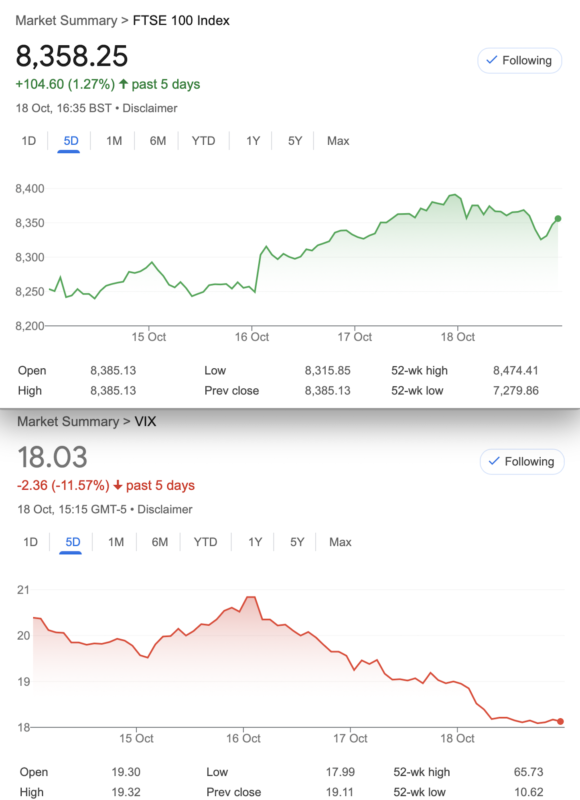

That Was The Week FTSE Deviated From The ‘Glidepath’

So, inflation, they say, is below 2% Just how credible is this number when one considers the nonsense that is the ‘basket of goods’? The fact is that airline tickets were dramatically cheaper and we have a new entry into the ‘basket’……. Air Fryers.Yes, air fryers. Talk about cherry picking! The world and his wife bought an air fryer ages ago and many can be found on sale on Facebook Marketplace. A few mouse clicks showed 120 used air fryers available within a 5 mile radius of yours truly. However the selective process of including yesterday’s ‘must have’ suggests to me this is a cheap shot. Pun intended. I get the impression there was much disdain over this inflation number’s veracity. And, it’s not as if we buy plane tickets every week.

Moving on from the general annoyance and the previous week’s missive inviting the FTSE lower, which proved to be folly. Not sure if it’s ever been mentioned that prediction is a fool’s errand. Gut can be a great asset and while it’s ok to be constantly slightly uncomfortable when you have a few positions, it can be helpful avoiding disasters. None of our trades is a disaster. Our losses are microscopic in the scheme of things. Rant over.

In the Inbox

A curious take on equity options, as most people place trades in anticipation of a move with long straddles/strangles or spreads. iVolatility is a good resource and this article is thought provoking though we stick with the index here for the purpose of avoiding complications. However it’s a 2 minute read.

https://www.ivolatility.com/news/3026

Here’s a taste of the future. https://fullertreacymoney.substack.com/p/the-promise-of-fusion?utm_source=post-email-title&publication_id=1289696&post_id=150424990&utm_campaign=email-post-title&isFreemail=true&r=21hwak&triedRedirect=true&utm_medium=email

I’ve been reading Mr Treacy’s whipsmart commentaries for a long time now, and it’s worth being a free subscriber if you have the time- there can be some lengthy stuff too.

Distraction Trades

ADA was $0.3550 now $0.3535

XRP was $0.5400 now $0.5468 Ripple still ahead of our preferred Cardano -paint drying again. I still believe crypto is a punt rather than an investment.

DAX : Top week! 5 wins, 2 losers Nett: 360

UK Gilts were £16.54 now £016.80 The expectation in a rate cut has boosted Gilts. The US has no such position.

Legacy Trades 383- 386 and now 387

Trade 383 October Can Get Spicy And The Omens Are…. Oh Wait, We have No idea!

We had a lot of fun with the ludicrous 3×1. Let’s go again and try to keep the risk level out of harm’s way, though venturing in the murky depths can mean missing out on the sunlit uplands of juicy profits. Let’s see. Again we sell 3 puts and buy 1. We sell 3 of the 7800 puts for 15 and buy the 8100 put for 45.5. Where’s our risk? sort of 7500-ish. Now that’s a fair degree of comfort with not a lot of likelihood for success. And, let’s not forget it costs us a ha’penny and requires some margin. Remember a very competent, very large hedge fund got blown up with the 3×1 trades, but with calls

Previously: 18 and 6.5×3 Just wait! ………….

Was: 24 and 7.5 (x3) We’re in profit!

Was: 9 and 2.5(x3)

Sadly a loss of a ha’penny

Trade 384 A multi Leg Classic But Cheesy Trade

In actuality we have 14.2 trading days for the October expiry and things are looking a bit sleepy. We like the idea that FTSE may take a gentle glide down to the 8100-8200 area but of course prediction is silly. Looking at the chances of this, however, the open interest suggests this may be the landing area for expiry. Here’s the strikes and prices for a CALL butterfly.

8100 257.5 8200 170.5 8300 98.5 Remember we buy the wings, sell the body, which is the 8200 strike x2. Thus we have 356- 341 = 15. Expiry at 8200 would give us 100 so it’s not bad reward for a max risk 15

*[ Should you want a bigger bang you can get the 8000/8150/8300 call butterfly for 24.5 ] (305.5, 172(x2), 68 )= 29.5 ( bigger bang for buck) NOW 44 *

Last week: 8100 214.5, 8200 133, 8300 68 Thus 214.5+68 = 282.5, minus 133×2= 266 = 16.5 A 10% profit!Obviously we’re looking for a tad more than a penny ha’penny

This week: 8100 166.5, 8200 81.5(x2), 8300 26 =29.5 100% profit We run to expiry of course. Both of these could get very juicy in expiry week.

At expiry this was a LOSER However 100% profit? We’d have taken that

Trade 385 – The Calendar Zone

Having a trawl through the options chain https://www.ice.com/report/265 for October and November made me think of the following trade, using the massive time decay of near month and the cost of the next month’s spreads. Here we go: We SELL the October strangle (8100 put for 24 and 8400 call for 28) and we BUY in November the 8200/8100 put spread, those prices 95 and 68.5= 26.5. for the call spread we buy the 8350 call and sell the 8400 call 109- 86= 23. So we have a credit of 24+28= 52, and a cost of 26.5+23= 49.5.

Eagle eyed traders will note this is a small credit 2.5, our risk at 8450 and 8000. We may well close out before expiry if it goes to plan. Max profit 100, or 50.This week, the October strangle (sounds like a Hitchcock film!) 8100 put 9 and 8400 call 5.5 November IC 8200 put 85.5, 8100 put 58.5 58.5= 27 8350call 74, 8400call 54=20. So, we have a debit for Oct of 14.5 and credit 47 for the November Iron Condor, gives us 32.5 While this is a nice win 30 we will run it though, the October strangle can only lose a maximum 14.5 . I’d be inclined to think that it may be prudent to close out, or roll the strangle, or the entire trade!

We could have got about 40 during the week but expiry (8365±) meant the strangle went out for zero, giving us : 25.5 for the call spread and 16.5 for the put spread

Trade 386 November And The Ominous US Election Cloud

Sticking to the knitting, and regulars here know we love a put ratio spread. The choices are huge but trade selection comes down to: Do you want a big chunk of premium? Are you happy to place a low or zero cost trade that could give bigger rewards?. Where do you think is an acceptable level at which to have risk that needs to be managed.? This time it’s a low cost 8200/8000 put ratio spread and as it is long at 8200 and short x2 at 8000 this means risk is at 7800, currently about 6% below the futures price. We pay 85.5 for the 8200 put and collect 40.5 x2 for the short 8000 puts. Our cost is thus 4.5 with risk 6% below the market, zero risk from 7801 upwards. Should the market go very South, we’ll look at adjustments. Let’s hope we get a delicious expiry in the meanwhile.

Surprisingly a LOSER We paid 4.5 so we could afford to lose one of these every month forever!

Trade387 What to Do With A legacy Trade

We will start from the position of using the spreads we own from trade 385.

8350/8400 calls (109 and 83.5) and 8200/8100 put spread (47 and 30.5)

OK here’s PLAN A. This requires that we sell the long call and long put for 109+47= 156. We BUY the Dec 8300/8400 call spread for 203-143= 60, and the 8200/8100 put spread for 84 -63.5=20.5. Now the short leg of our ratio trades ( effectively a strangle) is in November and the long spreads(effectively a long iron condor) in December, we have, in addition, a credit of 156- (60+20.5)= 75.5.

Confused? I suggest reading through in stages. 1. Selling the Nov long call and long put and 2. Buying the protective spreads in December. We have risk at 8500 and 8000

Given that we have some mitigation with theta as these are spreads, we could look to time the put side better. Next week may be a very different proposition.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.

Trade 386 November And The Ominous US Election Cloud

Sticking to the knitting, and regulars here know we love a put ratio spread. The choices are huge but trade selection comes down to: Do you want a big chunk of premium? Are you happy to place a low or zero cost trade that could give bigger rewards?. Where do you think is an acceptable level at which to have risk that needs to be managed.? This time it’s a low cost 8200/8000 put ratio spread and as it is long at 8200 and short x2 at 8000 this means risk is at 7800, currently about 6% below the futures price. We pay 85.5 for the 8200 put and collect 40.5 x2 for the short 8000 puts. Our cost is thus 4.5 with risk 6% below the market, zero risk from 7801 upwards. Should the market go very South, we’ll look at adjustments. Let’s hope we get a delicious expiry in the meanwhile. APOLOGIES THIS IS A NOVEMBER TRADE AND VERY FAR FROM A LOSER!