That Was The Week- Biiiig Drop At The Last

So somehow it’s still shocking when the expected arrives. With so many headwinds the markets were bound to take a drop. How we get to the next low is a matter of concern. Gently deflating assets would be preferable, but can that be managed? Sterling has taken a battering this year and of course oil is priced in USD, giving us more pain at the pump. Markets have been pumped with QE and silly low interest rates and this jumped out at me in an article I was reading:

a tip to Luke Gromen at FFTT for coining the term “Central Bank Zugzwang”.

Zugzwang is a chess term referring to a position where a player has to move, but every possible move puts them in a worse position than they are at present.

Here’s a link: https://youtu.be/Njyw9OFbyrE

So, is that where we are? Which ever way the banks go, there’s simply more pain? Common sense does not prevail in the lofty world of global finance, but then we don’t have to make it up as we go along. We can only hope some smarter minds prevail and we are let down gently. Developing countries are really going to feel the pain. Grain exports to these nations are going to take a huge hit. We need to take responsibility globally, but the omens are not good historically.

Know People Who Don’t Know About Options?

From what I can find, daily average of stock trades on US market= $185,610,102,011 Small beer compared to our world!

Distraction Trades

ADA Cardano $0.5566

XRPUSD $0.3582

DAX 3 no entries , 2 wins 70+ and 100+ It’s not horrible but is anyone actually got a seriously great P/L in directional DAX trading?

Legacy Trades -3 of them and 270

267 We Went Assymetric

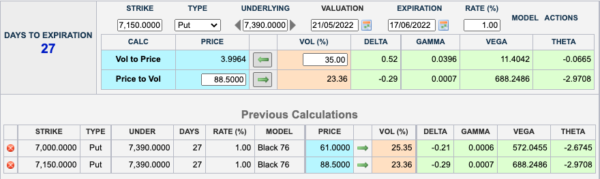

So here we see the CME futures options calculator. However for our purposes, the future is not far from the cash. So instead of doing a simple put ratio buying one selling 2, (OK sometimes we sell 3!) We buy 2(two) and sell 3(three).

Hopefully you will see the prices make this a tiny credit trade 88.5×2 -61×3= 6. Our real point of interest is how the Greeks stack up,and this could do very well if the market carries on down. Bear in mind that to date the S&P500 is down 18.66% Nasdaq down 28.28% FTSE is flat, but since when were we immune from the US? Hence this trade to capture a gentle down market in the next few weeks. Zero upside risk, downside 6900 …. But with many possible adjustments

Prices now 24 and 15.5 so.. 48 and 46.5 We can afford to sit on this it’s a freebie-tiny credit, so it’s only costing us a modest amount of margin.

This week: 23×2 and 14.5×3 -so 46 against 43.5 Nothing to see here!

Now….. 7150 = 58 x2=116 7000 =34×3=102 We could close out for tiny credit 14, but let’s see what more we can get. Fear and greed combining!

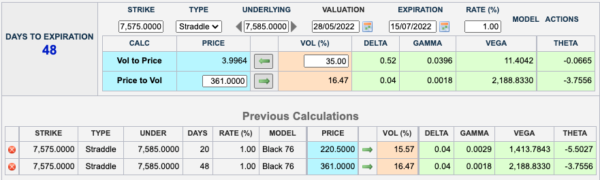

268 About 3 weeks to Expiry, Assymetric

Much to mull over and so many potential trades, let’s go with an old but quirky friend- the ‘bonkers’ calendar straddle 2×3. I have had fun trying to place this with my broker, but when it works……. so what is it? We buy 3 near month straddles and sell 2 next month straddles. Logic of the trade, we have an extra straddle with greater gamma and delta primed for a big move. NB I have used the CME calculator in ‘straddle’ mode, rather than inputting individual legs.

What could go wrong? Time decay and inertia are our enemies. This is not a well researched strategy as the entry rules are a bit of a secret, but hey, we don’t learn unless we break stuff, right? Oh and by selling 2 and buying 3 we still get a credit 60.5 (361×2=722, 220.5 =661.5 )

You all know a straddle is: same strikes,put and call ATM or as near as.

Last week: our short July straddles 334.5 x2 = 669, and our Jun long straddles 191.5×3= 574.5. So 95.5 to close, so currently losing

NOW! 852-784= 68 PLUS our credit 60.5 = 128.5 WIN!

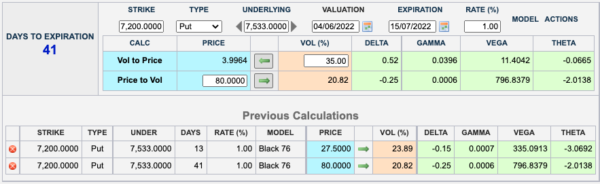

269 Making sense of a short week the Number 3 crops up again, we have a theme!

So due to the Jubilee we have to use Wednesday’s prices and again we are going for the racy calendar ratio –sell 3 x near month puts buy one next month put. We choose the 7200 strike

Yikes! We are in the doodie! We own the July 7200 put now 146, we sold 3x 7200 Jun puts now 69.5×3=208.5

Remember we are not really in trouble, as volatility smashed up. but we only have 4.2 trading days. We will run this to expiry and look to adjust if we incur losses.

Possible adjustments – we sell 2xJuly 7000 puts and buy 1 x July 6850 put -giving us a wide butterfly and a ‘war chest’ of 120 to finance ‘rolling down’ the short puts.

270 -Can We Squeeze The Last Bit of Juice?

Two words : Ratio diagonal. Two other words: strangle, calendar.

We are selling 2xJun options and buying 1x July options

2×6800 jun puts, 2x 7550 jun calls 15.5 and 17 respectively. Multiply by 2 gives us 65

We are buying 1xJuly options

6700 put 53.5 and 7600 call 56.5 gives us a cost of 110. Our credit for selling those Jun options is 65, so the whole thing costs us 45.

We want FTSE above 6800 and below 7550. That is all.