That Was The Week – Regular Options Expiry(Triple Witching Notwithstanding)

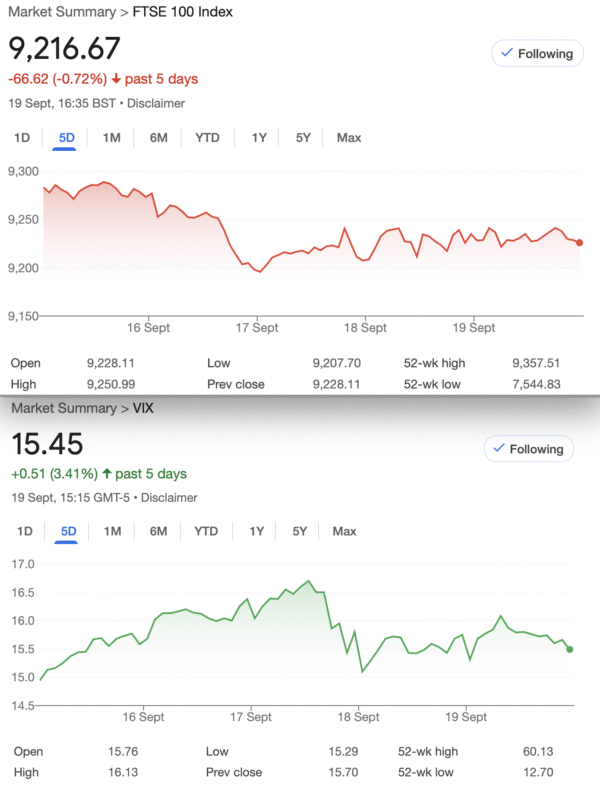

9210.85 That was expiry level in a curious week of concerns over a state visit. Congratulations to our security services for protecting all and sundry. There were some protests and notable pictures of a certain Mr Epstein and a friend, but no violence. So, markets in the US continue to see new all time highs, while FTSE has eased off a bit. However, even if this signals a lack of enthusiasm for our dreary little corner of the world a tiny 0.72% drop is nothing, and we keep getting these small range days. VIX is not really telling us anything and in the 6 month chart VIX has been under 20 since end July and the bands are tightening. You probably know that volatility can plod along in an unrealistic narrow range for a while. this may reflect the amount of also trading in big volumes trading small moves.

Interest rate decisions barely made a bump, job numbers have barely affected interest rates, etc. The character of the market is so hard to gauge but then if memory serves, we’ve had these epic periods of upward markets with barely a blip. Volatility is a problem when it is in short supply. See CBOE’s explanation https://www.cboe.com/tradable_products/vix/

How did those September trades do? Well, there were 5 winners Our runner was rolled again for a credit, with the aim of turning an ugly trade into a trickle of income. Like a stopped clock it will come right at some point too!

In the Inbox

So occasionally John Mauldin and his colleagues send interesting stuff that is left of centre. However we cannot ignore the march of technology. If you like a punt on the future this is a short read:

https://www.mauldineconomics.com/global-macro-update/quantum-the-next-big-thing-explodes#share

Meanwhile back to the present and this runs counter to my own thinking. Probably because I’m a terrible judge of markets and economies. That’s why options suit me, as I’m generally wrong!

Distraction Trades

ADA was $0.9488 now $0.8902 ( a high of $1 recently)

XRP was $3.1670 now $2.9795 A little drop for our chosen Cryptos.

DAX : 3 no entry days, 2 break evens, 1 win 120 nett (this is eerily similar to last week so also investigating when the entry method breaks, trading the opposite direction)

UK Gilts Were £15.83 now £15.73 This is based on the Vanguard ETF, more wobbling around. This has traded as high as £27 still not looking interesting, it seems.

Legacy Trades -Mixed/Losses plus new trade 432

Trade 424 High Risk Big Reward

We will roll Trade 415/415b but also instigate a new trade which is long August 8450call short 2 x 8650 call. Those prices: 531 and 342, so as a new trade there’s a CREDIT of 684-531= 153. As a legacy trade there is a small credit 34.5. This as you can see, is deep in the money with risk at 8850 This may be a struggle but what if we can roll, for a credit ad infinitum?

Was 8450 call 652 8650 calls 456.5 x2 Gives us: 913-653= minus 260 We are running this, remember but it’s not pretty right now!

Was August 8450 call 600 8650 call 405.5 =minus 211. Still underwater with both trades but remember we are rolling, as and when it’s optimal.

Roll to September: paid to close Aug position for 300, opened same position in Sept for 370. CREDIT 70. As legacy trade it’s now a credit of 104.5, as new trade it’s a credit 223.

Last week 8450 call 846, 8650 call 647 x2, gives us 448 we will be rolling this, remember

However, we are running this and against the current market frenzy it will get ugly, but let’s see if this can come right. We can run, AND we can hide!

ROLL: SEPTEMBER TO OCTOBER Cost to close Sept:387, Credit to open 418. Nett Credit: 31

As new trade we owe 418, and took in 223, and now plus 31 =254 as legacy, we took in 104.5 +31 =135.5

We continue this and it breaks the cardinal rules of cutting losses, options can be forgiving. Margin is of course a consideration.

Trade 428, A Dog’s Breakfast of puts

Well as there is no downside risk whatsoever, we’ll take a bucket load of puts and sell them. We’ll buy a few too.

A quirky put ladder starts with a long 9200 put, 115, short 8950 puts x3, 41=123, long 8850 put, 29×2,=58 short 8600 put x2, 15=30. Debit 20

We have risk at 8600 but that seems as likely as the Loch Ness monster standing for Parliament (Quote me!) Max profit 250-20 =230

Here’s the risk graph: https://optioncreator.com/styasba

Was: 9200 put 39, 8950 puts 15×3 8850 puts 12×2, 8600 puts 7×2 Gives us 4, this is terrible!

Previously: 9200 put 73, 8950 puts 20.5,8850 puts 13.5, 8600 puts 7 Gives us 24.5 – well it’s in profit as we paid 20

Now 9200 put 57.5 8950 put 13.5 x3. 8850 puts 9.5 x 2, 8600 puts 5.5×2 Gives us 25 So, not a loser…

(Could have closed out as of 02 Sept: Trade 428 now 151-109= 42. but we let it run as we paid 20 and there could be up to ± 250 max profit )

Now: 9200 put 16.5, 8950 puts 3.5×3, 8850 puts 2.5 x2 8600 puts 1.5 x2 gives us a miserable 8

Best we could do: Wednesday gave us 37.5 +2.5×2, minus 3.5×2, 1.5×2 = 32.5 WIN! CLOSED

Trade 429 Raging Against the Machine

Maybe we get a dip, maybe the Moon is made of cheese. We find a trade that has moderate risk, generally and so we are again going with puts in a calendar ratio spread. Calendar: We sell a Sept 9150 put, 31, sell an October 9150 put, 65.We BUY an October 9250 put, 90.5. This gives us 90.5 minus 65+31= Credit 5.5

Sept 9150 put 55 Oct 9150 put 98.5. 9250 put 137.5 Ouch! That got weird. We are losing 10.5 ( late confession, the prices did NOT meet my usual criteria as we’d expect credit 20 – 30 to open typically)

Erratum: from last week: [ We BUY an October 6250 put,90.5. ] Apologies this should of course have read 9250 NOT 6250

Sept 9150 put 41 Oct 9150 put 86.5, 9250 put 123, gives us 36.5 -41= tiny profit of 1

Now Sept 9150 put 10.5, Oct 9250 put 79.5, 9150 put 53 Gives us 79.5- (10.5+53) = 16 WIN! We run it of course.

Now 94.5-58 =36.5 + opening credit 5.5= 42 WIN! CLOSED

Trade 430 Risk Reversal

A risk reversal? Yes, we sell a call to buy a put on the basis of a dropping market. Having previously stated we try to be market neutral, this will offer some protection for trade 429 should we see a bigger slide. So, those prices: 9300 call 43.5, 9100 put 42 So this gives us a tiny credit 1.5. There’s quite a lot of put exposure although we try to keep trades distinct and separate. Clearly risk to the upside may come back to bite me. It is interesting to note the overall position in the manner of the esteemed Charles Cottle (gotta love his LinkedIn profile listing languages: Options Greek )

Message sent 02 Sept by yours truly: Trade 430 we could close out for very respectable profit here: 9300 call is 23 the 9100 put is 65, gives us a nice 42, plus our 1.5 credit.

Would YOU close out or do you think there’s more to come?

Now 9300 call 31, 9100 put 30 So, in the real world we’d have happily closed out. We run for fun. WIN!

We’d closed out because of this 9300 call 42.5, 9100 put 7 This was not unexpected loss of 34 CLOSED

Trade 431 Iron Butterfly Time?

An ‘iron’ strategy has both calls and puts so here we sell the straddle 9200 call 78.5, 9200 put 57.5, we BUY strangle 9300 call 31, 9100 put 30. We make our max profit (136-61) 75 If FTSE expires in 2 weeks at 9200. Max loss 100- 75 =25. No, this would not be my favourite position but we can mitigate losses/close out early if things get crazy. We’re here to demonstrate real trades warts and all.

9200 call 112 9200 put 16.5 9300 call 42.5, 9100 put 7. 118.5 minus 49.5= 68. Our credit 75, tiny profit.

Expiry 9210 gives us: 9200 call 11, 9200 put 0 9300 call 0 9100 put 0 We took in 75 and we have a loss of 11 . MASSIVE 64 WIN! CLOSED

Trade 432 October Calls -pun intended! It’s a Put Position

Big and cheap is how we roll: big rewards, low cost, moderate risk. Here’s what we have: 2 ways to look at this: 2 put ratio spreads or a put butterfly paid in part by deep (7%) OTM puts.

Here’s the numbers, and strikes: buy 9400 put 149, sell 9200 put 64.5 x2, buy 9000 put 31, sell 8650 put 13.5 x2 So we pay 20+ 4= 24 And cross fingers! It’s horrible in this absurd market, but we have no upside risk. Logic of the trade, max reward 200 possibility of loss moderate.

Now: 9400 put 186, 9200 put 74, 9000 put 29.5, 8650 put 11 Crunching those numbers: 186+ 28.5 – ( 74×2 + 11×2) = 214.5- 170= 44.5 WIN!

While this has made nearly 100% in one scenario we’d close out, but here we will run it for the big bucks. THIS is how great options can be.

Trade 433 A Clever Trick- Don’t Try This With Stocks (You can’t)

So 429 had this outcome(we now have a long 9250/9150 put spread) : 94.5-58 =36.5 + opening credit 5.5= 42 WIN! CLOSED

What if we sell the Oct 9250 put for 94.5? What if we buy the November 9250/9150 put spread to protect our short Oct 9150 put? That costs 147.5-108.5= 39. We trouser 94.5-39= 55.5

Our position once again, we have a calendar ratio spread- 2 short puts one long put at the higher strike 9250.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com.

If there is anything you’d like help with, we all started somewhere and yes, it can be baffling. There are no stupid questions

All opinions expressed here are not to be taken too seriously and all of the trades are for educational purposes only.