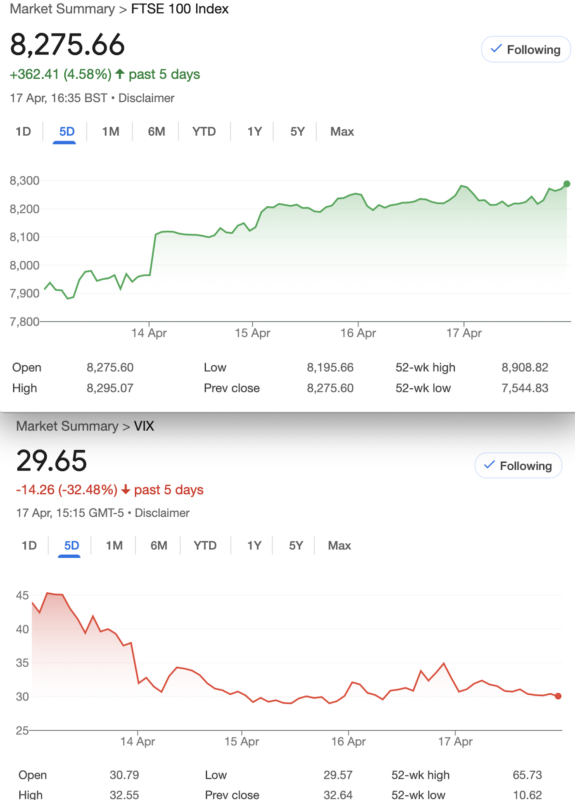

That Was The Week FTSE Melted UP, S&P Was Flat

So, some concerns as the US‘s big index S&P500 was up just 0.52% on the week. However the magnificent 7 have taken hits recently, more especially Tesla has become a pariah. But, while Tesla may make a good product it’s hard to come back from being deeply unpopular with your target market. Ironic that Elon was a champion of the environment and then joined Team Armageddon. Sorry! Enough of the politics. Yours truly, like most, has been thrown curve after curve with this market and it may be sensible to build a big defence in the form of some far dated Put strategies. We continue to make trades here in the name of education and enlightenment but we need to be aware of the real possibility of a major problem.

A wise old trader once told me that if a market move is political it’s temporary, if it’s financial it’s long term. Think’ There’s no market rally without the banks’. Banks created the 2008 great financial crisis, the credit crunch, choose your own term. Note, also that volatility spikes tend to be short lived too as this week’s VIX chart amply demonstrates. The remaining Put sellers still solvent will be making $$$. Stepping back for the chart of FTSE longer term it seems we had a ‘head and shoulders’ pattern from late January to start April. It may be coincidence.

Happy Easter

Expiry Special

Here’s the link to this week’s expiry at 8200.88 : https://finance.yahoo.com/quote/UKXSP.L/

On a personal note after exposing my own folly last week I decided NOT to run my 8300/8200 put ratio spread to expiry. It would have made 99, I got 35. The trade was a credit 14 to open, so it’s not desperate but I had predicted this expiry weeks ago! Making predictions that are correct is even worse than being wrong. I’ve been told in the past that perhaps close out half of my positions and leave the rest to capture the riskier higher reward. We each of us need to be slightly uncomfortable in trading, not blasé nor frozen by fear. Easy to go either way. This trade, placed on 3rd April has been a horror show, and it’s only human to seek comfort in closing for a decent profit. My own weakness is beating myself up, and living with constant doubt. It’s not that bad!

In The Inbox

A tempting invitation to those of you who like to spice things up in the options world. It’s a Zoom meet all about 0DTE options. I can see the attraction of taking long spread positions but the cynical me thinks there are no free lunches and you’re likely to be right and still not make much profit. Prove me wrong!

https://cboe.zoom.us/webinar/register/WN_XCfN6OFzR-O4Lsg__3yJoQ#/registration

A detour off the beaten track but the government’s tax plans and Rachel from Accounts alarming proposals may seriously put a dent in many sectors of the market. Labour claim to want to ‘reinvigorate’ the UK economy with massive building programmes but want the taxes too . https://www.cityam.com/inheritance-tax-changes-threaten-uks-infrastructure-push/

You may recall farmers made a big deal about this Business Property Relief being abolished but the unintended consequences may be brutal. Who’d ever try to start a bricks and mortar business in the UK? Builders, we salute you. Farmers too.

Distraction Trades

ADA was $0.6391 now $0.6126

XRP was $2.0597 now $2.0773 Cardano again lagging behind

DAX : short week 2 wins, 2 no entry days +200 nett.

UK Gilts Were £15.80 now £16.00 This is based on the Vanguard ETF

Legacy trades 406-410,Expiry and Trade 411

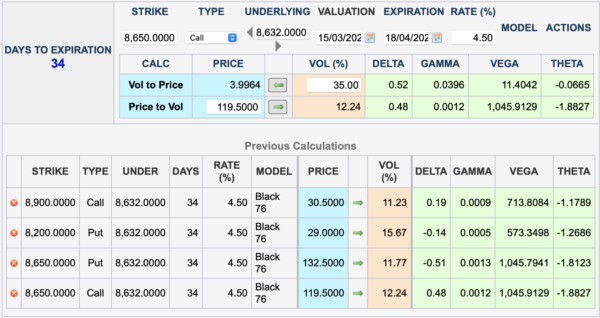

Trade 406 Straddle Versus Strangle(April expiries)

Here’s a bit of fun and each week we’ll update what’s winning and what isn’t. So….. the 8650 straddle: call 119.5 and put 132.5 =252. Strangle: 8900 call 30.5 8200 put 29. To keep premiums level we sell 4 strangles against 1 straddle, which then gives us 252 against 238

Remember we use: https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html

What’s YOUR prediction?

Strangle: 8900 call 21, 8200 put 19.( credit 59.5 -40= 19.5) The straddle 110.5 and 106.5 (credit 252- 217= 35)

However: We sold 4 strangles, so that gives us 19×4= 76, trouncing the straddle

This week: 8900 call, 12 8200 put, 10 Profit: 59.5-22= 37.5×4 =150 8650 straddle 95+83.5 Profit: 252- 178.5= 73.5

It’s not even April and the strangle has done brilliantly. We’d take that and close out, but the straddle struggles to keep up. Given the multiple strangles this is no surprise.

BOOM!

My argument- we’d have closed out the strangles but left the straddle, would give us Negative 610( Credit to open 252) Loss of 358 We are not done yet, this can be rolled into consecutive months) Had we kept the strangles the loss would have been 241.5×4 =966. however, we can cherry pick exits here and the strangles being a multiple of 4 would have given us a lot of pain, but again these can be rolled.

Last week: 2.5 and 682 for the straddle = 684.5. Strangle (0.5 and 260) x 4 =1042 Both losers

This week straddle = 450-252= 198 LOSS Strangle made 100% after another insane week 59.5×4= 238 WIN!

Did we prove anything? Strangles beat straddles? We are in crazy times, so no.

Trade 407 Building On A Legacy

With trade 405 we inherited a juicy long put spread 8800/8650 so let’s have fun morphing this into something more interesting than banking a plain vanilla 70. We get spicy and sell another 8650 put for 106.5. ( Much more interesting than 70!) Let’s add some downside protection too. We have risk at 8500, so let’s buy that put for 57 and sell 2×8350 puts (31.5×2) a credit 6

We now have risk at 8350 and a war chest of 106.5+6= 112.5 should we need to adjust

The 8800/8650 spread is now 169.5, 83.5= 86. The long 8500 put is 38.5, and the short 8350 puts are 18.5×2, gives us a credit of 1.5 -Is it all going too well?

So let’s adjust this? Not a great idea. 8800 put, 744.5, 8650 put 600(x2). 8500put, 463 8350put 340(x2) Gives us 1207.5 minus 1880= 672.5 Negative

OK this could wipe out a few month profits but we’ll stick with it for now, as trying to adjust this in the real world would not give us sensible prices.

Last week: 8800/8650 ratio spread 830.5, 682(x2)= negative 533.5 the next ratio spread: 8500 put 534.5 8350puts 391.5 (x2)= negative 248.5 LOSS 782

Time to panic? No……..

Now 8800, 600, 8650×2 =900, loss 300. 8500 put, 300, 8350puts 150 x2 =0 ( we still had a credit 112.5 ) 187.5 loss

A classic example of how to make money while sitting on your hands ( the spread of course would have made 150 with zero effort). LOSER!

Trade408 Risk Reversal

KISS….. Keep It Simple, Stupid! I need no reminders of my own stupidity (who manages to tip cornflakes into their empty coffee mug?) We are getting concerned about the market taking a dive but don’t want too much upside risk. As always we don’t want to pay for a trade. We go with a risk reversal selling the call and buying a put. Sell 8800 call 31.5 and buy 8450 put f0r 30. Credit 1.5

BIG BADA BOOM! So, having suggested this be closed out for 35 on Monday for a quick turnaround, the smart money would have given us 415.5

Last week’s prices 1 and 486=485, a huge win had we run it

Cannot beat that, it pays for any other losses, but we’re not counting

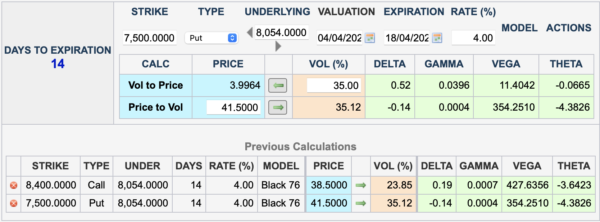

Trade 409 Sell The Spike

Volatility, whilst elevated, favours the seller. VIX (or any volatility index) is mean reverting. so the only game in town is selling premium. How safe is this? Another strangle, here comprising 7500 puts, 41.5, and 8400 calls, 38.5. We keep an eagle eye on this, but taking in 80 for a strangle with the following spicy vol and sensible deltas…

Was : 8.5 for the call, 27 for the Put. Looks like we win! (80-8.5 and 27) =44.5 Again we could run this as it could make the full 100% of the premium sold

This week: WIN! Phew! Collect the full 80.

Trade410 Calendar Ratio Put Spread. A CalP.Rat (Catchy enough?)

Rinse and repeat? We go with the aforementioned calendar ratio spread which, given the 4.2 trading days remaining may do well. However we know this is a bonkers market and so caution is urged. We sell Apr 7600 put for 36.5. We sell the May 7600 put for 126. Then we buy the May 7750 put for 164. It’s a tiny debit (164- (126+36.5)=1.5

Logic of the trade: 7600 looks like a key support level (with luck) we could make a nice moderately safe small profit with the further choice of doing something with the May put spread. Such are the quirks of the Calpy Rat! Should the market melt up, we stand to make a profit, or at least not lose our 1.5

Options prices here: https://www.ice.com/report/265

This week: 50.5 and 35.5= 15(minus 1.5 debit)=13.5 WIN! Caveat: there was a chance to close out earlier…… for even less. Would you keep this in your back pocket?

Trade411 The Devil’s Pitchfork

Ok we have used this once or twice before, and it looks terrifying, but it’s not. It’s the pitchfork. Simply we add up the put and call prices At The Money = 109.5,199.5= 309. Subtract this from the current ATM level =8275 although for convenience we use 8000 and at this level we have the 8000 strike call at 279, and Three times the 8000 put which is 95= 285. We sell these 4 options for credit 279+285= 564. Logic of the trade? It will benefit from a drop in volatility and might not be too awful if things get crazy again.

As you can see the deltas are -0.94 for the call and for the puts +( 0.28×3)= +0.84. So we are negative ONLY 0.1 Deltas. Remember when you SELL puts, you create POSITIVE DELTA.

Frankly the volatility is not wild so it may be too risky to the upside.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling. There are no stupid questions