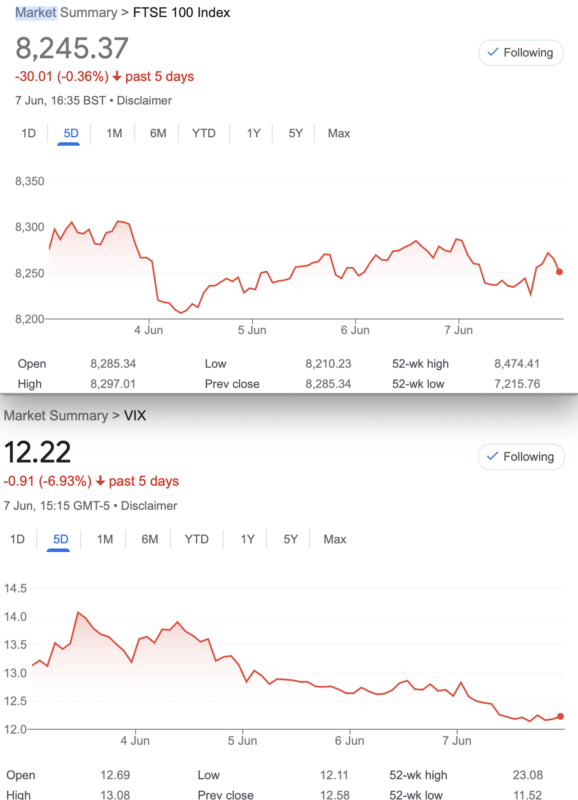

That Was The Week FTSE Started To Wobble, S&P Hits New Highs Again

So, the S&P500 hit 5375 as NVIDIA becomes worth $3 trillion. Curiously the only company worth more is MSFT. However while a chip company that makes things is a noble venture, you have to think a P/E of 70 is a big ask. Although this is nothing like the crazy valuations of the Dotcom boom of 1999 you have to ask is this a goldmine that just hit pay dirt the others didn’t find? Or, is it smoke mirrors and some mild stimulants? So, we understand that 70% of the rise in the S&P is down to 7 tech stocks, that’s a big responsibility. You have to ask also if they have any kind of monopoly on chips for AI, and even then how is AI going to evolve? So what if we asked AI to streamline its processes so it could function on a £300 laptop?

So, while NVIDIA are making chips, it seems they have a wide variety of other products but these are not the household names we associates with laptops for example. Confession here, in that I know nothing of this tech world. Gaming has never remotely interested me, it seems to be an allegory and a way of getting wins without any risk. However that is purely my opinion, having known people waste whole days playing games with no point to them. Making comparisons with trading and gaming is a mistake, but it seems the many platforms that allow trading and gambling like to draw that parallel. So are we going to see more market upheavals from tech and meme stocks? Not, with our dear old FTSE. There may be an advantage in having effectively no tech in the 100.

Interconnectedness. Are We Done?

We used to say if America sneezes, the rest of the world catches a cold. However while once there may have been a direct correlation between the US and UK stock markets for balance and comparison, we need to see the picture 30 years ago. FTSE May 1994 3127.3, the S&P 457.33. Making FTSE 7 times larger. However, this week we have FTSE 8245, the S&P 5347. So, in 30 years FTSE may have just kept up with inflation, but the US…. Well, the numbers speak for themselves. So whenever the politicians talk about growing the economy my hackles rise and I tend to mutter words like ” We still have no growth but a lot more debt”. Our plodders in oil, pharma engineering, mining and banking were never going to be huge engines of growth. Seemingly, they are the reverse. However our FTSE is our benign (hopefully) friend

‘X’ Twitter

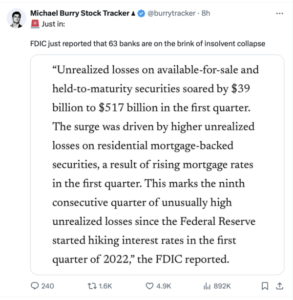

Remember the film ‘The Big Short’ ? This guy:

So, while we trade the index, on the peripherals of our world there are major events unfolding. MBS ‘s -anyone remember all this dodgy mortgages? Are we back in that world again? And, why is this info not front and centre in the financial media?

Distraction Trades

ADA was $0.4487 now $0.4414

XRP was $0.5201 now $0.4981 another ‘nothingburger’ week

DAX 3 wins total 370 1 no entry one loser -30 Now a curious week and some big moves down with our starting time at 08:00 am. So as always a stop loss of 30 and trailing stop with discretionary exit

UK Gilts were £16.44 now £16.53 Hard to contain my disinterest!

Legacy Trades 363- 367 and new kid 368

Trade363 Can we Find something not totally rubbish?

It’s unseasonal but it’s a pitchfork!

Ok so here’s the trade, and everything is wrong about this which might serve us well. We sell one call and 3 puts at the strike which is the value of the ATM straddle subtracted from the ATM (Futures) price, 8256. This gives us nothing much in the call but the put is all extrinsic value, ie if the put options expired today, they’d have no value.

We take in the premiums 271.5+ 50.5×3= 423. The dream is….. the market at 7700- 8300 for June expiry, ideally at exactly 8000!

Was: 466.5 and 18.5 x3 – not unexpected and those puts seem to be heading towards zero. Loss 0f 43 + those puts

Was: Still a loss, but we soldier on, now it’s 489, from our original credit 423

Previous week: 348+16×3 = 396. PROFIT!

Last week : 300.5+ 15×3= 345.5 Still winning but bigger!

Now 270 and 8×3 = 294. WOW! We took in 423, WIN! Profit 423- 294= 129.

Caveat -I have no entry criteria and this may not be typical

Trade 364 Back to The Knitting

So, it’s too late to use the May expiry, but June is well within the parameters (<45 days to expiry) and we again choose a ratio spread, which is a firm favourite here. However there’s a twist and a fellow trader has done a lot of homework and come up with the following. Subtract the value of the ATM straddle (8450 for our purposes) gives us ± 8200, and that is where we write the short puts. And for the longs we go 100 points above, giving us 8300/8200 put ratio. Those premiums? 41×2= 82, and 62.5. Earth shattering credit it is not, but it may be in the ballpark for the long spread to produce the goods- a max 100. Risk below 8100. We must endure such horribly, absurdly low prices for now.

Last week 48 and 29×2 gives us debit 10. Our original credit was 19.5

Last week: 75 and 43 x2= 11, our credit was 19.5 So happy days again, will June play nicely?

Now we have 49.5×2 and 90.5 =8.5 debit, our credit was 19.5 remember.

Trade 365 Calendar Ratio

Calendar time anyone? You know- sell the near month, buy the far month. We’ll do a simple comparison, between the 1 for 1 and the ratio spread, whereby we have a long spread in the far month.

Here we go: We sell the Jun 8250 put, we buy the 8350/8250 put spread in July. We have theta in our favour with a calendar, we have risk if FTSE drops below 8150, zero risk to the upside

Sorry if it ‘s a rinse and repeat a lot like 364, but as we’ll see the dynamics are different.. Oh, and the prices? Jun 8250 put 37, the July 8350/8250 put spread 88.5-61.5= 27 giving us a small credit of 10. The straight 1 for 1 calendar would cost us 88.5-37= 51.5 CORRECTION!!!!! sell: 8350 jun put 62.5, buy: July 8350 put 88.5= 26

Last week we had the debit in June: 57 and credit 38.5 for the July spread 18.5- 10 credit, gives us a loss 8.5

Was: 23.5 debit overall for the put calendar -jun short 8250 /July long spread 8350/8250

The straight one for one calendar was 127.5 – 97.5 = 30 a small gain from last week as we paid 26. Now 147-119= 28 ( we paid 26)

This week: 58.5 for Jun 8250, July spread 146.5- 96.5= 50 a tiny gain.

Level calendar 8350 put jun 119, July 146.5 gives us 27.5 -Squeaking by

Trade 366 This Takes some Cojones- it’s called a GUTS.

Here’s some fun and the GUTS trade is created as a deep ITM (in-the-money) strangle. We sell the 8000 call and the 8500 put. Think about those strikes and all points in between. At expiry they can only add up to 500. Here’s the kicker we sell those 2 options for…..542.5 So assuming FTSE does not exceed the 2 strikes at 8500 and 8000, we make 42.5* Mind boggling isn’t it!

*It’s known as extrinsic premium (where the 500 is intrinsic).

Was : 8500 put 230, 8000 call 300.5= 500.5 and we SOLD it for 542.5. We make 12, but run it of course.

This week: 8500 put 244 the 8000 call 270 gives us 514 –we sold it for 542.5

As we can only make another 14 for max profit we have gained the lion’s share of the profit at 28.5. We run it to expiry.

Trade 367 Trading in a ‘Clueless Void’

We need to be aware that volatility is not helping, the FTSE seems to be flailing like a toy kite in a storm. So, here we go with a least favoured trade, the call butterfly, but here’s the kicker, we will run two. Remember the structure? Sell the body(x2) buy the wings(the middle strike). We have A) 8100/8250/8400, and B) 8200/8350/8500.

Let’s crunch numbers: A)212,103.5(x2) 38.5,= 43.5.

B) 135.5, 56.5(x2), 16.5 = 39.

We should not do too much damage, though delta and theta are no help until expiry week.

Now: A) 178.5 71 x2, 20= 56.5 (cost 43.5)

B) 101, 31.5×2, 7= 45. 0. (cost 39.0)

So far so good.

Trade 368, finding the Gems in the Rough

There is an expression about selling options : Picking up pennies in front of a steam roller. Let’s do exactly that! We will sell a far OTM Strangle for tiny but probably low risk reward. Here’s the deal: We sell the 7900 June put for 5, and the June 8500 call for 7. We take in 12 (£120) and likely the margin required would be £2,500. Annualise that and you’re looking at 50% return. Thus, we have effectively 9 fun filled trading days to expiry. And, while this is how people blow up from time to time, it’s a set and forget until Friday 21st at 10:00am.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.