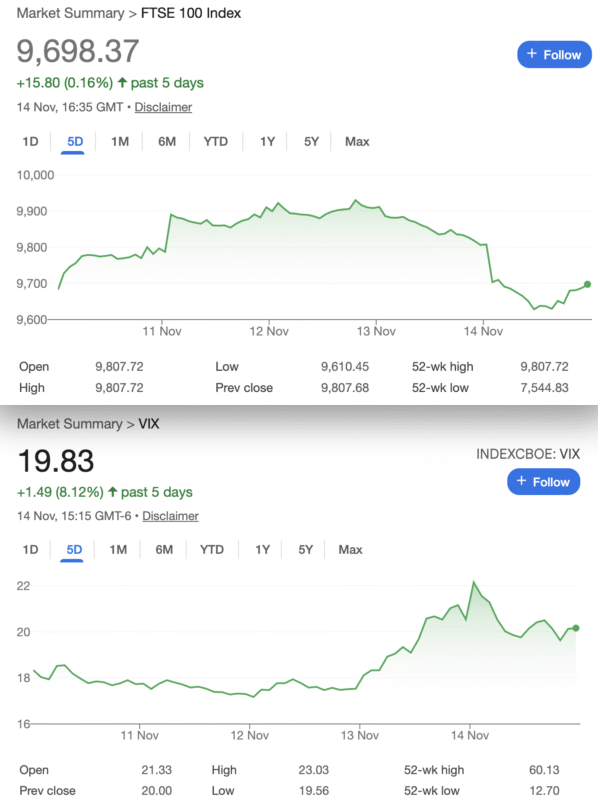

So, this graphic better represents the FTSE’s price action, in case anyone was not watching. So is this important TA? A spinning top, sign of a classic reversal? Of course we cannot draw any conclusions from what appears to be Algo’s having a bit of fun. It’s heartwarming to see this bully of a market got a bit of reality at the end of the week, but then the frenzied buying came in. When America wakes up, the dollars start going to work and bang on midday on Friday there started an 80 point rise from the day’s low. DAX generally gets the love from the US around the same time, allegedly. However, the reality is that the UK economy, if adjusted for inflation, is a hot mess. It’s a recession in anyone’s language but as we so often say, the Stockmarket is not the real economy. https://worldperatio.com/area/united-kingdom/#google_vignette

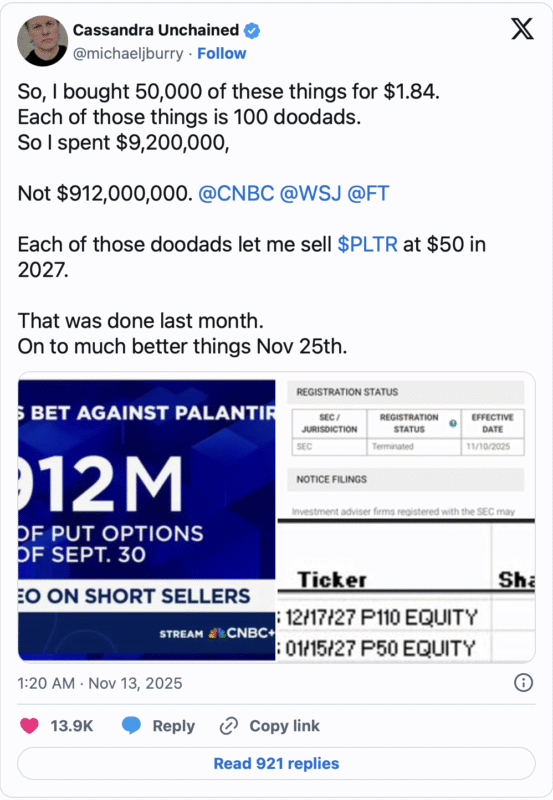

Geopolitics aside, there was some troubling news and if you haven’t seen the film, the Big Short, it’s vital viewing for any trader. The few smart actors were convinced the market in 2008 was due a massive correction, and Michael Burry was one of the key traders. This time in 2025, he has thrown in the towel, claiming he is no longer in sync with the market. It’s no comfort to know I’m in good company. While Scion Asset Management was one of his trading vehicles, it’s been suggested he has a substantial put position in AI. That’s a big position current stock price $175.50, P/E ratio 375. Personally I fail to see how any software company can be valued if it has no earnings and software to my simple brain is just coding noughts and ones. But then MSFT is a monopoly, maybe Palantir will be too.

Cannot verify this 100% as it’sTwitter.

Somehow it feels very uncomfortable that A.I. is such an enigma. We cannot say if it’s a force for good, a force for evil or a complete and utter waste of money. We are fed snippets from a variety of sources about the power of Quantum computing. It may be that conventional computing has had its time in the sun, but frankly I have more computing power than I need with a 3 year old Mac. Any input on this field would be most welcome but the real earnings from A.I. seem to be couched in a veil of secrecy and inter company transactions, inflating the real picture.

In The Inbox

Well a lot of irrelevant stuff this week, but I’d overlooked this from last week and I think it ‘s a worthwhile read: https://cdn.cboe.com/resources/options/Cboe_IndexOptionsGuide_Digital.pdf

My own journey was of course like everyone else, testing the waters buying shares, but in 1999 this was not a great idea. Without being able to trade options on those shares, the losses would have been dramatically worse. Index options are a great vehicle as they eliminate the issues individual stocks often have. My UK shares were NOT overpriced then!

Our old chum Larry shares his weekly wisdom: https://mailchi.mp/optionstrategist/the-option-strategist-weekly-updater-4862983?e=5f15d5ff5d Always worth a look and it’s free to subscribe.

Distraction Trades

ADA was $0.5781 now $0.5053 ( a high of $1 recently)

XRP was $2.3216 now $2.2592 So, our chosen Cryptos get a little unloved.

DAX : Yikes! totally and utterly missed the huge moves Wed,Thurs, Fri. So 2 trades, Mon and Tues nett: 160

UK Gilts Were £16.11 now £15.97 This is based on the Vanguard ETF. Again, the ‘Safe’ haven getting some love.The yield is still 4.45% not too shabby.

Legacy Trades plus new trade 440

Trade 424 High Roller

PRECIS: We start from a losing trade as below. Short calls are rarely a good idea.

Rolling Oct to Nov. 8450 call 8650 at expiry 904 and 704×2= 500, Nov 8450 call 930, 736.5×2 gives us 543, so a CREDIT of 43. We continue to take in a credit

Giving us 266 or as legacy 147.5

Our rolling debit hits a catastrophic high: 1201.5 and 1004(x2) Gives us a whopping 606.5 Debit However we are NOT adjusting but for educational purposes, we keep on rolling.

Not again! This creeping barrage of buying is annoying. But, we’re demonstrating the principle. Now 8450 call 1268 8650 call 1069.5×2 gives us 871 debit

Last week: 8450call 1226 8650call 1027.5 gives us 829 (against our credit 266 or as legacy147.5 )

Now 8450 call 1249.5 8650call 1050.5 x2 gives us: 851.5 -Expect a roll to December for credit ± 38

Trade 436 Who Knows What Next Week Will Bring?

So here’s the problem: The market tanked at the end of the day and ‘ looks like carrying on next week’. It’s a jumble sale and Friday’s closing prices may not mean too much.

Let’s go with a very spicy 3×1 using November prices. We buy the 9400 put for 124 and sell 3x 9000 put 38= 114. This is a bit spicy but we have a 400 point spread to protect us down to 8800

It still costs us 10 and spending money is annoying but the chances of the market rising and losing that 10 is minimal. It’d of course be no surprise if the market melts up, that has become the norm, after all.

Was 148.5 and 47.5 x3 = 142.5 = 6 Not sure where we go with this as the US as previously mentioned, could get really crazy

9400 put 31.5 9000put 10.5 (x3) Gives us…….. ZERO!

Was 26 and 9.5×3= 2,5 debit A sorry sight again.

Was 26 and 9 x3= minus1 Rinse and repeat the misery!

Now 12.5 and 4×3 = 0.5 Really a poor outcome, we run to expiry.

Trade 437 Calling the Top is a Mug’s game

As volatility has bumped up a bit let’s do the higher vol trade- a Strangle: We sell the 9500 call and the 9150 put for 70 each. Gives us 140 credit. Risk at 9010 and 9640

It doesn’t get much simpler than this -too simple?……..

Well that couldn’t have gone worse. 9500 call 197.5. 9150 put 14.5 Here are some ideas.

- Do nothing -and this can often prove to be the right move

- Write another strangle –put premiums are too low.

- Roll up the call side from 9500 to 9650 at a cost of 197.5- 96.5= 101

- Close out for a loss of 72 -least favourable tactic. (You could close and then sell the 9650 call as a ‘Hail Mary’ )

- Last week it’s only slightly more catastrophic 9500 call 253.5 9150 put 12.5 a loss of 126 –sorry! ( We will consider all the above at expiry or sooner)

Was 213 and 12 -Yikes! Let’s adjust and roll up the 9500 call to 9650, for a cost of 109.5 and the put to 9500 gives us 39-12= 27. 82.5 Cost (our initial credit 140, is now 57.5)

Now with no adjustment 9500 call 216.5, the 9150 put 6.5= 223 Had we rolled up the call to 8650 we’d now have 93.5 debit along with the cost 101.(Our original credit 140 remember) Ouch!

Trade 438 a Nod to Tasty’s Liz &Jenny

We seem to get burned for having upside risk so we go the Jade Lizard route. We sell a call spread and a naked put with sufficient premium to cover the call spread if it goes wrong. So, we will sell the 9700 call 72 and buy the 9750 call 51.5, giving us the bear call spread.(max possible loss 50) A credit of 20.5. We also sell the 9400 put for 31.5, giving us 52 credit. Logic of the trade? We get 52 if this expires anywhere below 9700 and above 9400. No upside risk

The 9700/9750 call spread 107 and 80=27 , and for the 9400 put 26 A loss of 1

call spread now 75.5 and 53 =22.5 9400 put 26 =48.5 (our credit was 52 remember)

Call spread is now 61.5 and 37= 24.5 the 9400 Put 12.5. WIN! ( credit 52, cost to close 37 gives us 15) We run to expiry and expect, nay, demand the full 52.

Trade 439 How To Keep Out of Harm’s Way?

Here’s a put condor: 9800, 141.5 9700, 90.5 9600, 57.5 9500, 37.5 So here’s how it works, we buy the expensive 9800, sell the 9700 and the 9600 and for protection we buy the 9500. So while we hate to spend money we will have to shell out 141.5+37.5= 179. Minus 90.5+57.5=148, giving us a cost of 31.

In the event of a market crash it’s safe as that is as likely as a UFO landing on the Loch Ness monster’s head. (We own a long spread and sold a short spread, it’s bulletproof) However there seems to be strong support at 9700. An expiry at that level would give us 100-37=61. Will the market ever give us a break? Or rather, could we do better?

Previously, those prices in order, 161, 101.5, 62.5, 39 =35 ( it cost us 31 )

This week’s prices in order 121,62.5,31.5,18= 45 ……. Win! Well sort of.

Trade 440 Let’s Go Time Travelling

We’re still in the November expiry cycle so theta(time decay) gets brutal for the near month. So we want to buy December options and sell November. Nov 9400 put, 26, Dec 9400put 73 for a cost of 47. Yes, we’re not going to do that, we’re going to buy a spread buying the Dec 9500 put for 94 selling the Dec 9400put for 73. Now we own the Dec 9500/9400 spread and sold the Nov9400 put for a small credit 5. This can, of course, make 100 assuming the Nov 9400 put expires for nothing, and the market takes a d*mp! No upside risk.

November 9400 put 12.5 Dec 9500 put 76.5, 9400put 59.5 Gives us 4.5 WIN! (not a hint of irony again)

Trade 441 Daring, Possibly Ruinous Trade

We always say we’re about teaching by doing. So here’s a trade we’d never normally contemplate. The value of the straddle (at-the money call and put) is so skewed to the next month we’re going to have fun. So Nov 9700 call and put are respectively 61.5 and 62.5, the December straddle 161 and 135. Now if the index at expiry is still at the same level 9700± the near month straddle is worthless. Would you sell it naked? What if we sold 2 November straddles and bought 1 December straddle? Cost 48 Risk at <9600 and >9800.

Try this link for the graphic https://optioncreator.com/st6thix

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com.

If there is anything you’d like help with, we all started somewhere and yes, it can be baffling. There are no stupid questions

All opinions expressed here are not to be taken too seriously and all of the trades are for educational purposes only.