That Was The Week- Quad Witching, Vix Drops(again) 4/4 Trade Wins.

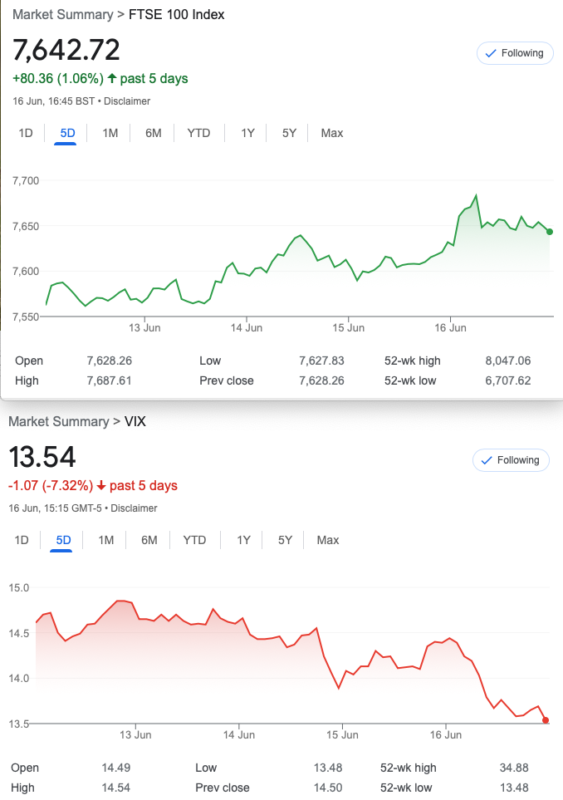

A curious week as world politics sees disgraced ex-leaders accusing everyone else of being deluded. As traders we can accuse the market of delusion all day long but, it’s not helpful. We ran trades to expiry (level not available to the public apparently). We think expiry was around 7650, as you can see it was a real piece of nonsense!

There is a worrying trend of mass call buying* I’m told. 0DTSEs are weapons of mass wealth destruction, and in our opinion make a mockery of options. In truth they are binary bets and should not be a part of a proper trader’s armoury. Gamblers, however may wish to pile in. We hope for us UK retail players options remain monthly, though weekly options are traded here. Market makers and options brokers are a dwindling force and it’s no surprise with regulators making life difficult all round. Odey asset management closed down due to sexual harassment. I think personally this is over reach by FCA as it’s not a financial issue. However that is how things are.

*Retail traders cannot short stocks so they will buy calls en masse to move the underlying, and it’s happened before via Reddit. I find that worrying, personally.

Stock Fever

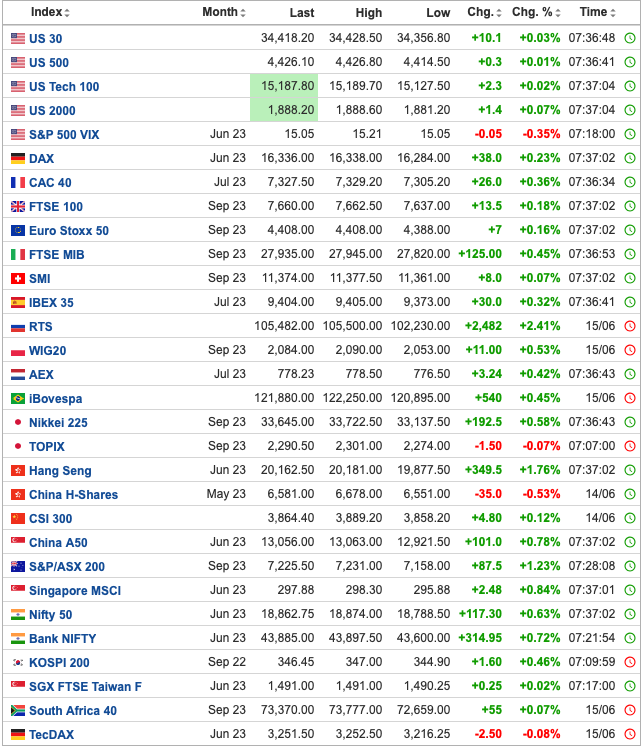

The above makes me feel ever so slightly ill! My natural bias is to the downside. I am cynical and coined my own mantra ‘Markets rise on lies and drop on truth’. Harsh, I know. Russia’s stock market seems to be on the rise, it’s a really quirky world and maybe sanctions are in reality, phantoms. Red seems to be somewhat in absentia in that list, but of course Vix is in terminal decline, for now. We should buckle up and buy far dated puts for the inveitable. Theta is of course the enemy and we need to compensate for that. Spreads of all varieties come into play. We are not desperate to take anything costly, however.

Distraction Trades

ADA $0.2675

XRP $0.4790 Crypto’s are becoming yesterday’s news and the scandals continue.

DAX 2 wins 2×100, two losers -30 x2, one no entry

We are looking at U.K. Gilt UCITS ETF (VGOV) It’s now £16.41 from an all time high of £26.75. Last week it was £16.60

Legacy Trades from Jun Expiry and New Trade 321.

Trade 317 It Was A New Expiry Month

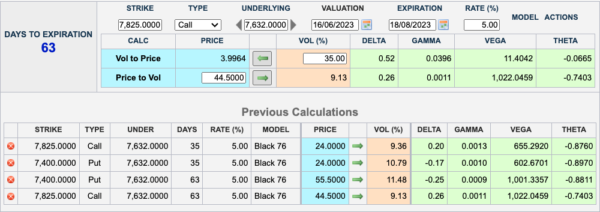

A homage to Liz and Jenny once more as we borrow from the esteemed Tasty Traders, the strategy known as the Jade Lizard. This trade has no upside risk, as we perceive the danger may lie that way. June expiry. We sell a call spread: Sell the 7800 call for 68.5 and buy the 7850 call for 45. We sell the 7550 put for 27.5. Maths scholars will note the call spread credits us with 23.5, add this to the credit for the put we sold, gives us 51. Figured out the upside potential loss? It’s the value of the call spread,which is 50. Downside risk at 7550 minus the credit 51= 7499

Last week: So, the drop was unexpected but we now have 53.5 for the 7550 put and 7.5 for the call spread. Gives us: 61, a loss of 10. I had messaged during the week about my concerns and possible adjustments, then this appeared somewhere in my ‘net travels:

To quote from last 2 weeks: Adjustment should not be a knee jerk, we need a plan. So where are we? 5, 2.5 gives us 2.5 for the 7800/7850 call spread and 35 for the 7550 put. The trade was tenuously in profit and it might make sense to close out the call spread, as it’s only 2.5 but let’s keep it straight.

Last week- looking fine: the call spread is 2-1.5= 0.5 and the 7550 put is 35.5, so we’re in profit 51-36= 15 -it’s not over yet.

WIN 51!

Trade 318 Time for One of Our Hybrids

We are going to sell a put in the June series and buy a put spread in the July series. June 7400 put 28.5 July 7550 put 101 and the 7400 put is 70. So we pay 101 for the 7550 put and for the 2 puts we sell, we get 70+28.5= 98.5. 101-98.5= 2.5 so that is our cost. We are short at 7400 in June and July, but long the 7550 put in July. The logic of the trade is that we will have a ‘free’ put spread for July, so long as June expiry is above 7400. We have risk at 7400-150(the value of the put spread). This means we have risk of loss at 7250. Max reward is 150 minus our cost 2.5.

We had for the July put spread 49.5 and 80.5,=31 minus 2.5 that we paid and 13.5 for the 7400 put . Thus we have a profit of 15 but we run to expiry.

Nice- we were now in profit to the tune of 29.5- our cost 2.5= 27 (July spread 87.5-49.5), The Jun7400 put 8.5. Run to expiry

WIN! 22.5 – minus our cost 2.5= 20

Trade319 A Comparison

Here’s a quote I picked up this week: ‘Comparison is a thief of joy’ while that might apply in everyday life, it’s interesting in our trading. As regulars know, we DON’T like the butterfly trade but in this market we don’t have any clues though the 7600 level may be a magnet. Or a figment of our imagination.

So, we are creating a butterfly and using 7600 as our centre. Buy the 7500 call, sell 2 x 7600 calls and buy the 7700call. Prices: 144, 70(x2) and 23 gives: 27 For the puts buy the 7700put sell 2×7600 and buy the 7500 put. Gives us 103.5, 50.5×2, 25, gives: 27.5 .We will be interested to see how market action/inaction affects the two.The joys of comparison, but with the same levels will there be a difference? We hit the jackpot at 7600, but a wild card-the 7850 butterfly (7850/7750/7650) is a meagre 13.5 to buy. NB A butterfly has zero risk beyond the premium paid as it is a long spread versus a short spread of equal max value.

Here goes: Calls 85.5, 25.5(x2),5.5 gives us 40. Puts: 140.5,60.5(x2).20.5 gives us ….40

Both gave us at best 50 about 90% profit but there was effectively no difference between puts and calls WIN!

Wildcard 7850 ‘fly : 286, 187.5(x2),96.5 gives us 7.5. And THIS is why we don’t like butterflies much, you have to get your strike levels right. So, as we said the 7600 level seems to be a magnet, but that is not carved in stone. LOSER! (as expected)

Trade 320 Bonkers and Irrational, but It Might Work.

We are selling ITM(in-the money-) strangle(also knows a a GUTS) in the June series.The 7650 put and 7450 call have intrinsic value of 200, the actual value 96.5 and 127.5 =224. We expect the intrinsic value of the sold options to be 200 at expiry.This may also be a trade that works well in reverse. It’s a departure and has some risk if we go outside 7450-7650. A very seasoned broker once told me he didn’t know why anyone would trade a GUTS. We’ll find out!

Expiry at 7650 was fine so we made our 24. I had commented during the week that we could have closed out and not had the PIN risk, but having some ‘skin in the game’ makes us focus. So, the question is, why would you trade a GUTS? I think that when you have big deltas, maybe the attraction is that any moves of the underlying within a fair bracket are not so alarming. In %age terms it’s far gentler. A better choice in a flat market compared to a strangle which can get very skewed. We will try another one when it’s a fit.

Trade 321 in a flat low vol market- Yikes!

Let’s get spicy in this season of low volumes low volatility and low expectation of actually having a smart trade. Theta is not our friend so we look to take on more risk and sell more options than we buy. Here we sell 2x the near month, July strangle 7400 puts,(24) 7825 calls(24), and we buy one August strangle: 7400 puts (55.5) and 7825 calls (44.5) .Here’s the numbers: 55.5+44.5= 100 and 24+24 (x2)= 96. Our cost therefore is 4

Overall theta is around 1.92 and Deltas, we are not far off neutral. Risk – well it’s going to get ugly outside of our strikes. Hand on heart it’s not ideal but we always remind readers it’s about learning, winning is the cherry on the cake.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.