That Was Expiry Week

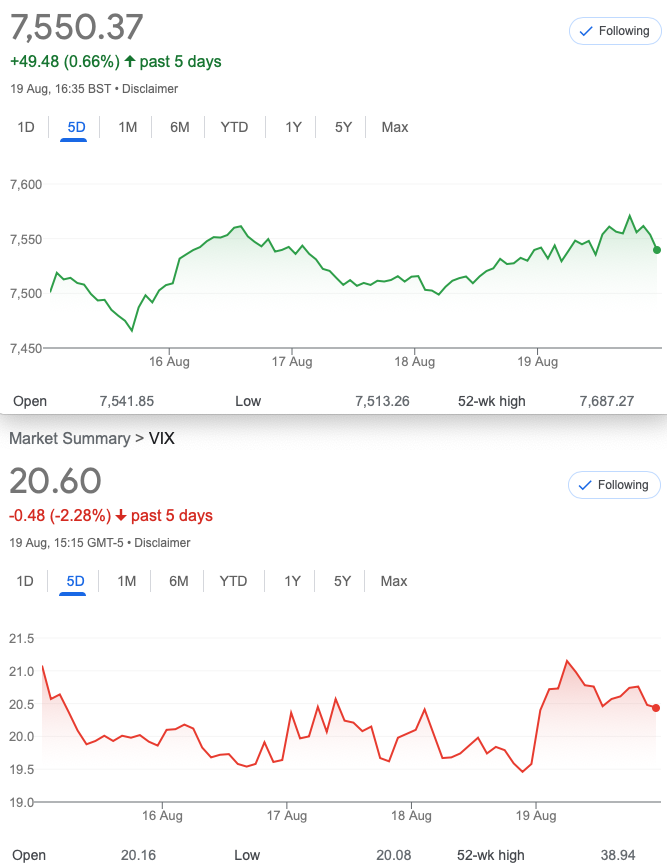

Expiry at the week’s high, more or less. What’s going on? This week’s moves by constituents: https://uk.investing.com/indices/investing.com-uk-100-components

Hard to know why the FTSE is up -seemingly Glaxo and BP– 2 of the behemoths have seen big ups, but to these weary eyes, there is a sea of red. However we are not really concerned with the quirky machinations, but with the final price. Nothing to report this week- impending recession, climate emergency saw Las Vegas, New Zealand and China among others dealing with floods. Meanwhile forest fires are rampant in Europe and the Rhine has his a new low depth of 30cms. The UK and much of America is in a drought and most areas here have a hosepipe ban. Nothing to see here. So let’s dig in and reflect on the trading wins and losses.

We like to show a diverse range of trades and the losses- an iron condor and the bonkers 3×2 trade are not our optimum choice as they didn’t fit our risk profile, or our assessment of the ideal market conditions. However it’s important we don’t paint a rosy picture, like the call buyers who seem to make $300,000 a week if we believe the claims. Jealous much? I couldn’t pick a winning stock to save my life’s my ‘fun’ portfolio shows. No, you can’t know what’s in it!

Late Publishing

Apologies for being late this week, travels to far flung points in the UK on family visits kept me away for a few (refreshing) days. Expiry kept me moderately interested but it was a surprise that FTSE Pinned to 7550. However the summation of my trading had butterflies expiring thankfully worthless, having taken the profits. Sometimes there can be a bonus when these do have a favourable expiry but it’s never a good idea to have a lot of short options at expiry. The one time you have a lot of short naked puts is when the market will bite you. We roll any liabilities into the next month.

Distraction Trades

ADA $0.4611 Ugly-further crypto drops.

XRP $0.34467

DAX- 2 losers(30 each) 2 no entries and one win +90. A modicum of effort for a tiny profit

Legacy Trades Trade 275, 2 wins closed 279 and 280

For those with a limited account the iron condor having no naked element. This keeps margin limited to the width of strikes employed. Here it’s 50 and- a reminder of what the iron condor is. We sell a call spread and a put spread, our view is that the market will stay in a limited range 6875-7425

We sell the call spread, thus: sell Aug 7400 call for 49, we buy the protective Aug 7450 call for 36. Gives us 13

We sell the Aug 6900 put for 99.5 and buy the protective Aug 6850 put for 88 Gives us 11.5

We thus take in 24.5 and our risk is……. the 50 spread minus our credit= 25.5

LOSER!!

Trade 278 Bonkers 3×2 Calendar Straddles

That’s a combination of words you don’t see every day! It’s fun it looks nuts but there is a rationale: We just need a big move one day this coming week. We have not seen a sensible 1% drop in ages, Vix has been quiet for a while….

We are buying 3 August straddles and selling 2 September straddles. The long and the short? Theta is mighty ugly, so we need a quick turnaround. The Aug straddle is 53 and 105= 158, we buy 3 =474. The Sep straddle 124 and 180=304 we sell 2 = 608. Now we take in 134 but that is not important. Theta = 6.5×3 against 3.7×2. It is horrible so…..

NOW I remember why we don’t do this!

It needs that massive move, preferably to the downside, so how grim is it? Well the numbers are truly horrific: 95.5×3 =286.5 and 147,113=260×2=520 LOSER! Sometimes we need to show the ugly side and we did say it’s not anything we’d do, for so many reasons. It is trying to be predictive, and primarily we avoid doing that .

7450 Sept 172 and 85 x2= 520 Our Aug 7450 straddle, the calls were worth 100×3. We took in 134. 520-434= Loss 84

Trade278b

Just for fun let’s do 3×3 at great expense 304×3= 912 158×3=474. Our cost 438-ouch! It’s not anything we’d do but let’s see what transpires.***

Trade 278b

*** a massive calendar straddle for which we paid 438,and our outcome? 260×3- 100×3= 480 WIN! A caveat here- this may have done better than this en route but I failed to monitor it daily-apologies. Calendar straddles can be hugely viable when there is excess volatility in the near month, and pretty safe- you are unlikely to lose much, but this was for fun. We’ll try another when the vol IS skewed in our favour.

279 Can we find a credible calendar trade? Yes we can!

Well typically we’d look to sell near month and buy the following month- what’s there?

Well…Sept 7600 68 Aug 7550 14.5 Yes! CALLS And this may well be a disaster -we will sell 2x the Aug calls 14.5×2=29 and buy 1 Sept call for 68. We pay therefore 39 for this ugly looking creature. Logic of the trade? 2 things- theta and the possibility of adjustment in the Sept series if it goes against us. We may need to make that adjustment midweek- we’ll aim to keep up.

For clarity the strikes are 7600 in Sept and 7550 in Aug series.

7600 is 82, the FTSE expired at 7550. Our short calls therefore expired worthless. We paid 39 so we make over 100% in old money! WIN!

Trade 280 and another piece of plagiarism

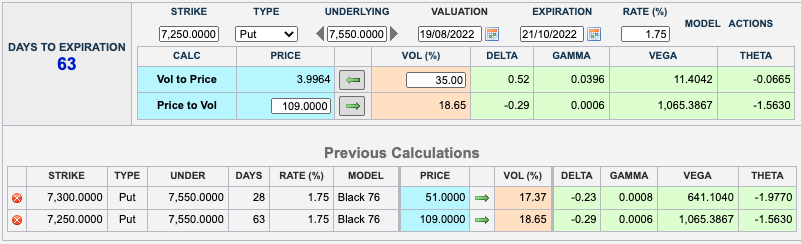

Following on from another of the Manifold American options sites- the best ever options strategy this is a DEBIT diagonal. We are selling the near month 7300 put and buying the far(Oct) month 7250 put. So, if they were both in the same month, we’d had a simple long put spread. What could go wrong? We are paying up for this 50-wide spread 109 minus 51= 58. Time decay(Theta) works for us, and as you will see it is Vega sensitive but Deltas don’t make sense due to the timeframes. We monitor this as it needs to run, but it might be rubbish if the FTSE carries on like the ‘drunken sailor’ it has been of late. Here’s the skinny( haven’t heard that for decades)

It’s a slow burner with 28 days max. And yes, we could lose all our stake but it’s unlikely.