That Was The Week NFPs Kicked The Market

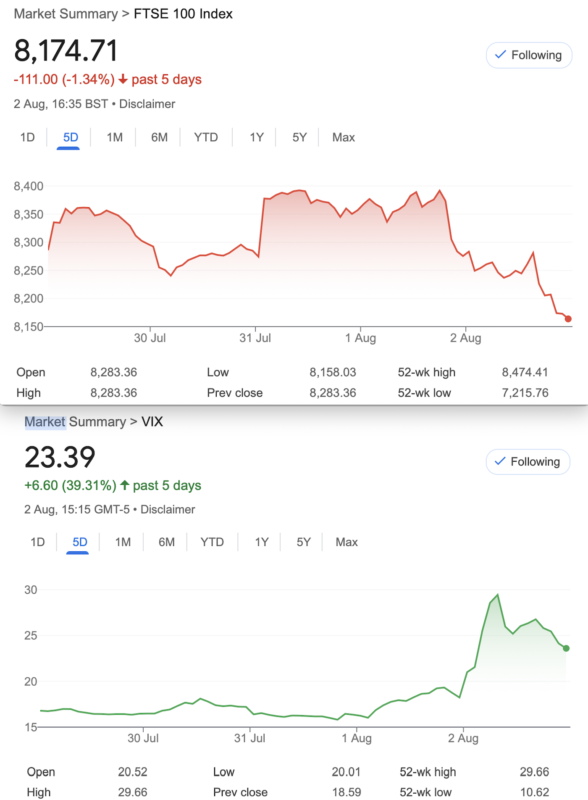

So why the heck happened this week? FTSE looked like it was off to the races again with a potential new high yet 8405 was the best it could muster. Phew! Vix has been climbing since 18th July, yet we still seem out of kilter with the US. The old lady of Threadneedle Street reduced the bank rate from 5.25- 5%. Bankers have kept interest rates stupid low since the great bankster recession of 2008. That greed driven rally and collapse was unforgivable, yet we expect little change in attitude from the banks. A month or more ago the FDIC https://www.fdic.gov reported 63 banks on the verge of collapse, casualties of the rate hikes since 2022. It’s only $517 billion nothing to see here. It’s a very mixed picture, but the world is far from untroubled.

Non farm payrolls -back in the game. Intel provided a double whammy sacking 15,000 people and the stock down 26%. That is indecent, how does anyone even trade that? Yours truly saw my own tiny share portfolio take a hit, but as oft repeated, an investment is a trade that went wrong! Sadly we can’t trade options in a pension* and we know in the long run shares do ok. I am concerned something else is afoot, and in the bigger picture we are seeing violent protests from the right wing even here in the UK. I will always support the right to protest but there is never an excuse for violence. Ironically the cost of these would probably have built a few hundred houses. Is this the new paradigm? Is ‘Stop the City’ going to roar back into fashion?

Investing for the Future.

I get a lot of ‘retirement stuff’ in my inbox, and this week was offered an annuity calculator. Not as exciting as a stairlift or motorised armchair! So, it is my understanding that an annuity is a bad idea. In my pension I have a mix of ETFs and active funds, like a money market fund that is supposed to yield 5.2%. We can pay into a pension up to age 75 currently and maybe(?) this will be extended to help late developers ( like me).

Now I can trade, pay tax on my earnings, but stick the money in the pension* and reclaim the interest. I have attended several ‘near death boring’ seminars about tax avoidance, trusts etc, none of them appealed.Pointy shoed sales people are not my thing. I am not offering trading advice but the reclaim of tax is the greatest gift we will ever get from the taxman. HMRC is not imbued with kindness.

My annuity quote was, as expected, something of a let down. I was led to understand that the drop in the bank rate would affect such products. They claimed rates were 40% worse a year ago. Yikes! Sure enough my PRU shares are looking ugly. Options traders like us should be capable of generating considerably more than the annuity rates, so let’s stick to what we know. Trust in our own ability to manage risk and generate profits. Beyond age 75? Do what you like! Prison is not an option. KIDDING!!!!

Distraction Trades

ADA was $0.4171 now $0. 3693

XRP was $0.6004 now $0.5680 . Ripple winning this race again, the gap is wider than it’s been for ages. It was up to $0.6500

DAX 4 wins 2 losers 1 break even 720 points/pips, this is bonkers, and may be cyclical, so as soon as I trade it in £££ it will go wrong.

UK Gilts were £16.68 now £17.09 It’s not an attractive instrument but hey, …………………. someday ! That day may be here sooner than we think

Legacy Trades 373, 374, 375 and new trade 376

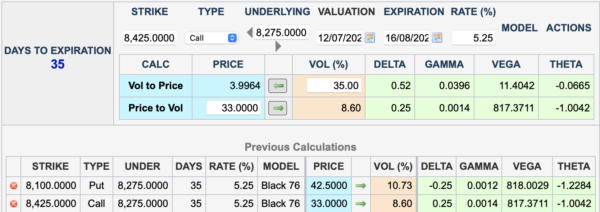

Trade 373 A Challenge Hotly Debated

We are told that the risk profile for a covered call v short put is the same. Now this is usually based on stocks,(which can be assigned/exercised early) not an index but we thought it’d be interesting to check this out. So, we buy a future and sell a call and in isolation from this we sell a put Eagle eyed traders know that expiry for July looms next week, so we go with August options. The future, at best guess : 8275 at cash close on Friday. We choose similar deltas giving us:

So as you can see, the short call would give us a credit of 33. Buying a future carries margin costs. The Put 42.5. This may not be a fair test but it’s a demonstration and gives us short Put risk to the downside if the future drops below 8100-42.5= 8057.5. The covered call gives us a modest 33 credit, so downside risk 8242. Upside risk? You get called away at 8425, plus you have the 33 call credit. The short Put credits you with 42.5

We could sell twice as many calls or puts, and will monitor that idea too.*

Caveat:

We really do not like mixing a long/short underlying with options. All our winning trades have been based on pure options. Buckle up!

Last week:

So we ‘see’ the future at 8158 around 4.30 yesterday. So this gave us –80.5 for the short put A loss for the future of 117, while the call went to 14.5 Frankly this is horrible and every way you look at it this is not a nice trade even if you were to trade the collar, (Reversal) sell the call to buy a protective put. ( loss of 117, mitigated by an increase in the put of 38, while the short call lost 28 in our favour. Of course this is a demo it’s not a trade we’d take and probably the options should be ATM.

*Does not look like a plan!

Last week:

Future = 8288 (+13) call =29.5, the Put =38. This is truly awful! The future in 2 weeks has gone nowhere but on the way it has been down >200. A modest profit

This week: Future = 8170 8425 call is 13.5 8100 put 76 It’s just horrible and tells us that futures are probably best traded intra day eg: Wednesday saw the future hit 8400

Typically our strategies rely on time decay, spreads and expiry so this is a departure and when we get to expiry the options advantage may be revealed. The future however could have been sold at 8400, and re-entry at 8155 on Friday.

374 Summer Madness ? GUTS v Strangle – Sounds like a Horror film!

Following the success of our previous GUTS trade ( both sides are short options in-the-money) We fancy comparing the dynamics of the two strategies. Both take in premium, with the expectation that this will go to zero. So for the GUTS we sell the 8350 put and 7950 call but for the strangle we sell the 7950 put and sell the 8350 call. See what we did?

So for the strangle we take in 62.5 for the GUTS we take in 462, BUT!! We will of course have a 400 point liability at best, as we have sold deep ITM options. We can only make 62. Check out the Greeks and as you’d expect there’s a bit of nip and tuck but similar profiles for the two strategies. Personally I like working with deep ITM options, somehow it seems a little more comforting that the market has to chase you for such big money! Of course you still owe it. By the way the 400 is called ‘intrinsic‘ premium, while the juice on top is ‘extrinsic‘. A little addition to that vocabulary.

How did it do? Those prices: 7950 put 17 7950 call 327 8350 call 51.5 8350 put 140. So, the strangle 17 and 51.5 ( we took in 62.5) =6 loss

GUTS? 140 +327= 467. ( We took in 462) Small loss 5

Interesting that it seems scarier to trade the guts but the outcomes are ± the same.

This week: 7950 put 37 7950 call 231 8350 call 23.5 8350 put 229 so, the strangle: 37+23.5= 60.5 -we took in 62.5

GUTS? 231+229= 460- we took in 462 It’s all gone a bit Pete Tong. However they are both equally not losers.

Trade 375 Is FTSE On The Up Escalator?

Let’s get fervently optimistic, and my bias be damned. We go with a call ratio spread and this is a low cost way of getting long with some risk. Our trade means buying nearer the money at 7300 and selling 2 calls further out of the money. We use August expiry: 8300 call 72.5, 8400 call 35.5

Where’s our risk? 8500 to the upside zero to the downside. What’s the cost? 72.5 minus 35.5×2. =1.5 Debit Bear in mind the volatility ‘smirk’ of calls ( vol decreases the further out of the money we go). However there is a small ‘premium’ here 10.14% vol for the 8300 and 10.18% for the 8400. This is unusual and may reflect unbridled enthusiasm. We would not expect to get a credit for this, however. This will go into a credit quickly as our 2 short options have almost twice the time decay. Oh no it didn’t! Volatility has gone from low to high

This week 34 and 16 (x2) =2. However it has fluctuated from small loss to small gains during the week.

Trade 376 Calendar Time?

Hopefully our readers understand the concept of the calendar spread: SELL the near month options buy further out in time. Typically we use the current and next month.

We return to the 3 x2. However while the strategy is to buy 3 near month(Aug)straddles and pay for it by selling 2 far month(Sept) straddles. Here’s the problem: THETA

We are going to be Devil’s avocado here and as the theta is so great in the August straddle we will sell 3 of them (187×3)=561 and buy 2 Sept straddles ( 316.5×2)= 633

Cost 72 and we reserve the right to disclaim this is any way decent trade, it just seems like a couple of quiet days will crush the volatility and theta is brutal on the August options. It will demonstrate the quirkiness of all the options properties.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.