Fallible and Distracted, Yes. Harmful? Probably Not!

Before getting into it, an apology for the errors in the last 2 trades. I had decided that March 24th was expiry. It is NOT! I have been somewhat distracted and there is genuinely no attempt to mislead anyone. Our remit here is : Warts and all trading. No BS and when opening the trade it is not in retrospect. However we did suggest adjustments for trade 304 with such massive premium from the short put. I hope we can update in real time any further adjustments.

So, here we are again, that grind upwards, and while it has suited our trades here yours truly finds it quite annoying. I confess I am short FTSE via some call strategies. This started in December and so I have rolled over and reduced exposure from that trade. However I had a very long term(6 months) strategy which while underwater can be rolled to a slightly better range for no cost. What this does is 1. Freezes my call exposure 2. Gives me a massive hedge for short put trades. Thus I am taking in profits as those put strategies have made serious coin. 3. I am comfortable in positioning AND size.

However while we can roll options trades ad infinitum, there is an opportunity cost.

That Was The Week -Stuck Record? No Good News is Good News

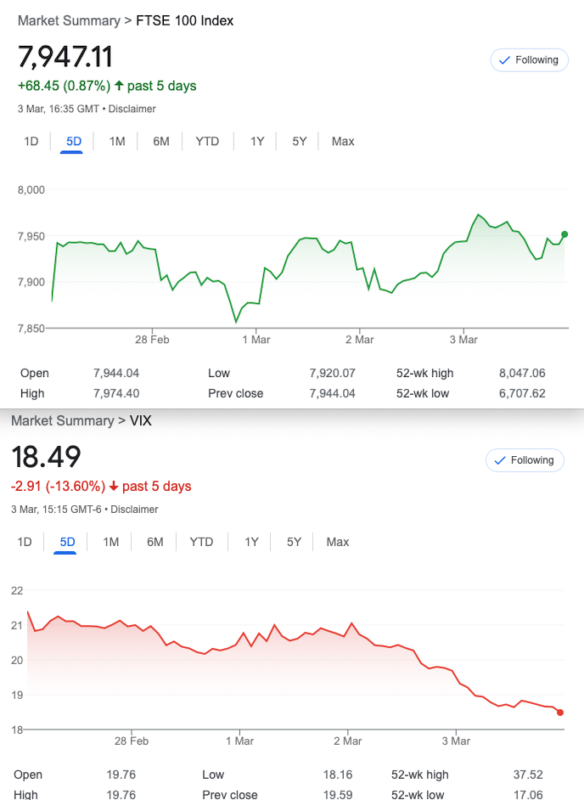

The charts say it all. Bit of a bounce, options vol dropping and people are back to buying the dip. However they are also selling the rip, as they say. 7900 is the key level and it will be good to see interest rates brought up to sensible levels. House prices are dropping but this is after a rise of some 20%+ in the last few years. One grave concern is the madness of 0DTE options issued by CBOE. Allegedly 45% of options trades are with these horrible things. Distortions ahead, anyone?

Meanwhile this popped into my head this week- a fresh look at CBOE’s data offerings, and the one index called gamma got my pulse racing, however it’s not what you think, but it’s interesting,see here: https://www.cboe.com/us/indices/dashboard/VIX/

and here for the explanation of the Gamma index: https://cdn.cboe.com/resources/indices/documents/GAMMA_Methodology.pdf

So, this plethora of indexes may be priceless to some, but it is indicative of the great data we can collate. Oh wait, it’s American. It thus remains in the world of acadaemia for us, but it’s thought provoking. We should never stop learning.

Distraction Trades

ADA $0.3421

XRP $0.3755 ( Changing places with ADA again but still in the doldrums)

DAX After last week’s bangers, 4 no entries one win 60 The entry method missed about 400 this week, but quite how entries might have been taken on the 5 minute chart is impossible to know, although lunchtime entries look promising.

Legacy Trades and 306

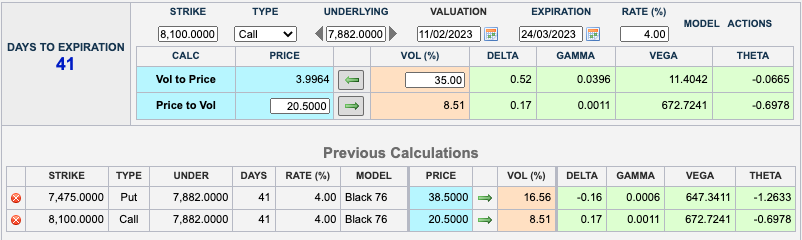

303 A Whole New Expiry, An Old Strategy

The regulars will spot this right away, and it’s maybe a cheap shot. Yes, it’s a strangle. We are selling Σ1 put and call. Tasty Traders will know this as a 1 standard deviation 16 delta strangle. Risk is unlimited on both sides, sort of. But the risk is at 8159 and 7416. We run these to 50% profit and if it still looks ok we run to expiry. Theta is ok but while vol is ok for the put that makes the call a very low vol item.

Those prices now: 37 for the call and 19 for the 7475 put.

Last week: the 8100 call now 14.5 and the 7475 put now 23 =37.5 our 59 credit now reduced by 36%

Now: 12 for the call and 7 for the put= 19 to close. We took in 59, remember. WIN!

[please note as stated, I put in the wrong expiry date, so the Greeks are a little off but the trade remains the same]

Trade 304 Starting with a Debit of 160

We are told there’s no downside hourly daily or monthly. Let’s put that to the test. We will sell for 173 the March 8100 put. As a little insurance we will also, have a call ratio spread 7800/7950 for cost of 215- 107.5×2 = 0

This is breaking some new ground and we will be in a bit of a pickle if the FTSE takes off upside again, but we have taken in the big premium from the 8100 put. This may need some adjustment but if we don’t break stuff, to quote Mr Musk, we’re not trying hard enough.

Last week we saw this:

Where are we now?

Where are we now?

So, no change- they say it’s a buy on a monthly basis,on a TA basis.

Last Week: 8100 put was 242 ouch! However some mitigation from our call ratio spread which was 144.5- (57.5×2)= 29.5 in credit.

This Week 166.5 for the put, and that call ratio 171.5 and 64.5×2 =42.5 Credit – Overall position thus 124

Adjustments? Monday we buy back the put for 196.5. Tuesday we sell it for 246.5 reducing our deficit by 50 (Easy in retrospect, but I will try to update in real time) However our liability drops to 74

Trade 305 30 days to Expiry When Theta is our Ally [not 30 days, but 23 as mentioned]

We are again in the sweet spot of theta, the edge that makes this idiot look moderately impressive! We therefore need to sell more options than we buy. Let’s get spicy with a short iron condor. We BUY the body and sell the wings. Here, our body is the 7900 straddle, the wings: the 8000 call and 7750 put. BUT we do a ratio, by selling twice as many wings. This means we pay 82 and 110 for the body, and we receive(x2) 38 and 59.5 for the wings= 195. This gives us a tiny credit of 3. Risk is at 7600 and 8100

Those prices now: 95 and 40×2 for the calls 50 and 20×2 for the puts Giving us a credit of 15+10= 25

We run this again but note we have a healthy profit

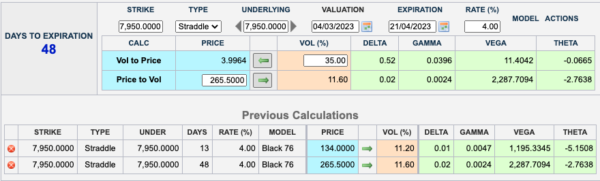

306 Straddle Dilemma

So it’s almost exactly half price to buy the near month(March expiry) straddle(put and call at same strike) compared to April. Should we be headed for serious moves and an uplift in volatility, we’d be buying 2 of the March and selling 1 April straddle. I see too much theta for one thing. I also don’t expect a mighty downside move which we’d need. We need to be on the right side of this so we will cautiously sell 2 March straddles, and buy 1 April.

Murphy’s law of options states: When using theta as the sole reason for the trade, it may come back to bite ones rear end!

Aaaaaah Dammit. Last night I was reviewing the day’s action and thought it was time to close out, but at the screen late! – the 8100 put was 178 and the call ratio was 65, cost 113 and a clean slate for a drop.

even closing last night …..221.5 and 65 for the call ratio.