America’s Train Crash -Traders Beware

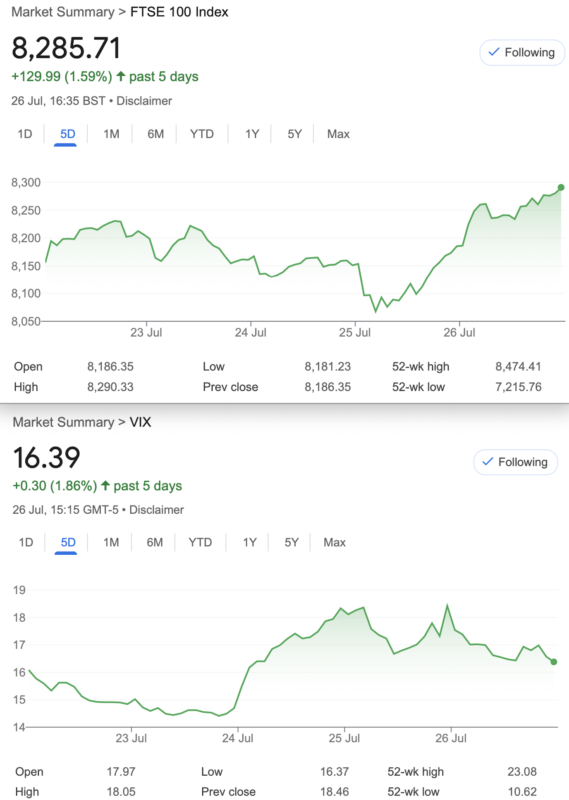

I am sickened and appalled by Trump as readers know. I’m optimistic that Kamala Harris can keep America on the right track. There is no rational debate for supporting Trump as the age argument against Biden is now Trump’s problem. Now, as previously mentioned the market wobble-meter of political upheaval barely moves. So is it different this time? We can put in place strategies at low cost for such events and take a view that with a very wide range we may well have a decent win. In other news FTSE went on the rampage with yet again the weirdest moves that may be designed to knock out day traders. Or………. somebody has AI algo quantum computing software that is a trader killer. There was much talk of a built in delay to stop algo shenanigans some time ago, but maybe it’s just my paranoia.

I did see some opportunities, being already in a web of delta neutrality, but cowardice got the better of my courage! Friday knocked that delta position bigly.

What Happened This Week?

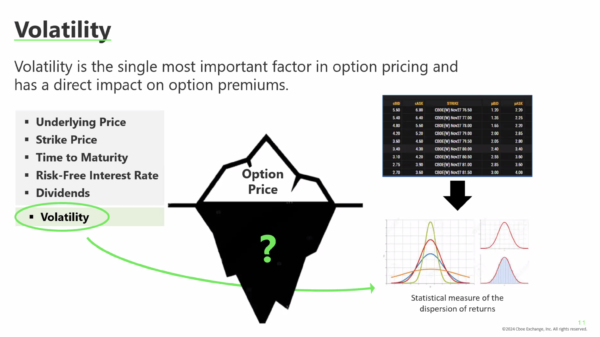

On a personal level a fascinating lecture ( Universities do occasionally allow the great unwashed to such things). The subject was the start and end of the Universe, so a quick chat really! Pertinent to trading is the scientific method, however. Doing the hard yards and testing based on reliable data, we can put together a variety of strategies which we can whittle down to the ones that ‘suit’ us. Again there was a CBOE webinar and again, it was really not very user friendly, in fact it was confusing for the new people.I have cherry picked the most useful graphic here:

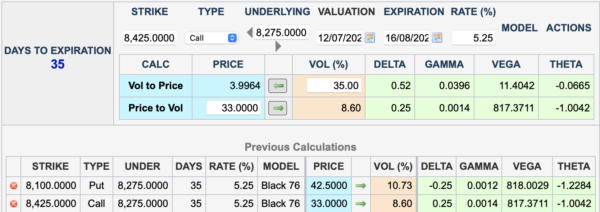

This is as profound as it gets but we cannot always choose the optimum entry based on volatility- ie selling high vol and buying when it’s low. High or low-it’s also subjective and needs to be taken in context. It’s worth a play with the calculator https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html

You can input the price of the option OR, its volatility. Once you have entered all the relevant info, try adjusting the vol, especially with 2 or more different strikes. You will notice the cost of a spread will vary a lot in %age terms, factor in bid/offer, aim to get the best value. Some people like to ‘leg in’ buying/ selling one part, then legging in to the other. You need sharp skills and over time you may find it evens out.

You can see how different trade strategies work here, every week, for free. There’s also our track record and 374 old trades.

Distraction Trades

ADA was $0.4331 now $0.41§71

XRP was $0.5942 now $0.6004 Ripple winning this race again, the gap is wider than it’s been for ages.

DAX 4 wins 1 no entry +480 pips Again letting loose. We have shifted from the dogma of trading at a specific time, but the problem is, running those winners. Exits are harder than entries

UK Gilts were £16.67 now £16.68 It’s not an attractive instrument but hey, …………………. someday !

Legacy Trades 373, 374, nd new Kid 375

Trade 373 A Challenge Hotly Debated

We are told that the risk profile for a covered call v short put is the same. Now this is usually based on stocks,(which can be assigned/exercised early) not an index but we thought it’d be interesting to check this out. So, we buy a future and sell a call and in isolation from this we sell a put Eagle eyed traders know that expiry for July looms next week, so we go with August options. The future, at best guess : 8275 at cash close on Friday. We choose similar deltas giving us:

So as you can see, the short call would give us a credit of 33. Buying a future carries margin costs. The Put 42.5. This may not be a fair test but it’s a demonstration and gives us short Put risk to the downside if the future drops below 8100-42.5= 8057.5. The covered call gives us a modest 33 credit, so downside risk 8242. Upside risk? You get called away at 8425, plus you have the 33 call credit. The short Put credits you with 42.5

We could sell twice as many calls or puts, and will monitor that idea too.*

Caveat:

We really do not like mixing a long/short underlying with options. All our winning trades have been based on pure options. Buckle up!

Last week:

So we ‘see’ the future at 8158 around 4.30 yesterday. So this gave us –80.5 for the short put A loss for the future of 117, while the call went to 14.5 Frankly this is horrible and every way you look at it this is not a nice trade even if you were to trade the collar, (Reversal) sell the call to buy a protective put. ( loss of 117, mitigated by an increase in the put of 38, while the short call lost 28 in our favour. Of course this is a demo it’s not a trade we’d take and probably the options should be ATM.

*Does not look like a plan!

This week:

Future = 8288 (+13) call =29.5, the Put =38. This is truly awful! The future in 2 weeks has gone nowhere but on the way it has been down >200. A modest profit

374 Summer Madness ? GUTS v Strangle – Sounds like a Horror film!

Following the success of our previous GUTS trade ( both sides are short options in-the-money) We fancy comparing the dynamics of the two strategies. Both take in premium, with the expectation that this will go to zero. So for the GUTS we sell the 8350 put and 7950 call but for the strangle we sell the 7950 put and sell the 8350 call. See what we did?

So for the strangle we take in 62.5 for the GUTS we take in 462, BUT!! We will of course have a 400 point liability at best, as we have sold deep ITM options. We can only make 62. Check out the Greeks and as you’d expect there’s a bit of nip and tuck but similar profiles for the two strategies. Personally I like working with deep ITM options, somehow it seems a little more comforting that the market has to chase you for such big money! Of course you still owe it. By the way the 400 is called ‘intrinsic‘ premium, while the juice on top is ‘extrinsic‘. A little addition to that vocabulary.

How did it do? Those prices: 7950 put 17 7950 call 327 8350 call 51.5 8350 put 140. So, the strangle 17 and 51.5 ( we took in 62.5) =6 loss

GUTS? 140 +327= 467. ( We took in 462) Small loss 5

Interesting that it seems scarier to trade the guts but the outcomes are ± the same.

Trade 375 Is FTSE On The Up Escalator?

Let’s get fervently optimistic, and my bias be damned. We go with a call ratio spread and this is a low cost way of getting long with some risk. Our trade means buying nearer the money at 7300 and selling 2 calls further out of the money. We use August expiry: 8300 call 72.5, 8400 call 35.5

Where’s our risk? 8500 to the upside zero to the downside. What’s the cost? 72.5 minus 35.5×2. =1.5 Debit Bear in mind the volatility ‘smirk’ of calls ( vol decreases the further out of the money we go). However there is a small ‘premium’ here 10.14% vol for the 8300 and 10.18% for the 8400. This is unusual and may reflect unbridled enthusiasm. We would not expect to get a credit for this, however. This will go into a credit quickly as our 2 short options have almost twice the time decay.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.