Return Of The Vol

That Was The Week

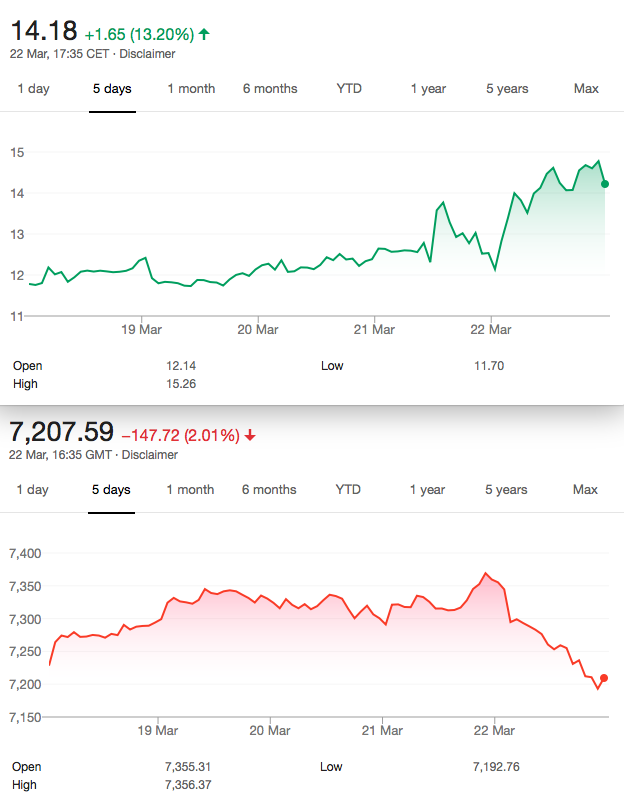

Curiously while everyone is running around proclaiming Friday’s move is a game changer, FTSE is actually up 22 points on the week. Investors cannot stand a down day- just look at the track record of up days this year. I did say last week it makes no sense when everything goes up. However one down day does not a bear market make. We note futures were barely unchanged at close of play, perhaps 10 ticks off.

So what can we expect now we have more MAYhem(see what I did there)? Lawmakers and politicians seem at a loss to find a way through. Many many traders are sidelined, perhaps unwisely. We now have an April or May deadline or is it June. I understand there’s another ‘meaningful’ vote this week. We could see a new prime minister.

For us the big deal is that Sterling can flip one way or t’other moving FTSE a few % either way. But inversely. We can either be positioned for this, or wait for it to happen. I am personally in camp B. Meanwhile,some musings from Saxo Bank-

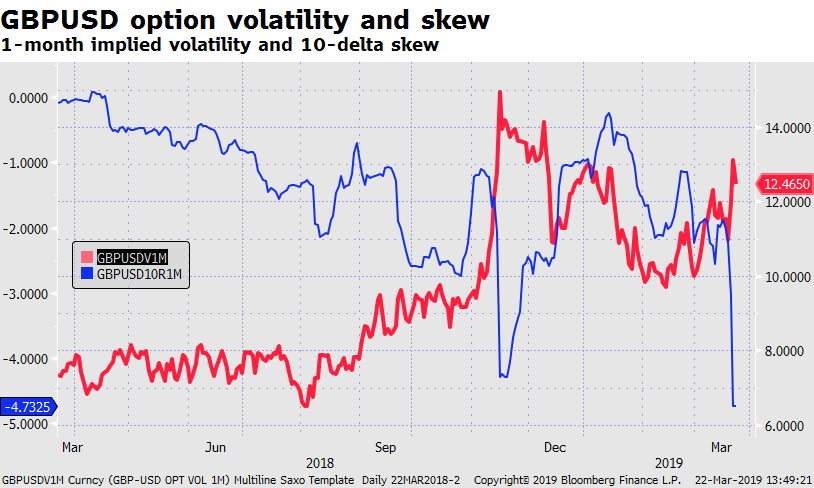

Insights from Derivatives of Derivatives

Excellent link and commentary from Saxo Bank

Including this:

What does it mean? Well on one level not a lot, as it seems obvious. When volatility rises puts get more expensive. I have never seen such use of options data on cable before. However, institutional players are often late to the party with their options buying, I just learned. I’m not sure how many of them actually have an idea-options are the dark arts to so many traders. (Our salvation is that options are complicated. All trading should be. How often do we see new shiny platforms offering instant access to forex, CFDs etc? The footer on the email always proclaims at least 78% of traders lose money.)

I don’t think this helps much for us FTSE traders-and then we have this:

We hope that you all understand P/E ratios. It would suggest the FTSE is expensive-but then it was cheap in December. Oh my! All a bit mystifying. Buyers of funds should always be aware that returns are diminished, in direct proprotion to increased p/e. Which brings us to:

Trade 124 A couple of Considerations

Trade 123…… a bit of a let down. Currently the 6950 Apr puts are 44, the 7000 May put is 96.5. I would opine that a trade gone wrong is a trade to add to. Many many times I have placed a trade and then seen to go ‘against me’. 95% of the time it pays to double up. Logic here is that the front month puts are far too expensive relative to the far month.

Trade 124

Wide winged butterfly Apr puts 7200(long) 7000(shortx2) 6800(long) strikes. Thus we have 116.5 plus 24.5, minus 2×7000 @53.5= 24.0. Thus we have a potential max profit of 200-24= 176. Risk limited to the premium paid= 24.

Logic of the trade?We are profitable between 7175 and 6825. We cannot lose more than we paid.HUMBLE APOLOGIES THIS SHOULD READ A DEBIT OF 34 AND THEREFORE PROFIT BETWEEN 7165 AND 6835. MAX PROFIT THEREFORE 166.

This week’s takeaway- in normal times the data can be unhelpful, and we are very far from normal times.

Harsh!

MASSIVE APOLOGY TRADE 124 IS A DEBIT OF 34 NOT 24 – OPTIONS TRADERS ARE SMARTER -RIGHT?

I WILL STAND IN THE CORNER FOR ONE HOUR