That Was The Week A Lot Grabbed Our Attention

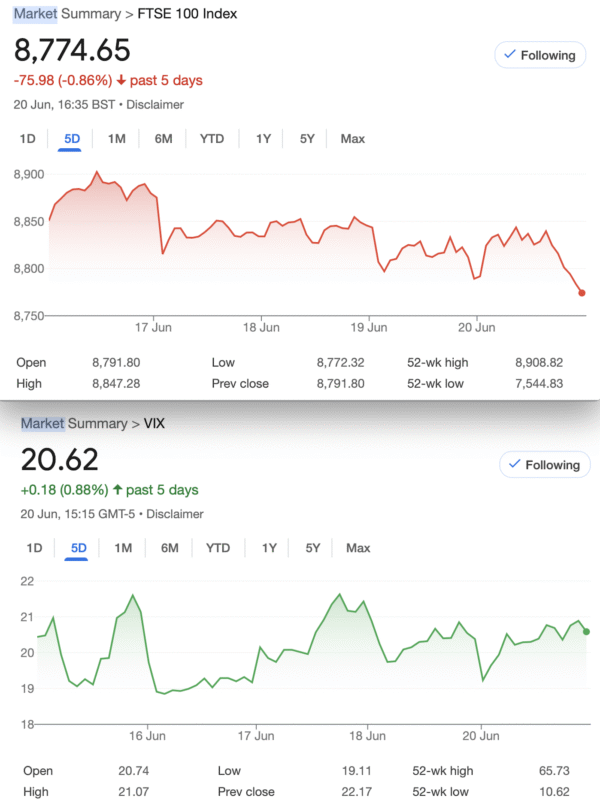

Interest rates stayed the same at 4.25%.The US also held rates. Inflation was grim and numbers fudged again. Honestly the basket of goods is from another level of silliness. Summer Solstice was a sight to behold for a change. Tasty Trade were in town. Sadly, yours truly took advice and declined the invitation due to the oppressive heat. By all accounts Tom was mighty impressive. What they have done for options in the US really has yet to translate here, in part due to our reluctance to change and offer sophisticated platforms. While not everyone is comfortable using online platforms for financial transactions, it’s not the future, it’s the here and now. Perhaps the spread betters will start to offer more options, although IG now seems to have a Tasty Trade stand alone platform. Unable to post the link, Google it please!

We have some trades in trouble at expiry and we’ll take a look at how we can adjust, and how leaving things to expiry day can work against you*.

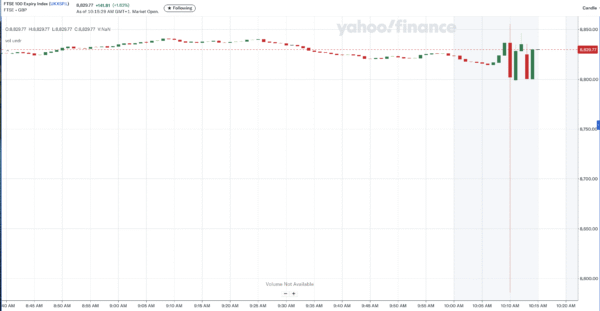

Hope you can see the massive candle wick(or tail) dropped at the 10.10 auction open by 300 points. A reminder PIN risk is when you risk your options being ‘pinned’ :called away or put to you. Exercised or assigned the stock, but when it’s the index it settles at £10 a point. Of course if your options were out of the money no problemo. So 8230 was the number, and you always need to remember that the expiry for FTSE is at 10:00 am the 3rd Friday of the month. (Yes, it’s possible to forget! ) Other derivatives may have different expiries, always check

Hope you can see the massive candle wick(or tail) dropped at the 10.10 auction open by 300 points. A reminder PIN risk is when you risk your options being ‘pinned’ :called away or put to you. Exercised or assigned the stock, but when it’s the index it settles at £10 a point. Of course if your options were out of the money no problemo. So 8230 was the number, and you always need to remember that the expiry for FTSE is at 10:00 am the 3rd Friday of the month. (Yes, it’s possible to forget! ) Other derivatives may have different expiries, always check

In The Inbox

Sorry about the link but there is a London Options Traders Group, not connected with us, but any options stuff is better than none.

CBOE( The Options Institute) https://www.cboe.com/optionsinstitute/?utm_source=mcae&utm_medium=email&utm_campaign=derivatives_digest_newsletter&utm_content=email_type-thought_leadership-see_more

As always YouTube has some excellent content and this guy digs deeper into the government stats: https://youtu.be/cozw2gEterc?si=R02k2SXB0mCOSAgH

The cynic in me relishes this content and while it’s only politicians playing games as they have always done, it’s good to hold their feet to the fire sometimes. We’re not complete idiots!

Distraction Trades

ADA was $0.6361 now $0.5821

XRP was $2.1700 now $2.1392 . All a bit uninteresting. Precious metals are in the spotlight again. My silver investment was up 12% at one point

DAX : Choppy weird market 2 trades 250 Nett. 3 days no entries!

UK Gilts Were £16.07 now £16.06 This is based on the Vanguard ETF, not a lot of love. It’s hard to know whose government’s debt is the worst.

Legacy Trades 415-419 and 420

*So currently there is only 415 that warrants rolling into the next month and apologies that yours truly could not find better trades. Trade 418 was an outright loss, being the wrong trade for the situation. Expecting an unpredictable set of circumstances to oblige is not a strategy.

Trade 415 Is The Optimism Justified?

We don’t mind being wrong, in fact many of the trades here are based on the premise of ‘not being right’. So here we take advantage of theta with a juiced up ratio calendar spread. We sell the June 8650 call for 132, and we buy the July 8500 call for 294.5, and sell the 8650 for 187.5 call giving us risk at 8800. Thus we have 132+187.5= 319.5, minus 294.5 =25 Credit Logic of the trade -we can be right up to 8775 and below. We are selling 2 options and buying one, so a lot of time decay working for us. There is of course the strong possibility of FTSE going ‘postal’ again and hitting new highs. We will have opportunities along the way to close out.

How It Went Wrong And What To Do:

Jun 8650 call 162 July 8500 call 335.5, July 8650 call 225.5 gives us a grand total of minus 52. Remember we took in a credit of 25. This trade needs time to mellow

This has yet to show a profit this week the June 8650 call 176.5 The July 8650 call 248, the 8500 call 368 gives us minus 56.5 (against our credit 25) 31.5 loss

Last week the jun 8650 call is 205.5 The July 8500/8650 long call spread 397.5, 270.5= 127.5, giving us a loss of 205.5-127.5= 78 Ouch!

Was: jun 8650 call 210, July 8500 412.5 8650 is 282.5 So we have the July spread worth 130, but the June call is worth 210. Minus 80

At expiry, the 8650 call went out for 180.We took in a credit 25. So a loss of 155. However:

We’re proud owners of the 8500/8650 call spread(worth 126 ) and we can get our 155 back. We sell the July 8700 call for 174.5, giving us 19.5 credit. So now we have risk at 8850 and Trade 415a

Trade 416 We Go Cheap

We want to own some puts but don’t want to pay in case we’re totally wrong, so here we buy a put spread and sell a very much further out put to help pay for it.Thus we have long 8500 put 61.5, short 8400 put 46.5 and short the 7800 put 13.5. At expiry if the index is near 8500 we will take a view and a profit. The spread costs a measly 15 so with the credit from selling the 7800 put we pay 1.5 for this, and relax. We have risk at 7700 but in this market the frenzy of buying the dip is forever at play. (The recent low was around 7500 )

8500 put 23.5, 8400 put 16.5, the 7800 put 5 gives us a credit of 2! As we paid 1.5 we are looking at a 33% profit. Take that, stock pickers!

Ugly and sad! 8500 put 9, 8400 put 6.5, 7800 put 2 Gives us a ha’penny. (NB we now have 73 up and only 43 down days this year to date)

Worth Zip!

Expiry was not kind to us. LOSER !

Trade 417 Why Not Strangle the FTSE?

I do not speak metaphorically either! Given the random nature of the markets let’s go with a strangle with equal pricing. We can get premiums of 23.5 on either side by selling the 8950 call and the 8500 put. Thus we have risk at 8453 and 8997.We aim to keep the full 47. It’s not the best time given contraction in volatility but it’s hard to make a reasonable assessment of the unreasonable.( These are for June options with 20 days to expiry)

8500 put 9 and 8950 call 18 We could close this for a cost of 27 and take our 20 profit As always we run to expiry and maybe we get the full 100%

Now 14 for the call and 9 for the put=23. Run to expiry, what could go wrong?

WIN! We claim the full 47

Trade 418 More Neutrality?

It’s time again for the crazy stuff, the boredom trades and the limited potential trade. It’s a ratio calendar straddle. (Yawn…… I hear you). We will buy the near month 8850 straddle calls 55, puts 67. July 8850 straddle calls 128.5, puts 116.5. All in gives us a penny credit when we buy 2 June straddles and sell 1 July straddle. The only way this works is if there’s a decent seized move, so it’s not looking promising. However we need to acknowledge that markets do occasionally drop when actuality hits the fan. This is when Deltas and Gamma work for us, while Theta snaps at our heels

July straddle is now 243, the June straddle 110( we have 2 ) =220. Losing, in fact leaking cash, now a loss 23

There was no point running this to expiry THAT is not how this works, we need action within a few trading days Woeful 50+ LOSER!

Trade 419. Give me a Clue Here!

As June options expire on 20th, this is not something we normally trade, however there are ways of doing this, but not with FTSE https://youtu.be/mUweXxqBtrI?si=a4jgGT7eVTGB0mCl

So the plan for this is to sell an iron condor- short call spread and short put spread, with 7 DTE (Days to Expiry). The numbers simply don’t pan out due to the lack of volatility on FTSE, however as his strikes, he claims have never been hit using his simple formula, we can sell a strangle. The formula? We take the sum of the call and put at the money, ie a straddle, and multiply it x2. We know the 8850 straddle is 110, so we look for the strikes above and below 8850 ± 220. Gives us 8625, and 9075. Of course there’s almost nothing at 9075. So again going with a strangle we sell put at 8625= 14.5 and call at 8975 =9.5. Of course this is naked and therefore risk is considerable but there’s a fair margin of comfort with the puts.

Apologies we cannot find any inspirational winners or even juicy strategies. Why? It’s personal.

WIN! Collect the full 24

Trade 420

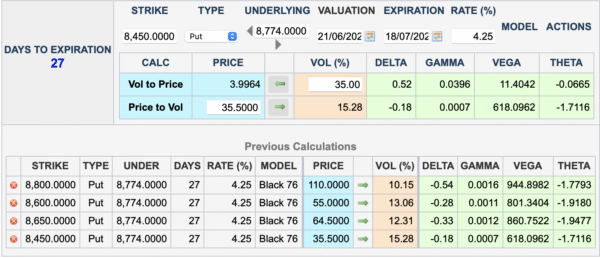

June punished us for poor trade selection, but sometimes the strangle is the ‘go to’ trade. So, what can we do for July? We have 27 days to expiry. Here’s a double put ratio spread.

8800 put 110 8600 puts 55 8650 puts 64.5, 8450 puts 35.5. We buy 1 8800 put and sell 2 8600s. We also buy the 8650 put and sell 2 of the 8450 puts credit 6.5

This makes a profit down to 8300 and to the upside has zero risk. Anything lower than 8800 and above 8300 is our target, and we can adjust along the way.

We now have 420 and 415a

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling. There are no stupid questions

Pay attention I will only say this once!

The other possibility for repair of Trade 215 is as follows:

We have a loss of 155 and a July long 8500/8650 put spread. We SELL the 8500 put for 338.5 and buy the August 8450/8650 put spread for 157.

We now have credit 181.5 so our loss is now a small credit 24.5 and a good looking call ratio calendar spread with risk at 8850.

No puts!!!!! It’s calls only