That Was The Week We Really Did Not Wish For!

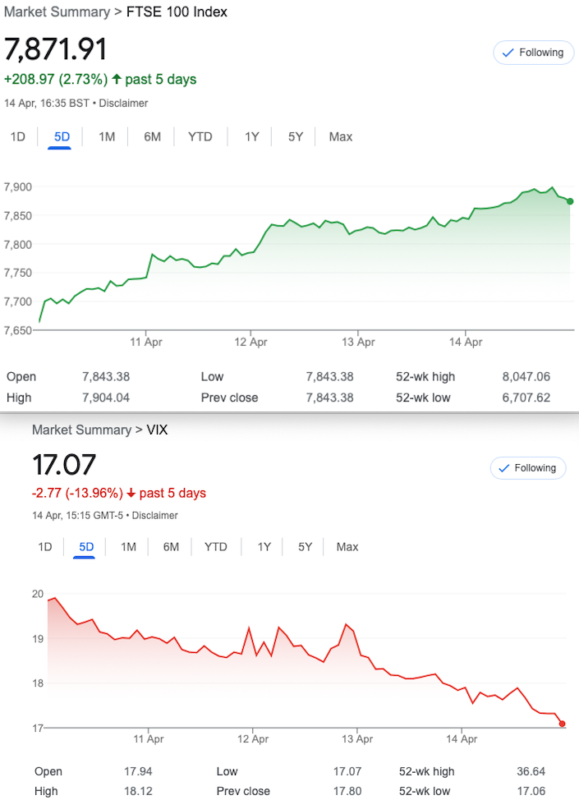

So, 4 days and the FTSE has gone postal! So the MSM really went to town with convincing us it was 2008 all over again. Fool me once, shame on you, fool me repeatedly- shame on me, yet again. Like many traders I tend to have a short bias and again this is ugly. FTSE is up 7.2% in a month, VIX down 34% . It has been a long time since we saw decent volatility and thus it may make sense to step aside until the froth gets blown away (we hope). The joy of options, is that when we are wrong, we can take a hit and take some fresh positions, or we can roll and maybe miss some opportunities.

Frankly, your dauntless trader thinks it’s time to do nothing, when time decay is the only tool in the locker. While my duty is to post a trade every week it has been a tough call(pun intended!) for a few weeks. Although, we are not here for bragging rights, as primarily we aim to educate and enlighten.

History Lesson

A quick back of the cigarette packet calculation shows that in the last 10 years we’ve had 7 up years and, yes, 3 down. Furthermore those up years gave 67.7% up against 29.2% down.(01Jan-01Jan) So the buy and hope strategy, if dividends are reinvested over a decade will do ok, as we all know. But at what point do you buy in? Our metrics tell us S&P500 is very overvalued and earnings may shock.(heard that one before, somewhere!). Curiously FTSE was massively overpriced Nov- March relative to the S&P. Nothing has changed except these relative P/E ratios. I am at a loss to understand this, but fundamentals were never much of a concern, when the options chain can tell us 75% of the picture. Seasonality, a moribund VIX tell us the buying frenzy may have legs yet.

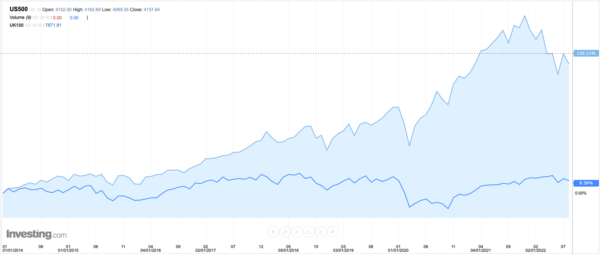

Where would you put your cash? A decade of US vUK indexes and relatively the FTSE just looks a bit rubbish, even taking longer to recover from the dips. Does anyone see the US losing their dominance?

Distraction Trades

ADA $0.4514 Now above the level at which I closed out- will I regret it? Do I have FOMO? No.

XRP $0.5227

DAX 3 no entries, one loser(-30) one break even(+30) Well that’s a week to forget!

Legacy Trades 308 (won and we closed, but we ran it for fun), 309-312

Remember this is NOT our strategy but all power to its creator.

What is it? Oh you’ve forgotten. A trip through the archives will show we’ve used it before.(You do the search!) Here’s my understanding of the trade. You find the value of the ATM (7350) straddle 188.5 (calls)and 203.5(puts)= 392. Subtract that premium from the 7350, and it gives us the strike for our trade, but we always have a bit of wiggle room. So, we go with the 7000 level, which gives us premiums of 438.5(calls) and 3x 105 (puts) We SELL therefore, one call and three puts for a massive premium of 753.5 as you know in real terms this is a shedload of cash: £7535.00.

Imagine FTSE expires on 21st April at 7000. We keep the bloomin’ lot. Now-do the hard yards (it’s not hard) and see where your risk is. It’s simply 4 short options at same strike. Yes, it made 100+ WIN!

As we said this was a quick turn, not a hold to expiry. (877 -a loss of 123.5 )

Trade 309 Sentiment =denial, let’s test that proposition. (I think we might see another plummet!)

We like the idea of….. oh wait. We don’t really like these things, but in view of the fact there’s no market moving news until Thursday, let’s see if FTSE vol will shrink further. And to save a bit of legwork here’s a nice explanation: https://www.optionsplaybook.com/option-strategies/iron-butterfly/

We choose the 7400 ATM strike and buy the wings at 7200(put and 7600(call). Gives us ( 147.5+144.5) – ( 85.5+48.5) = Credit 158. Worst outcome, the FTSE smashes either side of the wings- ie <7200 or >7600. We need a quick round turn. We need vol to drop off.

Worst outcome – it’s here! 299- 126= 173 Losing 15 so we will let this run, but not much hope of a turnaround. ( we never like these and would usually close out quickly, or not take the trade!)

Also looked at this with 7600 put and 7200 call– same misery! 229 cost, current value 216.5

7400 straddle 354 and 10, 7200 call 547 7200 put 5.5 7600 call 168.5, put 26.5 Thus we have 364- (168.5+5.5) =190 a loss of 32 or (547+26.5) – 364( the straddle) gives us 209.5

Now 202 –cheaper to run it to expiry! Horrible trade.

Either way, once it goes outside the wings, it’s a losing proposition.

Trade 310, a Diagonal Twist

A diagonal is a short option in April, the front month and a long option with a higher value strike in May, the next month, and here we favour the puts. Normally we buy the 7600 May put and sell the Apr 7500 put, but it’s rather expensive. In fact we have 130.5-43= 87.5. We have a litle more risk but we sell the 7200 May put for 44.5 bringing our cost down to 43 the max reward will be 400*-43= 357. We risk losing some or all of our premium if the market takes off skywards, and on the downside we have risk at 7500- 400*= 7100 and we surmise there is strong support at 7300. Thus we are delta neutral and theta works nicely for us. [for fun I am tracking an equivalent trade with calls, but its risk/reward is not as good]

*400 is the max value of the 7600/7200 spread, remember.

Ugly Results:

Was: April 7500 put= 15.5 May 7600 put 81.5 and 7200 put= 27 Gives us 39. Tiny loss 4 so far.

7700 apr call 91 7850May call 60.5 May7650 call 171.5 gives us 20 and cost 30

Now: Apr 7500 put=3.5 May 7600 put 39.5, 7200 put 15.5 now 24-3.5=20.5 still losing

Calls: 7700 apr call 182.8 May 7850 call 110 May 7650 257.5 Even uglier cost 30 and now minus 35 plus 30 debit

Trade 311 Spring Fever or A False Dawn? Time for A fun Vol trade……..This might hurt.

We note the following prices: 7600 May put 81.5 7600 April put 26.5 Anyone spot a crazy fun trade? Let’s sell the May put and buy 3 April puts with the premium (3×26.5=79.5 ) Gives us a credit of 2. Does this make any sense? The esteemed Price Headley has made the case for reverse calendar spreads when vol is very low and it is not unreasonable to expect it to have an up move. We’re going all in with a 3 x 1.

Now we have May 7600 put 39.5, April 7600 put 4.5×3= 13.5.26-2 credit LOSER ( Please note erratum- I had declared this a WIN before editing)

Trade 312 A Jelly Roll , That’s Right, A Jelly Roll

This trade comprises short call in the near month(Apr) and long put at the same strike. This is then reversed in the far month(May) Thus we have:

The strike is 7850 April- call 52.5 put=26 May call 110.5 put 98.5. We sell the Apr call and May put= 151, and buy the Apr put and May call 136.5. Gives us a credit 14.5. after expiry we may or may not be in profit but we are left with a long synthetic- the short put combined with long call give us a theoretical proxy for the underlying FTSE future. This is an old strategy that I have not ever tested, as it seems self defeating, though one or both April options could expire worthless. We will have to wait until Friday when I hope expiry will be 7750 for purely selfish reasons.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’ like help with, we all started somewhere and yes, it can be baffling.

Apologies for the late edit.Trade 211 was a back spread.