That Was The Week FTSE Stank!

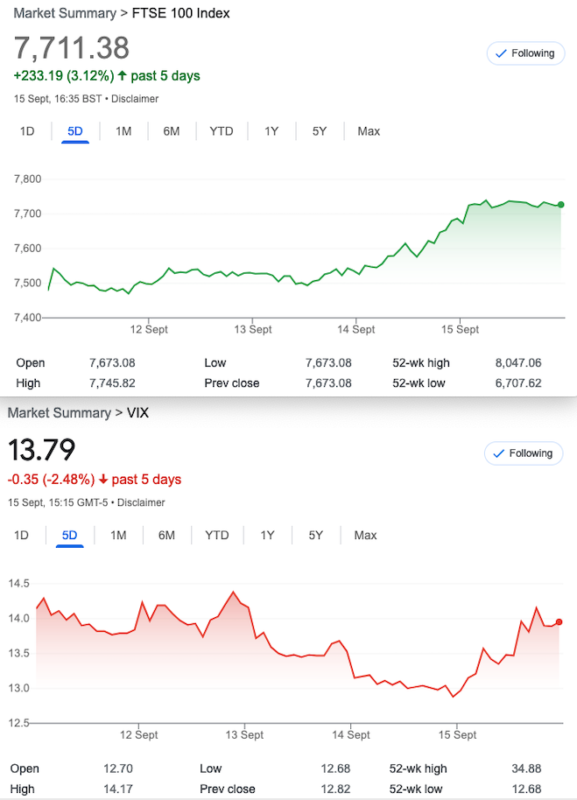

So what’s going on? Who stood to gain from the massive rise in the index? So firstly, let’s look at the news. Interest rates are going up again, yet that may be the end of the rises. Personally I think that’s irrelevant, as nearly all FTSE companies are international and the US was basically flat this week. Eurostoxx? A modest 1.37%. China’s economy ‘improved’, and the UK had a fall out about Chinese spies in Parliament. UK GDP? DOWN again! So, for the life of me I seen no reason to throw £70 billion into our crumbling concrete, striking economy. Maybe there’s something else?

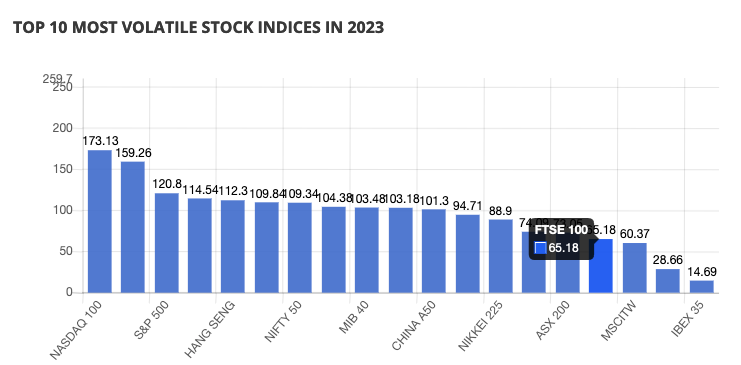

Let’s look at the real numbers FTSE against our old barometer S&P500. First up, this graphic:  As you can see FTSE has comparative Vol 65 while the S&P is 120. Next let’s look at expiry week volatility over the last 11 months, and total vol for FTSE 11.44% against S&P 6.25%. Anyone else think this might be an insight into a whole other paradigm? I should add, I am very miffed as I took a big hit this week* and call BS on the FTSE, so maybe it’s my prejudice, but if I can see glaring inconsistencies without really trying, maybe there’s more to it.

As you can see FTSE has comparative Vol 65 while the S&P is 120. Next let’s look at expiry week volatility over the last 11 months, and total vol for FTSE 11.44% against S&P 6.25%. Anyone else think this might be an insight into a whole other paradigm? I should add, I am very miffed as I took a big hit this week* and call BS on the FTSE, so maybe it’s my prejudice, but if I can see glaring inconsistencies without really trying, maybe there’s more to it.

Calling BS

I was drawn to an article that calls BS on the S&P. How so, you may well ask. I recall the article stated that, and this dates it somewhat, there had been only 2 other examples in decades of the US index going >91 days without a 1.5% move. For 91 days, now read 160. I urge everyone always to verify my ramblings. However, it’s no great demand on your time to check the data,and then explain how the heck the FTSE is half as volatile as the S&P? While we like to use Bollinger bands on some indexes including the VIX as they show vol squeezes, that’s not happening. Of course if trading was a matter of spotting such things, we’d all be billionaires.

I call BS on this week’s action, being a quarterly expiry in the same way as March was. That was also off the scale suspect. Check out :308 17 Mar Bloodbath at the Bank. I posted someone else’s smart thinking about options expiry, and hey, if you’re on course to lose £71 billion, why not spend £70 billion to get a cool £1billion? Algo’s ? AI? We used to expect expiry week to be a big non-event while non farm payrolls were the big market shaker.

By the way the S&P has gone > 160 days now without a move >1.5%. FTSE?…………………………… 6 such days. That’s six.

* In fact I have been very unwell and normally (as in the mad March expiry) I would close out any positions going into expiry. I didn’t and got hammered.

Apologies:

As stated I have been very unwell this week so took a double hit from missing some much anticipated fun events, and watched my account swing wildly by 5 figure amount, in basically one day. I’m still very annoyed, and feel lousy!

Distraction Trades

ADA $0.2501 disappointing

XRP $0.49979 drifting/ flat

DAX 3 no entries one break even +30, one win +100

UK(Vanguard ETF) Gilts: £16.34 last week, now £16.36

Those Legacy Trades and Now 334, Can We Stop Winning? No!

Trade 328 Put Spreads, the Long and the Short

In conversation with a very smart, and risk averse trader, his research had led him to an interesting proposition. Seemingly the max theta is to be found in the 20/13 delta spread. Combined with TastyTrade’s 45 DTE(days to expiry) this is the optimum place for a short put spread. Let’s see the graphic:

We were a little late to the party but perhaps that’s fortuitous, given the drop this week. So the short put spread, selling the 7250 put (delta 20) and buying the 7100 put (delta13) gives us a credit of 16.5. Now I’m going to be Devilled Avocado here and say I’d rather go with a put ratio spread. But it’s important to understand the difference. Margin for both trades will be required but fixed for the short spread and bigger and variable/possibly brutal for the ratio spread. A big drop would see the ratio spread in trouble but the ratio spread doesn’t get ugly until 6950.

Last week we saw : 39.5 and 24 ( started at 45 and 28.5) so the credit spread was a tiny credit of 1, the ratio spread took in 12, now 8.5 -early doors of course.

Last week :The straight spread=5.5 the ratio spread gives a Credit 1

Now: 7250 put=4.5 and the 7100 put= 2 So it is a win all round and the straight spread here actually did fine,making 14, while the ratio did at best 17.5 IF we had taken action 2 weeks ago. Not the same trade, remember.

Both trades WIN Arguably the ratio spread could have been closed out for a tiny credit

Trade 330 We Don’t Take a Loss Lying Down

We carry on the position and break the golden rule: A calendar trade runs at best to expiry, anything else is a new trade. So let’s say we are in debit 255 we own a 7500 put. How can we redeem this position? MAJOR ALERT: We NEVER accept a big loss, we always look to mitigate this with a new expiry month. Here’s what we do: We sell 2×7650 puts, and buy a 7800 put. You’ve guessed, right? We now have a bulletproof rock solid 22 carat gold butterfly. Those prices for the 7650s we get 383.5×2= 767, we pay 528 for the 7800 put. Gives a credit 239, and our loss was 255. So, we are in a loss of 16, but wait………. we OWN a huge butterfly with max poss gain of 150.

Last week: Of course there’s no free lunch, our butterfly is currently worth 16 but Trade 329 cost 57 and we want it back!

Losses.

Can we make good? We need the market to rise in the next 4 weeks. Likely? Who knows, but our position cannot worsen much, we are locked in safely.

Was 173, 302(x2), 446.5=16 exactly the same as last week!

Was: 7800 put =321, 7650s 180.5(x2), 7500 put 71 Gives us 31 Credit

Last Week: 7800 put 315, 7650 puts 169.5 (x2)=339. 7500 put 56 Gives us 32 Credit (Remember we want to get our 57 loss back)

Now: FTSE expired at 7720 which makes our long 7800 put worth …...80 WIN!

Trade 331 Futures Go Skywards After The Cash Close (7375 )

We have seen this before but does it presage a rise on Tuesday? Let’s get bullish and BUY the 7375 /7475 call spread(74-35) and sell the 7200 put(36) to pay for it, minus 3. Logic of the trade being that the next couple of weeks may be positive, and the trade could make 100 for a cost of 3. We reckon there’s support around 7250, but we are selling a naked put if things do go south, the call spread may not be a lot of help. Again we could have some valuable education with that.

Last week: 7375call=132, 7475 call 65, and the 7200put=7.5. WIN! 59.5 -3 trade cost=56.5 Close out for big profit, run for fun to expiry. So, we’ll take that, and watch to see if it does make the max 100.

Last week: the call spread = 125- 53.5 =71.5 and the 7200 put now 3, plus trade cost 3 gives us 65.5 Profit

Now? 100 profit WIN!!!!

Trade 332 Let’s Break Something

Here’s a fun trade with 2 naked elements, a risk reversal. We sell the call and buy a put. 7600 call for 20 and the 7350 put for 21, costs us 1. So, some may scoff and this really is not recommended but the logic of the trade is simply this: We have had to date 99 up days and 74 down days and the old logic was that if this got too out of wack you’d go that route. So, a surfeit of up days tells us to go short. OK, hands up, there’s no real logic to this but let’s see where it goes.

These trades made ££££ in 2008/9

and the joke was, we’d wait for 2 consecutive up days if there were such a thing, to place these. Since then aside from the obvious 2020, we’ve seen an endless stream of BTFD.- buy the freakin’ dip

Best we could do was win of about 20, WIN!

Trade 333 – Triple Nelson Should we be Scared?

It’s expiry next Friday and we need a calendar trade but don’t want to get too ugly. We BUY a 7550/7450 October put spread and against it we SELL a Sept 7450 put. Those prices: 135, 91 and 34. Gives us a debit of 10. We hope the spread is worth >10 at expiry and the Sept 7450 expires worthless. So, we will have fun adjusting if it goes to h*ll.

Now: 38 and 24.5= 13.5, and it cost us 10. A fund manager would claim 35% profit! We will now morph this into something new.

Trade 334 Picking up our Legacy Trade

We have a legacy of a long October 7550/7450 put spread, currently worth 13.5

Let’s look at:

1.Convert the trade into a 7750/ 7650/7550 put butterfly. We buy the 7750 put for 98.5, sell TWO 7650 puts 61.5, giving us a credit of 24.5. And magically that buys back our short 7450 put.

2. Convert to a put ratio spread by selling another 7450 put, giving us risk down 5% out of the money at 7350, it’s now a credit trade for 28 with a shot at collecting a further 100 if the FTSE takes a tumble.

3. Sell a 7350 put for 16.5, giving us an overall credit of 10 but risk now at 7250, with the chance of a max 100 points extra.

4. That’s enough! Yes we could do allsorts with calendars, condors et but let’s keep it as simple as your frazzled (this week) author

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.