That Was The Week, Holidays Never Last

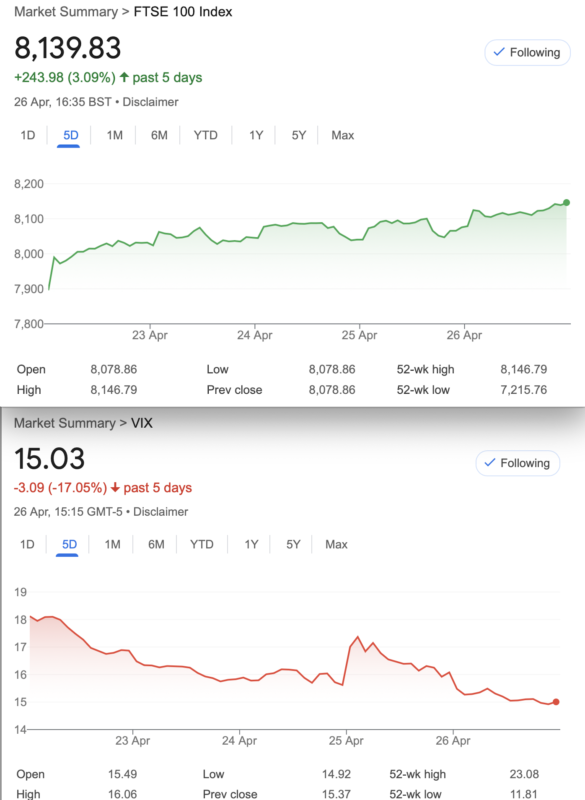

So, back to a delightful 7ºC and a grim soggy Britain. And, being short, the week’s activity made this trader quite uncomfortable. However the nature of the positions means that there are some mitigations with longs v shorts. Sometimes the market comes back to bite you, burn down your house and steal your car! My own personal view of the resistance at 8100 did not hold good, but it’s just a view. I am not the arbiter of the market’s behaviour and to be humbled is to be a proper trader.

So what the heck happened? FTSE is cheap they say, well nothing changed and it was not considered cheap when it was 5% cheaper! Boldly going to new highs makes this cynical old duffer highly suspicious and A.I. may have had a hand in this. FTSE seemed to start the year at around 7450 and crept up like a timorous wee beastie, then retreated, until the ‘BTFD’ crowd Bought The F******* Dip. We do not need America’s hysterically optimistic valuations here, thank you.

Vix has dropped back but seems to be alert to the dynamics of world events, financial and other.

Holiday Perspective

It’s interesting that switching into ‘holiday mode’ means not taking the news in such large doses. The BBC was happy to oblige with their watered down ‘jolly nice’ news channel interspersed with the odd advertisement. We were made aware this is probably a more or less free service for those of us who venture beyond the Isle of Wight for a sojourn. Market action was bizarre as every dip was met with increased buying. Auntie BEEB was rather casual about it all. Is the economy and the UK market doing that well? The cynic in me says of course not, the trader says ‘no idea’ I just trade the thing. One outstanding feature, however, was the extreme weather. Summers may become intolerable in those places we used to call ‘sunnier climes’.

Distraction Trades

ADA was $0.5137 now $0.5132

XRP was $0.5432. now $0.5130 Finding parity with Cardano?

DAX 4 no entries one win +150

UK Gilts were £16.61 now £16.40 Yikes! Bonds have been getting spanked again

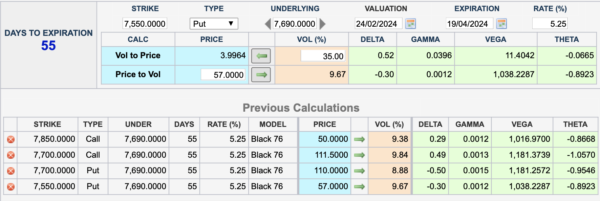

Legacy trades from 355 and new Trade 362 From Expiry Friday 19th April @7823

Trade 355 SIC Short Iron Condor.

In a nod to another options website/blog, this is a curious trade as it should not work. The presenter claimed it had made more than a strangle or a calendar trade in a week. This is a short iron condor, so we are buying the ATM options and selling the outer wings. We choose April expiry which gives 55 days to be wrong. The trade shown was 49 days from expiry, and the strikes were a little different, but let’s give it a whirl. We buy the April 7700 call and put and sell the 7850 call and 7550 put. Those prices: 111.5+110= 221.5 minus 50+57=107, gives us a debit (ouch!) of 141.5. However, the prospects of this trade winning are not zero, but flippin’ close.

Caveat: people make a living trading normal iron condors.

APOLOGY! Typo- the cost was NOT 141.5 it was 114.5. .

The 7700 straddle 84.5, 115.5 = 200 7850 call is 33.5 7550 put 55.5 =89. Our trade is now 200-89= 111.

However, with any trade you really don’t want to see that premium melting away. Thus we run, for fun and the unexpected.

Was- 112.5 -it’s never going to be profitable but we did not choose entry using any particular criteria.

WAS: 7850 call 133 7700 call 257 7700 put 15, 7550 put 7. So, we OWN the 7700 straddle 257+15= 272. We SOLD the wings 133+7 =140 gives us 132. Profit 17.5!

Was : the 7700 straddle 277.5. the 7850 call 138.5, and the 7550 put is 5.5. 277.5-144 =133.5 A little more profitable

Was: UGLY! The straddle is now 228, but the wings are 129.5 and 7= 91.5 Losing

Now WIN!!!!! 142 note: probably wise to close out but we run it of course.

At expiry: 123 A lot of sweat for very little.

Trade 357 The April Expiry Cycle Beckons

Despite the many winners we also like to show other trades in all their splendour. However nothing works as well as real prices in real time. So instead of cherry picking another winner we go with an old chestnut, the Butterfly. What’s the problem with the ‘fly? You have to be right in a narrow range, but there is of course a huge choice in risk/reward. We like quite a wide ‘fly and the strikes we choose for our Put butterfly 7800/7650/7500. Remember we sell the body and buy the wings. Our prices 7800 177.5, the 7650 is 91 (x2)and the 7500 is 43.5. 182- 177.5=4.5, deducted from the 43.5= 39. Max profit at 7650 is 150 -39= 111. However our risk is no more than the 39 premium paid.

We could reduce this and buy a lower wing as the 7450 put is 34. That would give us a broken wing butterfly with lower cost but risk increased by 50.

Max reward, ( the difference between 7800 and 7650) 150- 29.5 =120.5, max risk 84.

Was 32.5 – Don’t hold your breath!

Then, 7800 put is 28, 7650 puts are 11 the 7500 put is 6. Gives us 28+6= 34, minus 11×2 =22. Ouch! It’s only worth 12 and while we have never liked butterflies we run it.

So, 23.5, 8.5 x2, 4.5 =11. Ouch, again

Last week 41- 212.5×2= 16. Horrible!

Even worse now worth 3.5 Doubtful there’s any coming back from this but we run it and risk threepence ha’penny!

LOSER!

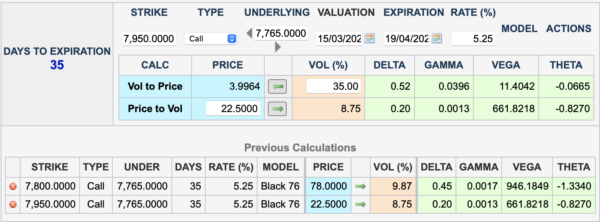

Trade 358 Bonkers Trade

We’re going to do something totally wrong. This is the trade that destroyed a hedge fund. It’s a 3x 1. ( a three by one) not a recognised* trade. We sell 3 further OTM calls and buy one call OTM but nearer the money. Here’s what we have: We buy the 7800 call for 78 and sell 3 of the 7950 calls for 22.5 x3= 67.5. Thus our cost is 10.5 and we expect the theta to help us out in a big way.

In the event of FTSE hitting >7950(heaven forbid!) we have a lot of juice in the tank from our long 7800 call but it could get scary. (Calculator uses the Future price, note.)

The 7800 call is 170.5 and the 7950 calls are 74.5 x3= 223.5 We are nursing a loss of 53+ our cost 10.5 Ugggly!!!

We run it and hope( that’s not a strategy) that the market fades, while we are in our golden zone. Expiry this week would be peachy for this trade.

Previously: 177.5, and ……. 75×3 gives us 225-177.5 =47.5 LOSS We’ll run it and show how to repair such a lamentable trade!

Last week 129.5 and 44.5 x 3, gives us minus 4

Now, 83×3 and 207. Minus 42 but…. we run it as Monday may be the big down day

Trade 359 Come On, This High Looks Suspect. (Ignore my massive bias!)

While that might express my opinion that is not tradeable. I’m pretty rubbish most of the time, and definitely lost the plot + vat this week.

OK, let’s take a ‘punt’ here and do a synthetic short. We sell the 8000 call for 53.5 and buy the 7900 put for 58.

Previously the call is 52.5 and our put 49.5

Previously 28.5 and 72.5 YAY! WIN 44-4.5=39.5 profit Or as they say in the share tippers world 877% ( It’ll pay for the bonkers stuff we tried this month)

We will run it but that’s a healthy profit and highly directional, it would have been ugly this week

At expiry this would have given us 23 Modest WIN

Trade 360, are we calling the market’s bluff?

While the volatility is shockingly low it’s no fun to be selling puts So, in search of something to trade, let’s look at a strangle. Naked, yes, but playing Both sides of the market we sell 8100 call and 7800 put for 23 and 23.5 respectively. Our risk is now at 8146.5 and 7753.5 -logic of the trade? 15 days to expiry, and the downside does not seem to be under any pressure………. Yet!

This week 10 and 35= 45 we’re in credit for 1.5!

Now, 19 and 7.5= 26.5, gives us 20 credit. WIN!

We’d take that all day long but again, run for fun (TastyTrade recommend closing out at 50% of max profit)

Running to expiry was a losing strategy. ( Anyone detect a theme here?)

Trade 361 Something for May ( Aren’t we supposed to go gathering nuts?) No, apparently

This is a highly favoured trade and uses theta and the protection of a long spread. By now you are all familiar with the term ‘calendar spread’ whereby you sell the near month option and buy the far month. Here’s the twist: We buy a long spread in the far month, thus reducing our cost and perversely managing a little risk against the market flying upwards.

So, we sell the April 7750 put for 24.5 and we buy the May 7850/ 7750 put spread for 95-61.5= 33.5

Logic of the trade? If it goes wrong, ie a huge drop, it’s not hard to repair , and if the market smashes up we are unlikely to incur a loss

CAVEAT: When the near month option expires it becomes a new trade, be sensible.

Now those numbers 7.5, Apr 7750 put and the May spread- 54.5 and 35 =12.( We paid 33.5-24.5= 9 )

At expiry the 7750 put went out for zero, and the spread was probably around 50

——————————————————————————————————————————————————————————-

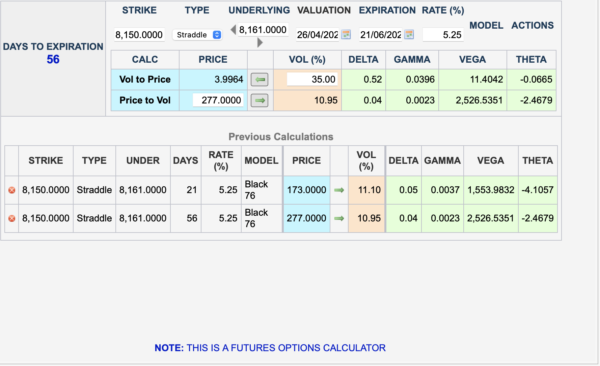

Trade 362 -Can We find Something Novel?

An interesting feature of the CME calculator is being able to plug in the price of a straddle. So what’s the idea here? Let’s try the curious 3 x2 ratio calendar straddle trade. Those with a long memory will recall this is an allegedly highly successful trade as invented by a Dr. Singh. A huge caveat: I have not discovered the entry criteria for this trade, but you may recall we buy 3 near month and sell 2 of the far month straddles. The theory is that while theta is ugly against us, Gamma and therefore delta are in our favour so any big move should produce a decent profit. In effect this trade is a free ride with a straddle. The numbers: 173×3= 519, 2x 277= 554. We therefore take in a credit of 554-519= 25.

An interesting feature of the CME calculator is being able to plug in the price of a straddle. So what’s the idea here? Let’s try the curious 3 x2 ratio calendar straddle trade. Those with a long memory will recall this is an allegedly highly successful trade as invented by a Dr. Singh. A huge caveat: I have not discovered the entry criteria for this trade, but you may recall we buy 3 near month and sell 2 of the far month straddles. The theory is that while theta is ugly against us, Gamma and therefore delta are in our favour so any big move should produce a decent profit. In effect this trade is a free ride with a straddle. The numbers: 173×3= 519, 2x 277= 554. We therefore take in a credit of 554-519= 25.

This is not free money as we have to buy back the entire position when and if it makes money.

https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.