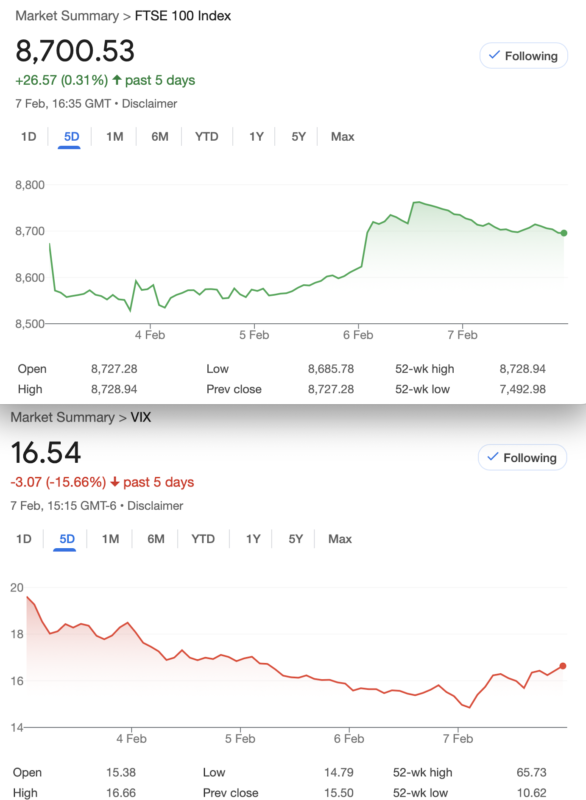

That Was The Week -Hopes for a Big Drop Dashed, For Now!

More darkness descends on America, does anyone really care? Trump’s flip flops are a ploy as he is testing the waters, probing and pushing limits. Testing relationships as the US withdraws from IMF and World Bank. Are they the benign institutions we think they are? Are they the bulwark between normality and total corruption? Meanwhile, in a non event nobody cares about, the BofE dropped rates to 4.5%. Anyone monitoring their large options portfolio may be looking at Rho and thinking ‘ nothing’s changed’. The banks will be happy as they find innovative ways to juice profits, while passing on next to nothing to customers. Allegedly.

House prices hit another high, but unlike the Stockmarket we cannot live without housing. However, the amount of times a housing crash has been predicted is er, a lot. More out flows in January from UK funds, a billion apparently. UK growth estimates slashed by 50% to 0.75%. The UK even reversed tariffs on Chinese E-bikes. And, the Labour Party are starting to look like the Conservatives on steroids. So, if any of you are feeling bewildered, you are not in the minority, we live in in interesting times ( You may know this is actually a Chinese curse)

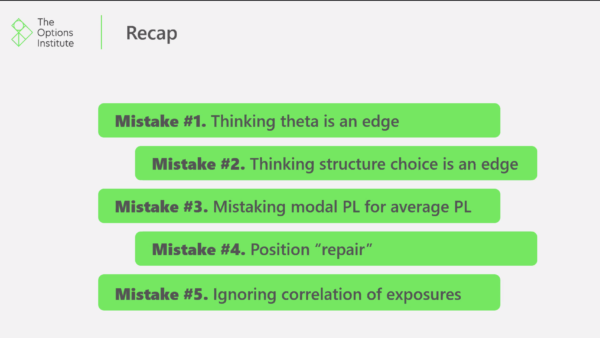

In the Inbox This Week, Seminar from CBOE: Euan Sinclair’s 5 Mistakes Traders Make

This summary needs a few words of explanation. Theta is an edge, but he rightly says gamma neutralises theta. Gamma increases during the expiry cycle until the last week when it jumps. But so does theta. It’s a problem if you’ve sold ITM options but if your options are going to expire for zero, it’s clearly not an issue. He says a strategy is a structure, and perhaps the wording is important. He does talk about equity options most of the time so perhaps we are better placed trading the index. GameStop options came up as a ‘meme stock’ of note and curiously when it dropped by about 30% so did the put volatility. Makes no sense right? That’s why we don’t trade meme stocks!

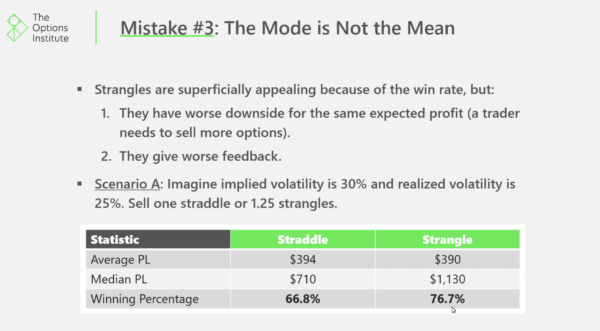

Position repair- the domain of such as Charles Cottle, he suggests there is no such thing and it’s simply a new trade. OK. Correlation of exposures is something we never ignore, and mostly we like to be delta neutral or at least well aware of how the components of each trade work. I’d be curious to know if anyone else saw this webinar, and their comments. Personally it left me cold but he’s the professor, and I’m the retail trader. I have never traded straddles on their own, but let’s test the professor’s 66.8% winner

Distraction Trades

ADA was $0.9341 now $0.6862

XRP was $2.9986 now $2.4007 Is this another demise in the crypto minnows?

DAX : 4 wins, 2 losers 1 break even(+30) 1 no entry nett: 460

UK Gilts were £16.10 now £16.21 On fire! Slight gain, again. This is based on the Vanguard ETF (not a recommendation)

Legacy Trades 396-400, and now……401

Trade 396 Calendar/Time Spreads

Our weapons of choice:

Jan 8200 call 83.5 Feb 8100 219, 8200 150 call spread. So we sell the Jan 8200 call and buy the Feb 8100 call and sell the 8200 call (83.5 minus 219-150)= 14.5 Thus we have a small credit 14.5 but that’s not the point. This is a trade with some flexibility and of course we have done these many times, it’s a combination of theta and a fair chunk of protection. We have zero downside risk, which is not a bad thing. Let’s hope calm heads prevail as the chances of economic growth are <zero, or slightly>zero.

Now the 8200 call for Jan 84.5, Feb 8100 235, 8200 call 164 gives us a debit 13.5 Caveat: This was placed before the crazies bought the market.

So the Jan expiry at 8495 made the call worth 295 against us. The feb call spread 442.5- 350= 92.5 A horrible loss. (Ok we took in tiny 14.5 credit)

So here’s a risky plan.

We buy back the 8200 call 350 and sell 2 8300 calls 262.5 gives us 525-350=175, mitigating our loss to 120, but with risk at 8500. This is risky as the market can get crazier than seems humanly possible.

Risky plan update, the 8200 call 328, the 8300 calls 239.5= 479, gives us 151 -could be worse and best case 8300 might not happen but 8400 would do nicely

However the FTSE is rising, fact is that somebody has the hots for it.

This is woeful MASSIVE LOSS 293 8200 call is 487, 8300 calls 390 (x2) Remember we could have swallowed the 78 loss

Now 8200 call 495 and 8300 call 397 x2 gives us 299 Ouch!

We run, for fun and see what we can do ( roll into March)

Trade397 Look Out Below – A Safer Play NB- February Prices

While we don’t love butterflies there are times when a modest trade with a modest return might be the prudent way to go. So as in the traditional sense we buy the 8300 put x1, sell the 8150 puts x2, and buy the 8000 put x1. This gives us 131.5+42.5= 174 minus 74×2= 148, gives us a cost of 26. Logic of the trade? Max profit 150-26=124, max loss limited to the amount paid 26. We may get a little spicy with this and do some adjustments, and comparisons with letting it run.

Now 39.5, 23.5×2, 16= 8.5 LOSER! 2 Courses of action, close out and lose 17.5 or run it and see what happens. A third way( thank you Tony Blair) would be to close out the 8150s we sold and the 8000 put that we own for a cost of 31, and then buy the 8500 put 95 and sell 2 8400 puts 60.5. Overall a cost of 5, though we’re already in it for the initial cost 26. We would now have a butterfly worth 39.5+95 minus 60.5 x2= 13.5

Running the trade gives us(Puts) 8300 31.5, 8150 16.5, (x2), 8000, 10= 8. (initial cost 26)

The third way(8500/8400/8300 put butterfly) now gives us 86+31.5 minus 51.5×2 =14 (initial cost 31)

Now: 8300 10 8150 6 8000 4, gives us 2

The third way 8500 put 26 8400 15 8300 10 gives us 6

This is frankly so far out of the money we’d close it and take the hit. LOSER!

Trade 398 What The Heck Can we Do?

Frankly this is such a whopping great absurdity I have no idea so if push comes to shove, I have no ideas other than: 8100 put 8800 call strangle for 20 per side. It’s better to go ahead and do something and say sorry later, is the perceived wisdom.

this week: 10 for the 8800 call and 14 for the 8100 put so we are doing ok as our initial credit is 40

Was: 30.5 for the 8800 call and and 5 for the 8100 put

Now: 24.5 and 3.5 It’s not a happy trade but it’s making a profit

Trade399 a Challenging new Trade Idea, Gearing Up

So, with a firm conviction that the worst trade is a long straddle, we look to test that hypothesis. We take a standard iron butterfly which sells the straddle and buys the outer ITM options. BUT! We sell 2 straddles instead of 1.

To clarify, we BUY the outer ITM Call 160, and Put 174.5. We SELL 2 each of the 8500 calls and puts. 95×2, 86,×2, gives us 334.5- 362, gives us a credit 27.5

Now, I’m going to be cheeky here and suggest you plot this yourselves, bearing in mind the buy/sell and quantities involved. You will see the profit zone giving a maximum 300 + our Credit. Is there a downside? We’ll address that in due course. So here’s the graphical calculator https://optioncreator.com/new

CAVEAT: This is not recommended and may get in a right pickle! You’re all aware that this is purely for educational purposes, and prices were at close on Friday: https://www.ice.com/report/265

Apologies, I sent an erroneous link to the options creator, but this has been a disaster. We have 206.5 and 26 for the straddle 8500 call and put. We have 295.5 and 64 for the wings. So here’s the maths: We sold 2 straddles which now cost 232.5×2= 465. Our long strangle is worth 359.5 a loss of 105.5.

That could have gone better.

Now the straddle is 293(x2) our LONG strangle 423 gives us a loss of 586-423= 163 ( OK we took in a lofty 27.5)

Trade 400

I’m stumped. Honestly this is completely new and, frankly, terrifying. Let’s tempt fate with a short 8800 call at 30.5 and a put ratio spread buying the 8600 for 47 and 8500 for 26(x2) gives us 5, +30.5 =35.5 Credit We have risk at 8835 and 8364.5

Now 24.5 and 34.5 minus 18.5 x2= Debit 27, our Credit was 35.5 A tiny glimmer of hope as our losing streak continues to dominate

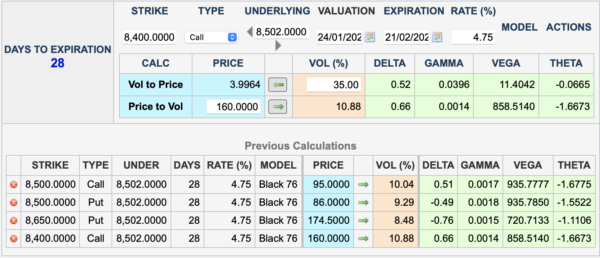

Trade 401

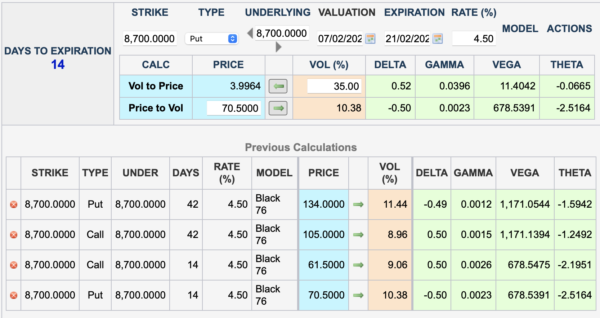

Let’s go with the esteemed Professor’s straddle

Feb expiry:

As you see the February prices at the top are miserably low, so we’d go with the March expiry but here’s the Greeks so we can watch the gamma /theta relationship. You can see they are both elevated for the Feb expiry.

Caveat: Really not recommended!

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.