That Was The Week The Hammer Of The Stocks Struck A Blow

I hope, firstly that our readers have not been clobbered by this massive blow to the market. Should you be nursing losses please USE this time to step back and divorce yourself from your positions, and look at them again, pragmatically. Ask yourself those tough questions: Were my reasons for the trade valid at entry(tick that box).Were my reasons for staying in the trade STILL valid? (tick box). Did the reasons, ie the facts, change and you did nothing? (do not tick that box). As options traders we can alway limit losses when we trade sensibly. We look at the risk and consider how we would deal with a 5% move against us. We do not marry our trades, we do not revenge trade. No shame in having losing trades. They are a learning opportunity.

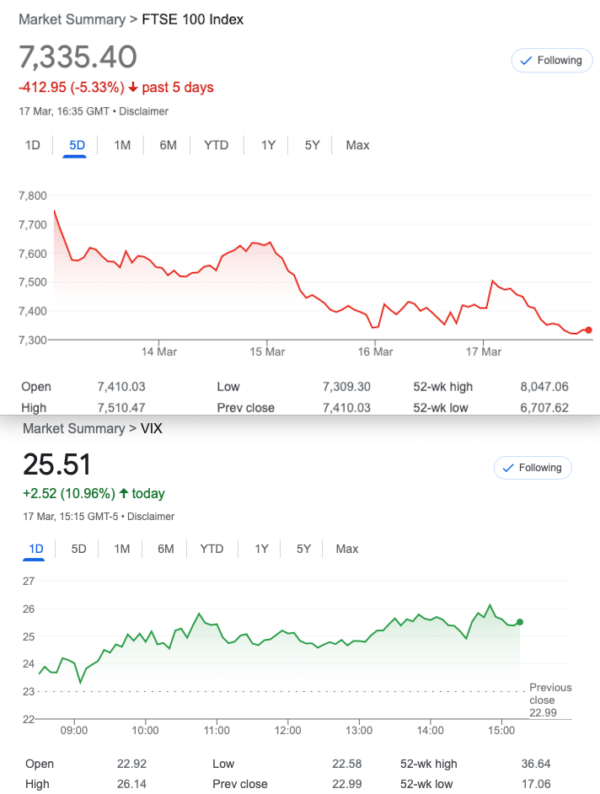

I hope the expiry chart is clear- 5 minute candlestick showing how it was held up, before the ‘dump‘. However this raised my eyebrows to the heavens:

From one of my multitudinous emails: Fuller Money.Monday 13th March (David Fuller, the highly rated founder) is no longer with us.

1. OpEx – March (3/17) Option Expiry: $2.8 Trillion Notional to un-clench GAMMA (also quarter-end gamma). This is a big number. This removes the 4k pinner, that has kept a lid on big moves. Either way. We are going to move next week.2. Peak open corporate repurchase window. The corporate buyback blackout window begins on 3/16, where 40% of US corporates will be in the blackout window. This window ends of 4/28. Reminder corporate authorizations have been an all-time high YTD. There will be a decline in vwap purchases during the closed window. We expect executions to drop by ~30% during the closed window.

My 4 Penn’orth

Personal Note:

Your intrepid real money actual bona fide FTSE options trader had a ‘senior moment’ but also a flight to safety. Tuesday I realised I had a heavy cold coming on, and while my positions were designed to run to expiry, I closed out. I have traded when unwell before and it did NOT go well. Your less than intrepid trader had also failed in my duty of care to close out some short put exposure that could have been neatly closed for a tidy profit. Underlying this was a deep ITM call strategy that was a huge hedge against short puts, and utlimately did extremely well. I will not reveal the trades but suffice to say, the profit range on FTSE was 7200- 7800. A miserable fail and I missed enough profits to take the year off! I avoided the crazy moves and resultant stress for a few hundred quid.

Lessons learned? Have more faith in the calculations. ( I knew precisely where my range of risk was). When you should do nothing, because you have in place checks and balances, DO NOTHING!

Distraction Trades :BOOM!!!!

ADA $0.3533

XRP $0.3821 BTC…….. UP 34% this week so our sad little players are doing zip, but would you want to own BTC?

DAX 3 wins: 600, 500 ,100. 2 No entries YES!!! Our miserable one trick pony strategy brings home the plant based bacon facsimile.

Trade 308 Opens as 306 and 307 close

We are again in the sweet spot of theta, the edge that makes this idiot look moderately impressive! We therefore need to sell more options than we buy. Let’s get spicy with a short iron condor. We BUY the body and sell the wings. Here, our body is the 7900 straddle, the wings: the 8000 call and 7750 put. BUT we do a ratio, by selling twice as many wings. This means we pay 82 and 110 for the body, and we receive (x2) 38 and 59.5 for the wings= 195. This gives us a tiny credit of 3. Risk is at 7600 and 8100

Those prices now: 95 and 40×2 for the calls 50 and 20×2 for the puts Giving us a credit of 15+10= 25

We ran this again but noted we have a healthy profit

Despite the massive drop this is still in profit as the 7900 straddle is 189.5, the 8000 call 3 the 7750 put 78.5. Gives us 189.5-(3+78.5)x2 =26.5

Of course by 17th March it would have been a catastrophe if we’d held on.

306 Straddle Dilemma

So it’s almost exactly half price to buy the near month(March expiry) straddle(put and call at same strike) compared to April. Should we be headed for serious moves and an uplift in volatility, we’d be buying 2 of the March and selling 1 April straddle. I see too much theta for one thing. I also don’t expect a mighty downside move which we’d need. We need to be on the right side of this so we will cautiously sell 2 March straddles, and buy 1 April.

Murphy’s law of options states: When using theta as the sole reason for the trade, it may come back to bite ones rear end!

LOL!!!!! 305 for the April straddle and 230×2 for the March.155 loss if we’d taken the perverse route reliant solely on theta. See the above statement- if selling it on Friday it came back to bite yer bum big! However, we talked about the massive time decay and if closing out on Wednesday (when yours truly got a ‘GUT’ feeling about the impending drop) You’d have made 237-211=26

Done the normal way we’d have monster profits I have highlighted my original views. Expiry ( nobody is going to tell us) so I guesstimate – 7470, this would give us a monster 7950 straddle x2 of 480 March and 1x 7950 straddle Apr= 7+620.5= 627.5. So, 960-627.5=332.5

The lesson here is plain: Do NOT try to meddle with this, it only works the way it was intended, by giving you a free extra straddle. I have traded these in the past and never managed to time them so profits/losses were about break even. But, I’m no market timer.

307 Big Vol Short Time as Expiry Looms.

A relatively safe play. A one for one calendar spread as near month vol is not too rubbish for once. Reasons for the trade? Vol does not tend to linger -see the hourly chart

April : 7900 put 227 and March 7900 put 179.5 our cost: 47.5

Monster win! 7900 Mar put (7900-7470) = 430 Apr put 574, gives us 144 profit,minus our original stake 47.5=92.5

We make ±200% and should consider: Is this a rinse and repeat trade? Some backtesting required. Some further trade rules too. WIN!

Trade 308 High Volatility- But IS IT?

Let’s dance with the Devil. It’s PITCHFORK time. Remember this is NOT our strategy but all power to its creator.

What is it? Oh you’ve forgotten. A trip through the archives will show we’ve used it before.(You do the search!) Here’s my understanding of the trade. You find the value of the ATM (7350) straddle 188.5 (calls)and 203.5(puts)= 392. Subtract that premium from the 7350, and it gives us the strike for our trade, but we always have a bit of wiggle room. So, we go with the 7000 level, which gives us premiums of 438.5(calls) and 3x 105 (puts) We SELL therefore, one call and three puts for a massive premium of 753.5 as you know in real terms this is a shedload of cash: £7535.00. Imagine FTSE expires on 21st April at 7000. We keep the bloomin’ lot. Now-do the hard yards (it’s not hard) and see where your risk is. Here’s a blokewith a pitchfork- get it? 4 prongs, 4 options at same strike

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com

The utter temerity of the banksters -now ramping up the markets like it’s free money time again.

Trade 308- one option was to close out and take quick 34-38 points.