That Was The Week Japan Derailed the Global Market Then Reversed The View

We experienced a vertigo inducing roller coaster as the Yen carry trade went belly up. I feel sure our erudite readers know what the Yen carry trade is: You borrow Yen for peanuts, convert to dollars, collect interest at 5%, change back, all good. However it’s great until it isn’t and the Japanese Yen dropped* from 160 to 144 to the dollar ie worth more.

*dropped means lowered in value not the ridiculous misuse of the word as in ‘Kylie just dropped her latest album’ Which doesn’t mean it was dropped or shelved, but released.

Aside from the rant about word abuse, other events happened during quite an eventful week. The empathic person feels for all those in the rioting, the options trader in me recalls the numerous uprisings and a history of such events, going back to the ‘Peasants’ Revolt’ of 1381. Thankfully our king is a little more measured and did not ride into the throng, sword aloft. You have to ask who the heck did Greggs and Shoezone upset? May calmer heads continue to prevail. Well done the anti-racist people.

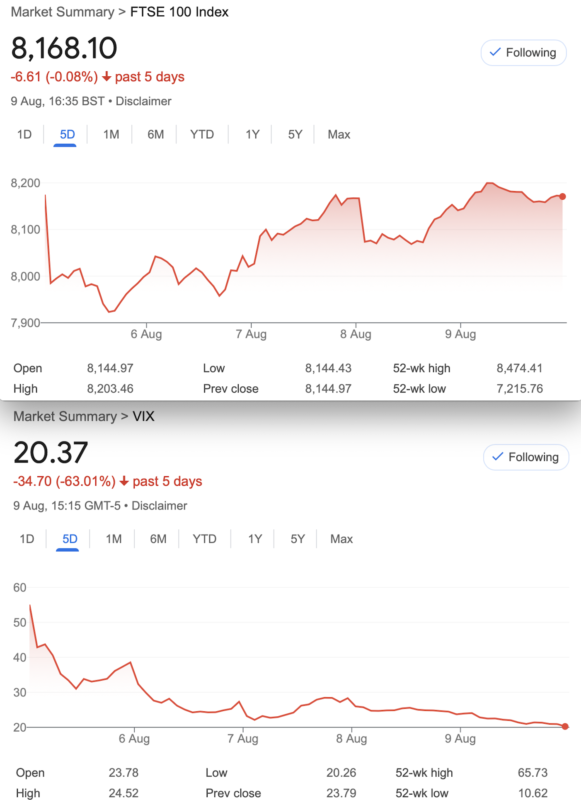

Don’t Panic in a Vix spike 55-OUCH!

My take on this as an options trader is primarily: Never be a forced buyer or seller. That is worth repeating to yourself. My trades as documented here may go through wild fluctuations, but we have a timeframe in mind. We would not be buying back short puts when volatility was at a high. We might adjust taking advantage of volatility skew. An example might be as follows:

02 Aug 8100 puts 76 7900 puts 29.5 Those strikes on Monday 05 Aug (after much of the mayhem was over) 8100 puts 165 7900 puts 79

As of this Friday 43.5 and 11. Let’s say you liked the idea of rolling down the 8100 puts on Monday, you sold 2x as many 7900 puts, and paid 165-(2×79)= 7. Your debit is now 29 not 43.5. If you’d sold the 8100 puts for big bucks, you’d be a happy bunny, if you’d bought them back in a panic, you’d be crying.

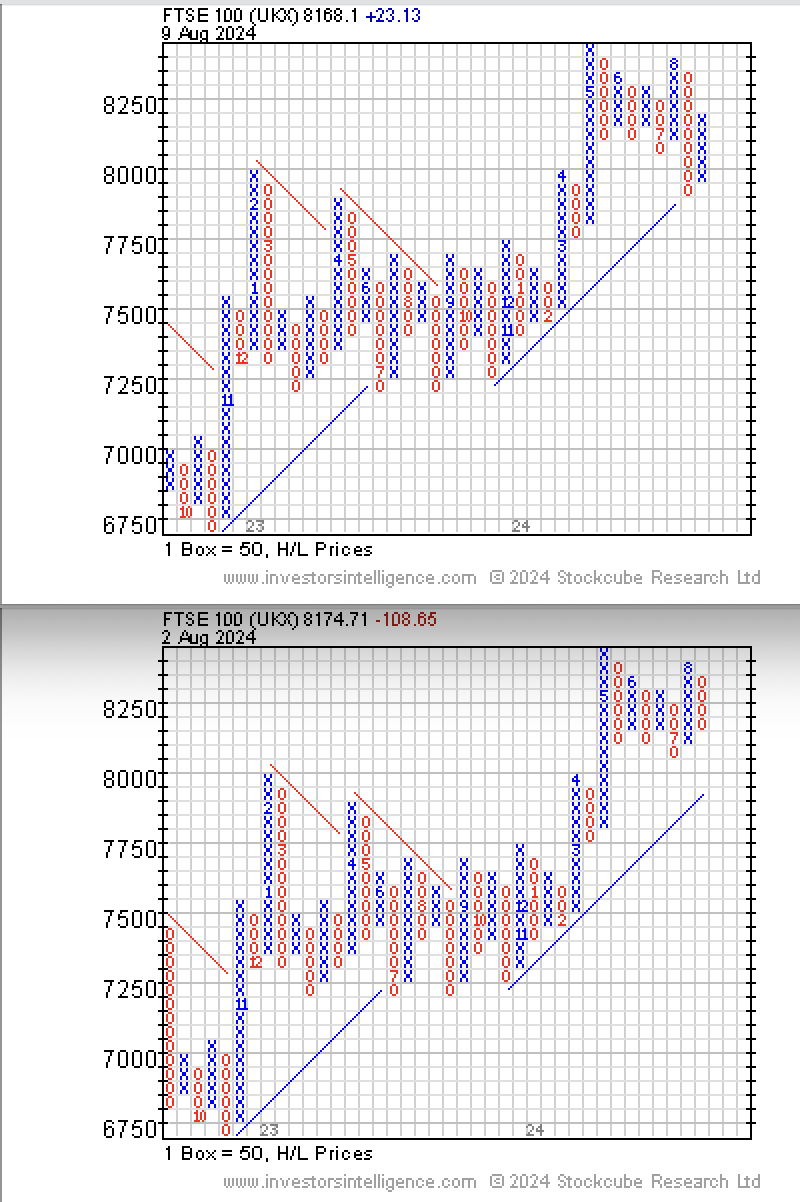

Point and figure

While there’s a lot of content this week with the trades, I thought it might be a good time to look at the P&F charts for last week and this week. They are particularly relevant for us as time is not a key feature, though here they denote 8 for August and so on. It says to me the market found support and reversed. Funny how FTSE is more or less the same as last week

Distraction Trades

ADA was $0. 3693 now $0.3474

XRP was $0.5680 .now $0.5885 The action was all in the main markets

DAX 4 wins 5 losers 1 break even 460 nett. so this is again a real performer but catching the entries is hard, exit is much harder.

UK Gilts were £17.09 now £16.97 It’s not an attractive instrument but hey, …………………. someday ! That day may be here sooner than we think

Legacy Trades 373, 374, 375, 376 and new trade 377

Trade 373 A Challenge Hotly Debated

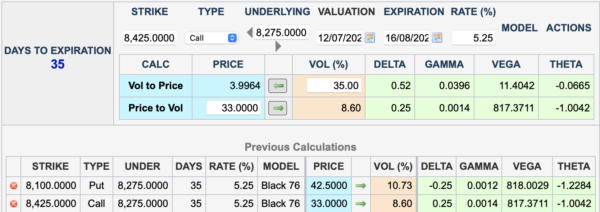

We are told that the risk profile for a covered call v short put is the same. Now this is usually based on stocks,(which can be assigned/exercised early) not an index but we thought it’d be interesting to check this out. So, we buy a future and sell a call and in isolation from this we sell a put Eagle eyed traders know that expiry for July looms next week, so we go with August options. The future, at best guess : 8275 at cash close on Friday. We choose similar deltas giving us:

So as you can see, the short call would give us a credit of 33. Buying a future carries margin costs. The Put 42.5. This may not be a fair test but it’s a demonstration and gives us short Put risk to the downside if the future drops below 8100-42.5= 8057.5. The covered call gives us a modest 33 credit, so downside risk 8242. Upside risk? You get called away at 8425, plus you have the 33 call credit. The short Put credits you with 42.5

We could sell twice as many calls or puts, and will monitor that idea too.*

Caveat:

We really do not like mixing a long/short underlying with options. All our winning trades have been based on pure options. Buckle up!

Last week:

So we ‘see’ the future at 8158 around 4.30 yesterday. So this gave us –80.5 for the short put A loss for the future of 117, while the call went to 14.5 Frankly this is horrible and every way you look at it this is not a nice trade even if you were to trade the collar, (Reversal) sell the call to buy a protective put. ( loss of 117, mitigated by an increase in the put of 38, while the short call lost 28 in our favour. Of course this is a demo it’s not a trade we’d take and probably the options should be ATM.

*Does not look like a plan!

Last week:

Future = 8288 (+13) call =29.5, the Put =38. This is truly awful! The future in 2 weeks has gone nowhere but on the way it has been down >200. A modest profit

Last week: Future = 8170 8425 call is 13.5 8100 put 76 It’s just horrible and tells us that futures are probably best traded intra day eg: Wednesday saw the future hit 8400

Typically our strategies rely on time decay, spreads and expiry so this is a departure and when we get to expiry the options advantage may be revealed. The future however could have been sold at 8400, and re-entry at 8155 on Friday.

This week:

Future 8170 8100 put 43.5 the 8425 call 2.5 Horrible – Making the case for NOT combining options with futures( Been there got that T shirt)

What is apparent is that for this to work it has to be dynamically traded. Our trades are essentially set and forget until the market makes the decision for us.

374 Summer Madness ? GUTS v Strangle – Sounds like a Horror film!

Following the success of our previous GUTS trade ( both sides are short options in-the-money) We fancy comparing the dynamics of the two strategies. Both take in premium, with the expectation that this will go to zero. So for the GUTS we sell the 8350 put and 7950 call but for the strangle we sell the 7950 put and sell the 8350 call. See what we did?

So for the strangle we take in 62.5 for the GUTS we take in 462, BUT!! We will of course have a 400 point liability at best, as we have sold deep ITM options. We can only make 62. Check out the Greeks and as you’d expect there’s a bit of nip and tuck but similar profiles for the two strategies. Personally I like working with deep ITM options, somehow it seems a little more comforting that the market has to chase you for such big money! Of course you still owe it. By the way the 400 is called ‘intrinsic‘ premium, while the juice on top is ‘extrinsic‘. A little addition to that vocabulary.

How did it do? Those prices: 7950 put 17 7950 call 327 8350 call 51.5 8350 put 140. So, the strangle 17 and 51.5 ( we took in 62.5) =6 loss

GUTS? 140 +327= 467. ( We took in 462) Small loss 5

Interesting that it seems scarier to trade the guts but the outcomes are ± the same.

Last week: 7950 put 37 7950 call 231 8350 call 23.5 8350 put 229 so, the strangle: 37+23.5= 60.5 -we took in 62.5

GUTS? 231+229= 460- we took in 462 It’s all gone a bit Pete Tong. However they are both equally not losers.

This Week: 7950 call 210 and put 15 8350 call 6 and put 210.5

GUTS? we took in 462 and now it’s 210+210.5, Win! Profit 41.5 Strangle? We took in 62.5 now it’s 6+15=21 Win! Profit 41 . Honestly, this may be a conspiracy( kidding) Yes, close out.

Trade 375 Is FTSE On The Up Escalator?

Let’s get fervently optimistic, and my bias be damned. We go with a call ratio spread and this is a low cost way of getting long with some risk. Our trade means buying nearer the money at 7300 and selling 2 calls further out of the money. We use August expiry: 8300 call 72.5, 8400 call 35.5

Where’s our risk? 8500 to the upside zero to the downside. What’s the cost? 72.5 minus 35.5×2. =1.5 Debit Bear in mind the volatility ‘smirk’ of calls ( vol decreases the further out of the money we go). However there is a small ‘premium’ here 10.14% vol for the 8300 and 10.18% for the 8400. This is unusual and may reflect unbridled enthusiasm. We would not expect to get a credit for this, however. This will go into a credit quickly as our 2 short options have almost twice the time decay. Oh no it didn’t! Volatility has gone from low to high

Last week 34 and 16 (x2) =2. However it has fluctuated from small loss to small gains during the week.

Now: 11.5 and 3×2 = 5.5. We paid 1.5 so nothing ventured etc. Hang in there? Close out for peanuts

Trade 376 Calendar Time?

Hopefully our readers understand the concept of the calendar spread: SELL the near month options buy further out in time. Typically we use the current and next month.

We return to the 3 x2. However while the strategy is to buy 3 near month(Aug)straddles and pay for it by selling 2 far month(Sept) straddles. Here’s the problem: THETA

We are going to be Devil’s avocado here and as the theta is so great in the August straddle we will sell 3 of them (187×3)=561 and buy 2 Sept straddles ( 316.5×2)= 633

Cost 72 and we reserve the right to disclaim this is any way decent trade, it just seems like a couple of quiet days will crush the volatility and theta is brutal on the August options.(LOL!) It will demonstrate the quirkiness of all the options properties. I was very concerned after Monday’s shocker!

Those prices: Aug 46.5 and 76 (x3) gives us 367.5 Sept: 146.5 and 142.5 (x2) gives us 578 Pure Luck? BIG WIN 210.5 -72= 138.5 Close out

Trade 377 New Month/ Near Month

This looks like a simple guilty pleasure- combining spreads, time and theta. It’s a modest trade as we don’t assume the market is back into risk on mode. So here’s the trade using last knockings of August selling the 8000 put for 20.5. We balance this with a protective 8100/8000 put spread in September. We buy the 8100 for 113 and sell the 8000 for 83, a cost of 30. So the maths professors will see we pay 30 but take in 20.5 for the August put we sold. Cost 9.5 max profit -the value of the spread 100- 9.5= 90.5

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.