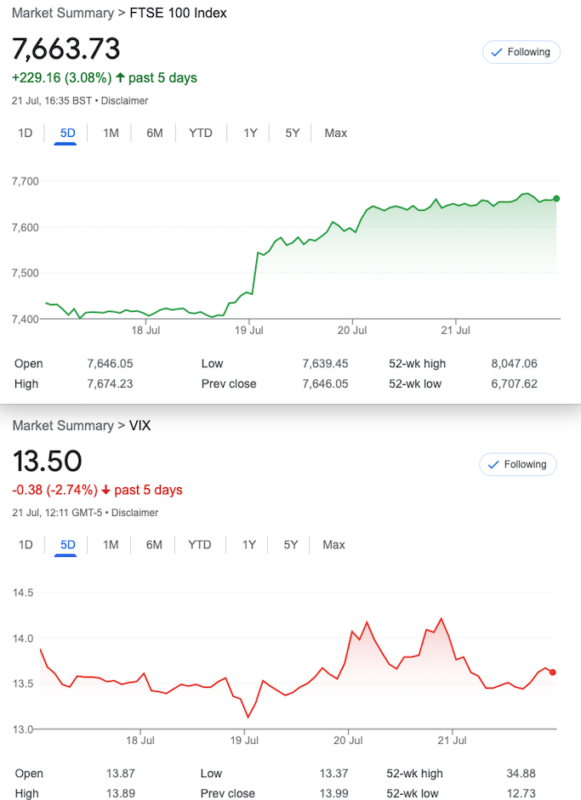

That Was the Week, An Oligarch’s Sanctions were lifted and then FTSE smashed Up!

CPI, an inflation metric much watched, in recent times dropped this week. The market went nuts, the FTSE250 up almost 1,ooo by Thursday, either fuelled by oligarch cash( who knows!) or the bizarre idea that money will once again become free/cheap as interest rates moderate. Quite why any company in the index has such sensitivity to debt, to my mind, does not bode well. Should a good business actually have any debt, while not growing? GDP is contracting and we may soon be in recession. Permabears like me always assume the gloomy outlook. The yield curve* is heavily inverted and always presages a recession.

So What Happened This Week?

Expiry was unexpected at such a level as this is the second week FTSE has shot up. Metrics such as P/E ratio tell us it is fairly valued, one of my favourite indicators however is the up/down day count . Currently we’ve had 84 up days, 60 down and it used to be that 51% of days in a calendar year would be up. So, while I have a clear bias to the downside I tend to look precisely for such evidence. 2/3 of the time the market does very little, so to have no expectation is the answer, any bias is based on a belief. And we recall the late Van Tharp’s words: We trade our beliefs about the market. Americans always seem to be so much more optimistic, and the growth in the US economy would justify that. We are just tired old Britain!

CAVEAT: We are not recommending trades or a view, these are just musings for education, and fun.

Distraction Trades

ADA $0.3211 a small decline

XRP $0.76767 was $0. 71818

DAX Rubbish week! 3 no entries one loser -30, one break even +30

UK Gilts U.K. Gilt UCITS ETF (VGOV) £16.63 was £16.37

Trades 321-325 Expiry Time, 3 wins 1 small loser, 1 ongoing and new Trade 326

Trade 321 in a flat low vol market- Yikes!

Let’s get spicy in this season of low volumes low volatility and low expectation of actually having a smart trade. Theta is not our friend. So,we look to take on more risk and sell more options than we buy. Here we sell 2x the near month, July strangle 7400 puts,(24) 7825 calls(24), and we buy one August strangle: 7400 puts (55.5) and 7825 calls (44.5) .Here’s the numbers: 55.5+44.5= 100 and 24+24 (x2)= 96. Our cost therefore is 4

WIN! 7400 put 28.5 7825call 23=51.5- our cost 4= 47.5 We could have maybe got a little more as expiry was 7650

Trade 322 Some Movement but Volatility Being Supressed

Again we can only use theta in this ludicrously low vol environment. It is a concern but if we take a real plummet, we will at least be able to morph/adjust/roll. The above calculation: https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html?utm_source=LINKEDIN_COMPANY

We are doing another old chestnut, the put ratio spread. Buying the 7500 put and selling the 7350 put twice. Cost:90.5-44×2= 2.5 Logic of the trade? We have risk down at 7200, and we may find this trade in profit quite quickly above that level, even if we have a blip up to 7600 or so. Should the FTSE dip lower than 7200 we will adjust, if the market shoots up we have no risk other than our tiny 2.5 debit

Last Week: 7500 put– 69 and 7350 put 10.5 (x2) Minus cost to open 2.5 Gives us a profit of 45.5 -again we’d take that but ‘run for fun’

So, run for fun produced a big fat zero but we would have happily taken 45.5 WIN!

Trade 323 Horrible Trade- Let’s Do it!

We will place the much acclaimed ‘broken wing butterfly’. By way of explanation, the ‘broken’ part comes from the cheaper wing strike being further out. So instead of say 100 point wide 7450/7550/7650 butterfly (using calls here) The 7700 is bought instead of the pricier 7650. I wonder if it makes sense. And will it work?

We buy the 7450 call 131, sell two 7550calls 63.5(x2) and we buy the 7700 call for 13.5 Thus our cost is: 17.5

Note: The 7650 call was only 23.5 so this is bonkers, IMHO!

This week: 9.5 3×2 and 1.5. =5 So as if to confirm our bias against these, the numbers are horrible but we might as well stick with it

Those prices now: 36.5 7.5 1 Remember the ‘body’ 7550 strike is x2. Thus even with this horrible strategy that cost us 17.5 we have 22.5 a tiny profit

As expected this was a LOSER at expiry BUT,……. on Wednesday we saw the following prices: 7450 155 7550 63(x2) 7700 4 =33 WIN!

For us we cannot asse any upside with this trade but clearly it was possible to make it profitable closing out during expiry week, so perhaps it’s unfair to dismiss it completely. We may return to this in future.

Trade 324 Smart Trade? Probably not.

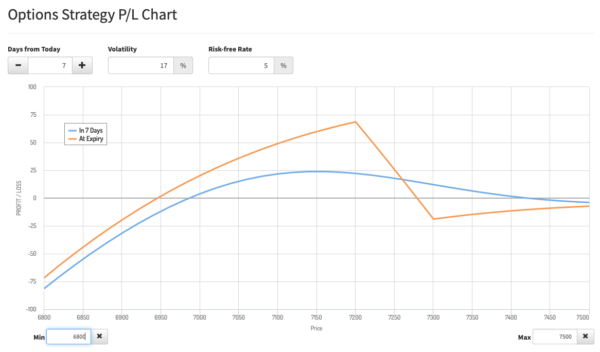

This is a huge ask, but I’ll try a reverse calendar, in the absence of a smart trade! We sell the August 6900 put 40 and buy 7300/ 7200 July put spread 88.5 -45.5= 43 So our cost is 43-40= 3 Logic of the trade? We want to own the Put spread but don’t want to pay for it. The trade makes a profit in various scenarios but there’s always the chance the market will tank. But if our spread hits the max 100, we then have a ‘war chest’ to adjust. Here’s our P&L

Here’s the link to the calculator: https://optioncreator.com/stqx435

At expiry a loss of 5.5 it was wildly optimistic. LOSER!

Trade325 An Old Chestnut

In the absence of fair looking trades we go for a call ratio spread. Thus we have some directional bias and a fair chunk of mitigation if we’re wrong. We buy one August 7500 call for 57.5 and Sell 2x 7600 calls 27. Our cost to enter is thus 3.5 which is cheap as chips, and the logic of the trade? We have theta on our side by selling two calls against the one we bought.

HORRIBLE! However this is a gift as it gives us a chance to look at how to manage a losing trade, and to say we have options is an understatement.

7500 call 182.5 7600 call 112.5 = 42.5 LOSS

We can make the following choices ( trying not to say options!) Though this is not the sum total of ALL possible actions of course

- Do nothing, and as Price Headley says more often than not, you make more money sitting on your hands.

- Roll the 7600 call to Sept, pay 112.5 for Aug7600 call sell Sept 7675call 115.5. Credit 3

- Buy 7700 call, for 60.5 creating a butterfly, sell Sept 7800 60.5 Zero cost

- Close out the spread for 70,buy the extant short 7600 call, sell 7750 call for 42 Zero cost

- Close out the spread for 70, buy the extant call by selling a strangle: 7550 put 59 and 7700 call 62.5. This then gives us a’warchest’ of 70 with which to adjust

- Create a 7700/7800 call ratio spread 60.5-28×2= cost 4.5 We now have risk at 7800, and a butterfly with max poss 100 reward (watch your margin as you’re now effectively naked short 2x 7800 calls

Trade326 Upside Risk- Let’s Take on Mr. Market

In our volatility drought we are limited to boring calendar/ time spreads typically. We will go with a combo, a combination known as the risk reversal. We will sell a call to pay for a put. August expiry we sell the 7800 call for 28 and buy the 7400 put for 28.5. The logic of this trade is that with so much upside recently, one good down day could give us a healthy profit. Should FTSE decide it’s all clear blue skies, we can adjust, somewhat.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.