That Was The Week FTSE Advanced some more

So, once more we have a creeping advance as there seemed to be a campaign to get FTSE to be perceived as undervalued. However, there are patches of extremely good ‘earnings’. Although ‘earnings’ may not be the epithet that truly affects price. Do companies ‘earn’ their money? And, how does this all work? We can assume a substantial amount of share buybacks, but pension funds may well be piling in with scant regard for value. New money in a new tax year and the start of the month can all be factored in. While my own bias does not support FTSE higher than 8000 that is the reality and maybe the new order, as we kiss goodbye to the 7000s. https://markets.ft.com/data/indices/tearsheet/summary?s=UKX.P:FSI

Friday’s non farm payrolls played a key part as the daft money piled in at 1.30 UK time. Trading these events is for a certain type of trader. News events can be troubling, as the market can react perversely.

There May be More Trouble Ahead, but There’s Trouble now!

Levels are relative to your starting point, of course, as some legacy trades from March have been dragged along underwater, it’s clear my own positions need to be addressed. While I have no wish to go public with these ‘uglies’ I have been a very risk averse trader for decades and have been humbled by taking my eye off those short calls. However, the weekend is a good time to think things through. We conduct ourselves better when not under the cosh.

Adjusting Trades That Went Wrong

Options are tools for trading, and a good understanding of your positions is key. We need to know our exposure in terms of Deltas to start with. Being a monitor of Delta neutrality can be an ordeal on a day to day basis. Say the market swings 1% your .50 deltas in the straddle as in 362 now become .40 and .60. We get another rise of 1% and now things are quite skewed. Dynamic hedging with futures may be some people’s idea of fun, but for yours truly I always assume a position is likely to go against me. (Futures are a different animal). I use a ballpark figure as to what I can live with, and this is possibly the hard part. Knowledge is only a part of trading, establishing your style, and attitude to risk management, that takes time.

As in trade 362, the values of those straddles have changed. Remember a straddle is when you sell both calls and puts at-the-money. In theory these are pretty much o.50 Deltas on each side. Puts have negative delta, Calls positive. So trade 362 sees not only the value of the straddles we bought dropping, due to theta, it’s now skewed to the upside and this can pull out volatility. We have a double whammy. So, how do we adjust?

Factors in Trade Adjustments, Delay the Agony?

How big is your account relative to your positions? What is your margin? This brings us to position size, and there are many who freely lecture us on the evils of overtrading. So, we cannot ‘get out of jail’ simply by selling more options, unless there are other factors in play, like a fat wallet. As in 362 we owned the near month straddle, and in isolation we might think about how much it has lost. It is not a catastrophe but clearly without a huge move it is just going to lose value. Had we sold it, we’d be happy with the handy return 173-140= 33 profit.

So, 2 sides of the coin, is our position under pressure due to sold or bought options?

Short options can get ugly very quickly and you have to take a view. Will the market continue its chosen direction, is a reversal likely? Can the account stand selling more options at strikes further away from the money. Can I roll up and out into further months? Should I use another strategy, or convert into something else?

Long options can lose value over time and being right on the market can still incur losses, even if you bought when volatility was low. Trading naked and swinging for the fences is not a winning strategy. Sometimes seeing a trade’s value dwindle is harder to bear than seeing losses mount, when we know time decay is our friend.

Adjustment needs calculation, understanding of risk and the many possible pathways to profit. Losses hurt and while many of the trades here are from my own personal account, some of the quirkier ones are not. I’m really not that terrible!

Distraction Trades

ADA was $0.5132. now $o.4682

XRP was $0.5130. now $0.5321 Finding its lost superiority over Cardano?

DAX Dismal week matching my other positions! 2 losers -30 x2 one no entry one break even +30, and May 1st DAX was closed

UK Gilts were £16.40. Now £16.53 Ugh! Interest rates may not be going anywhere for a while yet, a tiny improvement.

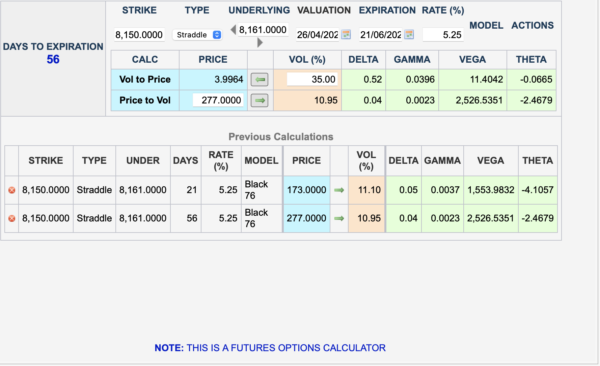

Legacy Trade 362 and new kid on the block 363

Trade 362 -Could We find Something Novel?

An interesting feature of the CME calculator is being able to plug in the price of a straddle. So what’s the idea here? Let’s try the curious 3 x2 ratio calendar straddle trade. Those with a long memory will recall this is an allegedly highly successful trade as invented by a Dr. Singh. A huge caveat: I have not discovered the entry criteria for this trade, but you may recall we buy 3 near month and sell 2 of the far month straddles. The theory is that while theta is ugly against us, Gamma and therefore delta are in our favour so any big move should produce a decent profit. In effect this trade is a free ride with a straddle. The numbers: 173×3= 519, 2x 277= 554. We therefore take in a credit of 554-519= 25.

An interesting feature of the CME calculator is being able to plug in the price of a straddle. So what’s the idea here? Let’s try the curious 3 x2 ratio calendar straddle trade. Those with a long memory will recall this is an allegedly highly successful trade as invented by a Dr. Singh. A huge caveat: I have not discovered the entry criteria for this trade, but you may recall we buy 3 near month and sell 2 of the far month straddles. The theory is that while theta is ugly against us, Gamma and therefore delta are in our favour so any big move should produce a decent profit. In effect this trade is a free ride with a straddle. The numbers: 173×3= 519, 2x 277= 554. We therefore take in a credit of 554-519= 25.

However, this is not free money as we have to buy back the entire position when and if it makes money.

https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html

Now? Very ugly and I suspect the problem is with the choice of May/June as opposed to say June/July, in addition to the market ‘s upwards move. (NO!) We have 140 for May straddle and 261 for June. So, mix it all up and we have a loss of 102. Minus our credit 25

Trade363 Can we Find something not totally rubbish?

It’s unseasonal but it’s a pitchfork!

Ok so here’s the trade, and everything is wrong about this which might serve us well. We sell one call and 3 puts at the strike which is the value of the ATM straddle subtracted from the ATM (Futures) price, 8256. This gives us nothing much in the call but the put is all extrinsic value, ie if the put options expired today, they’d have no value.

We take in the premiums 271.5+ 50.5×3= 423. The dream is….. the market at 7700- 8300 for June expiry, ideally at exactly 8000!

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.