That Was The Week Turkeys Met a Fiery Fate

Thanksgiving week tends to be a bit of a nothing for the Stockmarket, though the US ploughs higher still. Goldman Sachs state that growth in the UK may be 1.2% -up from 0.9%. Here’s the link: https://www.goldmansachs.com/insights/articles/uk-economic-growth-may-lag-expectations-in-2025?chl=em&plt=briefings&cid=1129&plc=body

I have stated many times that in my view growth equals debt. Are we good for ongoing issuance of debt? We’re a safe bet, we don’t default, and Charles III is not Henry VIII! However there is a very disturbing Youtube video: https://youtu.be/nNcNuDKSKAc?si=SwS6n5aan8nXwZFG

So, it amazes me how the wacky world of finance functions from government debt to taxation, to welfare benefits. The FCA is deemed incompetent, a step up from being passive enablers to all manner of shenanigans, allegedly. The taxman has yet again, taken on and beaten Harry Potter star Rupert Grint. He has some admirable form with HMRC which confirms magic remains the stuff of fantasy. Meanwhile as ‘Grinch’ Rachel Reeves stopped the Xmas fuel allowance for all pensioners, this sparked a backlash. Encouraged by Martin Lewis, pensioners are, en masse, claiming pension credit, which generally passports eligible claimants also to council tax reduction. The upshot of this will be a saving of the negative variety, to the tune of billions. Who knew there’d be a backlash? On the plus side the benefits paid out do not get salted away in the Caymans, they are spent locally.

Mea Culpa

Whilst I have from time to time mentioned the up day/down day count, my view of the ratio being 51% up is out of date. This is fairly comprehensive and makes sense : https://www.crestmontresearch.com/docs/Stock-Yo-Yo.pdf

Somehow Crestmont reminds me of the Wolf of Wall Street. However I think we can take this as a solid piece of data gathering. It also explains why I have continually been behind the curve regarding market outlook. Even our dreary little FTSE is more bullish than I believe. However this is a bit of a wake up:

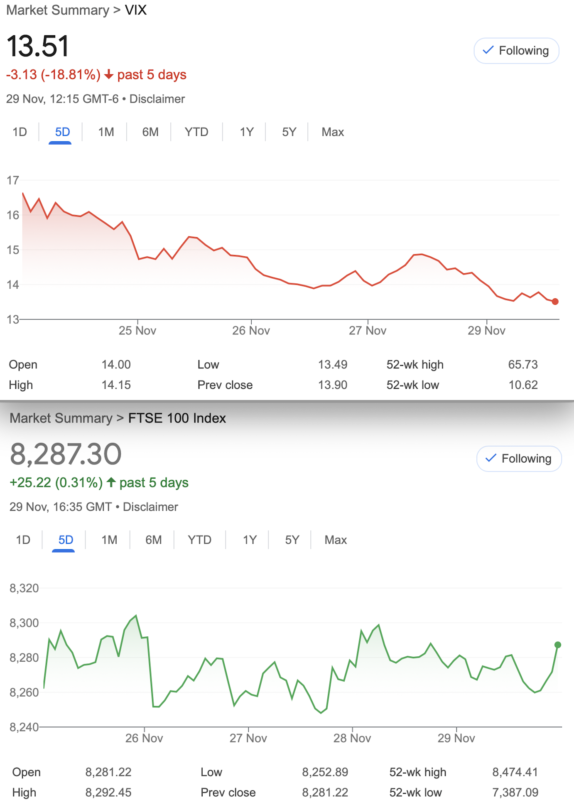

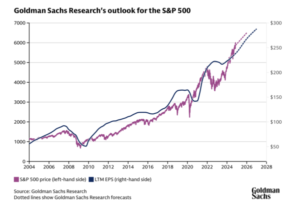

While FTSE has nearly doubled, the US is up sixfold. Is it any wonder people worldwide choose to invest in the US? Happily we plough our own furrow and as pure index options traders, have little interest in booming markets. That is for the likes of my pension fund managers. My stock picking is inversely proportional to profit. That is why I look at other investments from time to time but always come back to options for trading within timeframes that suit me.

Distraction Trades

ADA was $1.0659 now$1.0934

XRP was $1.5245 now $1.8882 Buyers still have an appetite for crypto.

DAX : 2 losers, -30×2, 1 break even +30, 2 wins, 290. Nett 260

UK Gilts were £16.34 now £16.54 Bond yields in the US eased too, meaning the value of the bond increases.

Legacy Trades 389,390 and new kid 391

Trade 389 What Can We Do In Light of the US election? Get Back To Market Normality

The Xmas effect or Santa rally, is it on this time around? Most market watchers know about this and the markets generally rise as the numbers show the economies are doing ok. We will go with a CALL BUTTERFLY

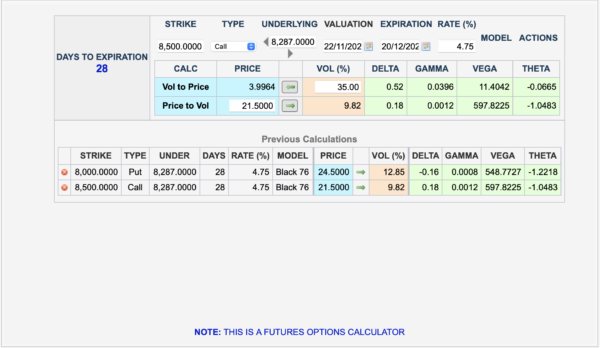

Here’s the trade: We buy the( December) 8300 call for 40. We sell 2x the 8450 call 16 x2, and we buy the 8600 call for 6.5. Our cost therefore: 40+6.5 minus 32= 14.5

The ONLY risk here is our premium paid 14.5

Previous week: 30.5, 10.5(x2), 4. Gives us 13.5 Christmas is coming !

Last week 8300 call 88, 8450 calls x2 31.5, 8600 call 10 Gives us 88+10 =98, minus 63= 25 We’re in profit but it runs to expiry

Now: 8300 call 81.5, 8450 calls x2, 24, 8600 call, 5.5, gives us 39

Trade390 Can we use Legacy Positions again?

Trade 387 leaves us those two spreads that we own, so we have zero risk and could run them, with one, possibly both making no profit. Or……….

We leave the 8300/8400 call spread for the Santa rally, it’s only worth 15.5 and could make 100.However, the put spread… we sell the 8200 put that we own, for a massive 168.5 and be buy in January the following put spread 8250 216, 8100 137, for 79. So we have a handsome profit(168.5-79= 89.5) still and another spicy calendar ratio trade. Our risk is at 7950 and nothing is set in stone. Santa may not give us the rally this year.

In summary we are long: Dec 8300 call. We are short Dec 8400 call Dec 8100 put. Long Jan 8250 put, short 8100 put.

Here’s the graph of the position https://optioncreator.com/strt35v

Last week: The December call spread 88-46= 42 (Remember we inherited this and run it for zero cost). The short put Dec 8100 37.5 our LONG Jan put spread 101-61.5= 39.5. In credit for 2

Now: December call spread 81.5-37.5= 44. The short put Dec 22.5, our LONG Jan put spread 8250put, 82.5, 8100 put 47.5= 35=12.5 credit

Trade 391

So, currently we have a long call butterfly, a long call spread and a calendar put ratio spread, shall we try something nuts? Let’s go naked with a strangle.

Here we SELL both a naked put and naked call. It’s not as bad as being naked in one direction and we have simple exit criteria in the event of a problem. IF the premium on one side trebles, we close out and create a new trade relative to the new market level. Tasty Trade have long been advocates of the 1 sigma strangle, which means using options with a Delta around 0.16. It’s simple, we have a plan we take in a credit of 45.5, so if the puts, for example, go to 73.5, we close out. Our loss is 18, we look to place another short put and possibly roll down the call.

Entry criteria? The levels are the most recent extremes of Bollinger bands, the Deltas are around .16, the premiums are decent and we are in the big time decay period <30 days to expiry.

Now 14 for the put and 15 for the call =31 We sold this for 46. So, we’re 15 to the good. Boring, predictable? Profitable? All three, mostly.

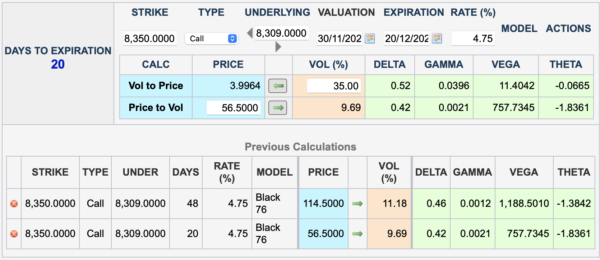

Trade392 November fades (but the Weather Gets Weirder)

It’s now a choice between December and January expiries but with the holiday looming it’s 48 days away but only 32 trading days

This is NOT a recommended trade as entry criteria are not public domain AFAIK. Price Headley the acclaimed trader and author of many options books used to say the following: On occasion it is advantageous in a calendar spread to sell the far month IF volatility is skewed. A conventional calendar spread is simply buying the far month and selling the near month because of the time decay. Here we see higher volatility in the far month Jan (to be expected) and hefty theta in the near month. BUT, we have 2 front month(Dec) calls giving us an overall delta of 84-46= 38, or .38. In addition we have Gamma of 21×2 versus 12. This means if there’s a big intraday move in the next few weeks, the near month calls will move far more than the far month call. It needs a big rise.

The numbers here: 114.5 and 56.5 x2= 1.5 Credit

We have realistically a week or so for this to do anything and it’s purely for demonstration and NOT a trade I would take without more of Mr Headley’s knowledge. It may get ugly! ( I hope it does!)

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.