That Was The Short Week

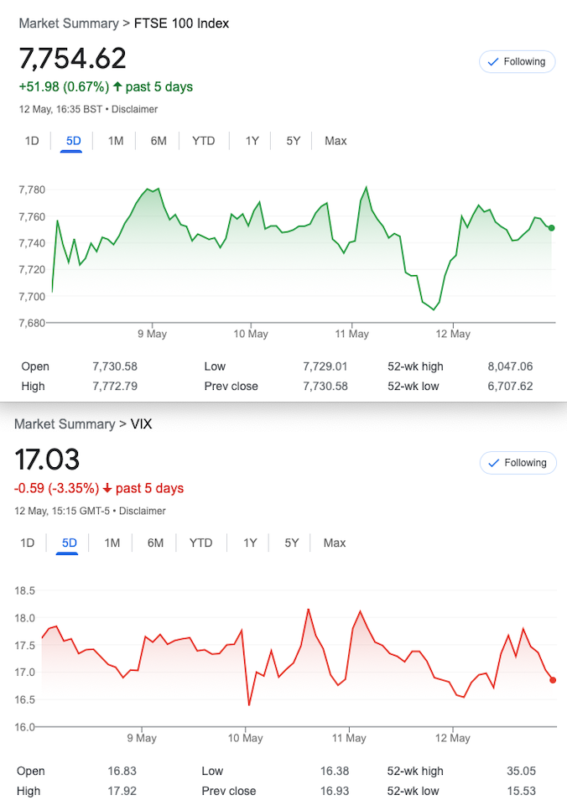

The coronation went well, though it seems the Metropolitan Police’s zeal was misplaced. I’d suggest that perhaps the risk perception was heightened in view of world events. We have concerns in our tiny microcosm of FTSE options, as the debt ceiling in the US looms, inflation stays high, banks raise rates. Our fickle mistress of 100 shares, however, remains unperturbed. Vix remains skulking around in the lower reaches. News will be thin on the ground but remember it’s expiry week, and next Friday may see some fireworks, so it may be prudent to close out. I always recommend thinking about trades that have nearly run their course, and you have to ask the question:”Would I take that risk/reward as a new trade today?”. Risking 100 to get 2 is never a wise idea.

Economists seem divided as the UK’s GDP showed a tiny 0.1% growth(p.a.) though quite how this number is cooked up calculated may be questionable. We don’t have those insights so have to take the ONS at its word. Rishi, our glorious leader remains stoic in the face of drubbing at the polls too.

Some Musings About The Bigger Picture.

FTSE index is our focus here, for its simplicity, liquidity and no prospect of early exercise, being ‘European style’. However options are a poweful tool when used in combination with ownership of the underlying. Whether it’s futures or a stock/share there is such a plethora of possibilities when used in combination. Beginners generally start with the old faithful, the covered call. Managed funds now advertise on TV as it seems the UK is slowly waking from a financial coma. There really are ISA millionaires, they’ve been around since the last century, that’s 24 years. But how about some protection for your ISA or pension portfolio? FTSE100 stocks tend to move loosely in tandem with the index itself and you could do worse than buy protective puts. How would that have worked in 2020? Massively well.

It’s a sobering thought that none of these funds use options to enhance returns and offer downside protection. They really lack the sophistication, preferring to offer only cheap basic services. Personally I’d settle for losing 2% a year for 3 years and copping a 30% return from written calls and long puts. That would be my idea of a properly managed portfolio, if we are forced to buy shares that may/may not perform. I don’t think that fund exists in the UK for us retail clients. Perhaps we should look at doing that.

The Wisdom of Charlie Munger

I think this may have been on Twitter , but as an aid to trading it is valuable, free wisdom.

Yours truly can still recall vividly my first trade, my mistakes, my depths of despair as I could not see the wood for the trees. Losses, profits there is nothing like trading. Nothing. We need to be mentally sound, not just stoic but at ease with our own persona. It’s ok to be a ‘perma bear’ we are profitable alongside the long only crowd who, at least in our minds, lie awake worrying about their portfolio. Trading options however is unparalleled for flexibility, for rolling ugly positions, for trade repair, for being bullish bearish and market neutral. Options give you 3 out of 3 paths to profit. However options demand a longer attention span, and there is a great quote about that from Charlie.

Distraction Trades

ADA $0.364

XRP $0.425 What is going on in crypto land? Is it an idea that has run its course? Twitter is plastered with nonsensical crypto Tweets. Dutch tulip mania?

DAX 2 wins 200, one break even (+30) one loser -30. This is still doing ok, not glamorous, but it ticks along making money. Nothing leapt off the page to inspire us into trading a new instrument.

Legacy Trades 313, 314 ,Spicy 315, 3 wins and 316

313 We Try to Break That Losing Streak( We did Warn Those Trades Might Get Ugly)

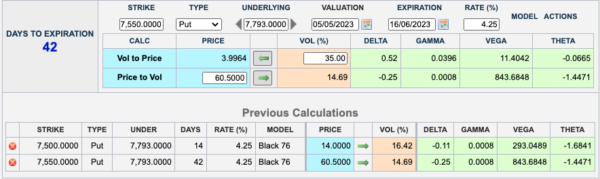

As you’re aware, this is not about bragging rights, it’s about learning.We have extensive runs of wins and statistically we were due a run of losers. It’s a ‘cheap’ market, with no expectation of a big drop. However, we can maybe find a trade that is not a horrible loser! We find a long put spread 7850/7750 and a way to pay for it with a 7600 put. This gave us 70-46= 24 the cost of the spread, and we sell the 7600 put for 27, giving us a credit of 3. Thus, the trade can make a max 100+3, and is safe all the way down to 7500. There is of course, no risk to the upside(makes a change!)

Previous week:

7850 put– 74 7750 put 44. the 7600 put 22.5. Gives us a little profit 30-22.5=7.5+ our 3 credit.Gives us 10.5 so far

Last week

7850 put 107.5, 7750 put 56, the 7600 put 23 gives us 51.5-23=28.5+3 A profit of 31.5 WIN! Close out? In short, yes we would, but let’s run it to expiry

Now 70.5-8.5 =62 Bigger WIN!

Trade 314 -When There’s no Vol

This is one of those times when trade selection is limited by volatility. What we can do with options, is take advantage of time decay(Theta). We can sell options but vol means risk is heightened,and the upside may again be a problem. Unusual but practical, let’s go with a rare foray: naked. We can place a strangle with May options and 21 days to expiry. Frankly I just like the round numbers, so this may not go well! We sell both of these as it seems that they are at strong support and resistance. 8000 call 15.5 and 7500 put 15.5 . Credit 31 means we break even at 8031 and 7469. The market has been kind and we now see the 7500 put for 14 and the 8000 call at 3

Close out! We make a healthy near 50% in a week. 31-17=14 That’s 45% WIN Again we will run it to expiry for educational purposes.

Amazing – this week it is 0 for the call and 5 for the Put, gives us a stonking 26

Trade 315 Calendar Time -Shall We Get Spicy?

So, the principle here is that time decay works faster for options as they near expiry. Thus we can take advantage of this by selling the May options and as protection we buy the June options. We can sell 1 in May, or 2 or 3 against 1 in June.

Here’s what we did: Sold 3x May 7500 puts, bought 1 June 7550 put.

Note: Deltas 11×3 =33 against 25. Theta : 5.05 against 1.4471 =3.6 Gamma 24 against 8, but not too crazy, with vega not so crazy against us either. We have 2 weeks to get our b*tts handed to us.

Welcome return to Profitville, our home. We sold 3 7500 May puts which are no 5×3= 15. We bought the 7500 June put,and it’s now 47.5. Gives us 32.5, a WIN, but we paid 60.5-(14×3)=42. Which gave us a cost 18.5. Therefore, we make 14 . Run to expiry

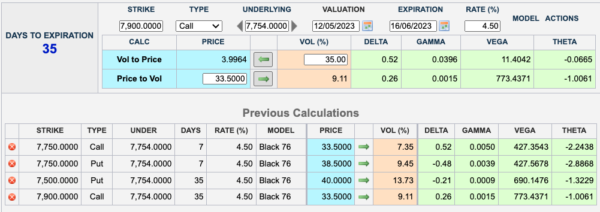

Trade 316, Last Trading Days into Expiry

Firstly I hope it is clear from the graphic that there are 4 options calculations. Secondly, this is untested but we’ll throw it in the mix for fun. We have renewed our winning ways and don’t want to spoil that. However we are here to educate, nothing more. And this is a quirky one. We are buying the May straddle, and selling a June strangle. Why? If we get a half decent move(downside preferred) the near month straddle is far more sensitive to price changes of the FTSE. It is a ‘Hail Mary’ trade as they say in American sports films! In summary we buy the 7500 call and put for May(The straddle). We are selling the 7900 call and 7500 put for June(the strangle). The prices are thus: 33.5+38.5= 72 for the May straddle. We receive 33.5+40=73.5 for the June strangle (7900 call and 7500 put) We therefore have a credit of 1.5.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.