That Was The Week a New Parliament Has Much To Do

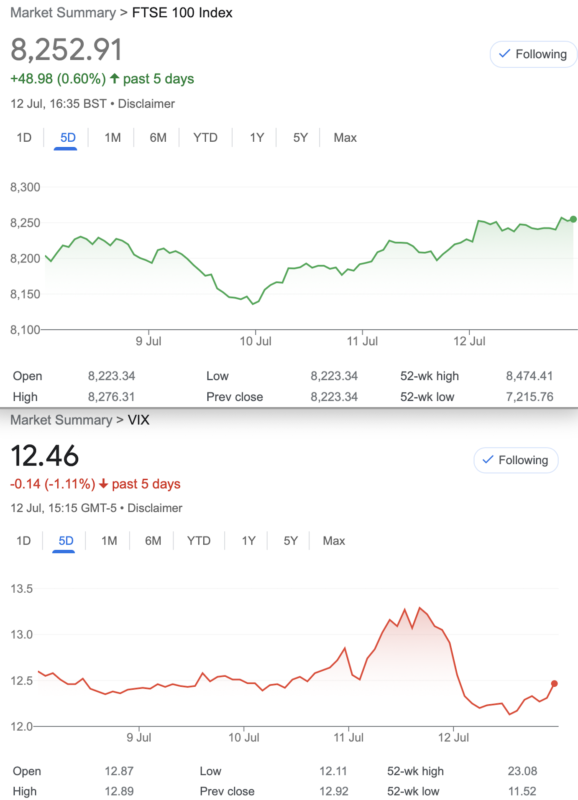

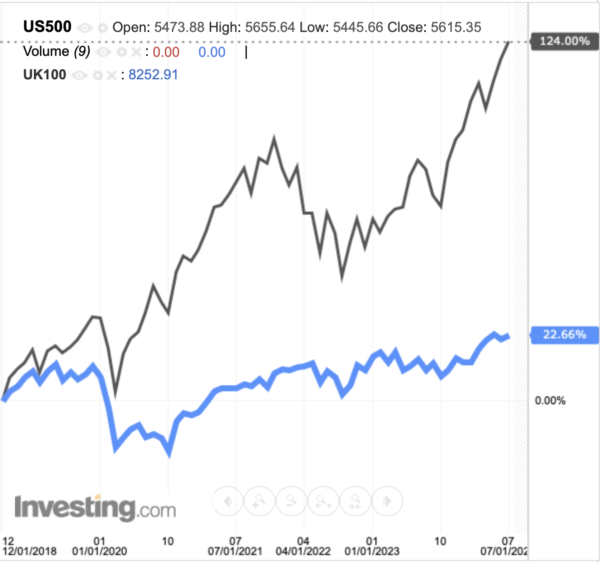

In a week when the saga of the debacles of Post Office, and water companies continued to blight us, our football team scraped by with another lucky win. (Caveat I’m no expert on football). FTSE shows no sign of disapproval of the Labour government, and the £sterling has rallied. Inflation has cooled somewhat but it’s hard to call a September rate cut. The S&P 500 marched upwards about 12% since mid May. So while we don’t like to call the market direction, there appear to be few headwinds. However it’s clear that America’s 7 stock stars make the difference as FTSE ploughs its lonely furrow:

It’s easy to criticise the ETF culture and index tracking but frankly we all want to see decent growth in our pensions and the FTSE is not favoured by UK pension funds https://corporate-adviser.com/pension-fund-investment-into-uk-shares-falls-to-new-low/

So, unless regulations change, our FTSE is likely to plod on without the might of the pensions industry in tow. This does not affect us because we trade options and trade according to risk and reward profiles, direction is largely immaterial. It does affect your pensions, but misguided loyalty to our markets carries a hefty price tag. I’m told we all need some bonds and gilts though.

NB: Seems FTSE is out of favour with everyone with record outflows in May as FTSE marched steadfastly upwards to another all time high 8474 – makes no sense to me either!

Education x3 -Anyone Remember Mr Blair’s Promise?

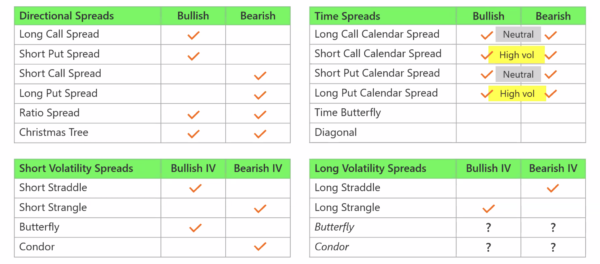

I allude to options education( rather than old New Labour’s plans) and a thoroughly disappointing and oddly dysfunctional CBOE webinar this week: 10th July:

[Spread strategies can be an effective approach to limiting risk and creating specific outcomes for portfolio managers and retail traders alike. In this session, Rich Excell will discuss the mechanics of spread strategies, and demonstrate why they are so powerful when seeking to manage risk.

Part 2 of 4: The Summer Series]

The Zoom meet was not an epic in terms of attendance and started with a bizarre question and an incorrect answer. We were then rattled through a number of rather unclear explanations about spreads and some risk graphs which of course show risk at expiry and are of limited use. This is why we feel that what we offer is learning BY DOING. By showing weekly updates of real weekly trades based on real prices it is hoped that options can be better understood. You could learn to drive from a computer based course, but there’s no substitute for the real thing. Curiously, yours truly had a flashback as they ran through the risk warnings:’ Options are not suitable for everyone’. My first tenuous forays were a real mental challenge. That is normal and we believe in our approach, in the hope that more people take up the fantastic prospect.

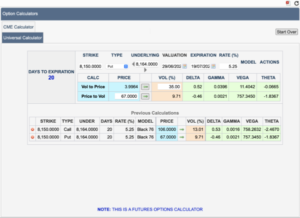

Here’s a moderately helpful CBOE screenshot:

Distraction Trades

ADA was $0.3563 now $0.4197

XRP was $0.4337 now $0.5111

DAX 3 losers 3 wins 1 break even losses 90, wins 330! We have shifted from the dogma of trading at a specific time, but of course the problem is, running those winners.

UK Gilts were £16.70 now £16.67 It’s not an attractive instrument but hey, …………… …….. some day !

Legacy Trades and 372 New Labour, Same As The Other Party?

Trade369 July Expiry

So, while we are utterly bereft of clues about the market should we try another strangle? Not the trade of choice but it’s hard to see what might work well and July expiry is only 34 days hence. Thus we go with the same strikes as Trade 368. Therefore we are saying we think/believe FTSE will find support higher than 7900 and resistance below 8500. We collect 39.5 for the put and 19.5 for the call We therefore collect 59 and sit on our hands for 33 and a bit days. Apologies if it’s a bit beige but we’ll try something a bit feisty next time.

With not a lot going on with volatility we now have prices: 15 and 20.5=35.5 we collected 59 a great outcome as theta took chunks out of premiums. Yes you could do this whilst lying shipwrecked and comatose drinking fresh mango juice. (Nod to Howard Goodall)

Last week: 14.5 for the 7900 put and 6.5 for the 8500 call Yowser! A very nice return as we sold for 59

Last week: 5 for the Put and 3 for the Call Even better-59-8= 51. Honestly, close out go sit on the beach WIN!

Now: Put is now 1 and the call 2.5 – No, I would not hold on for pennies, as shown with last week’s comment

Trade 370 Ladder Not Laddish

Let’s kick the beige into touch and sell a ton of premium and see where it leads us. We use July expiries: buy: 8500 put, 248 sell 2x 8300 puts 110.5×2= 221, buy 8150 put, 53.5, sell 2x 8000 puts 24.5×2= 49

Thus we have a cost of 248+53.5. – (221+49)= 31.5 Logic of the trade? We buy a juicy in the money put spread, we have no upside risk other than the cost 31.5 Downside is a tad skewed giving us a lot of wiggle room just below 8000

Last week: 316.5, 148.5×2, 67, 26.5×2 . We have 316.5+67= 383.5 long premium. Short premium: 148.5×2= 297, 26.5×2=53=350. We are in credit to the tune of 33.5(we paid 31.5)

Gives us: 280, 106.5(x2), 33.5 and 9.5(x2) 280+33.5= 313.5 minus 213+ 19= 232. We paid 31.5 thus 313.5 – 253.5= 60 (200% profit)

A real gift from a simple strategy, buying deep in the money WIN! OK- we run it ……for fun!

Again for fun…. those prices: 239, 63(x2), 8.5, 1.5(x2) =118.5 -31.5 gives a profit of 87 -ok almost 50% more profit

Trade371 A Trade for Election Week ( The US has some kind of holiday on 4th July)

This is disturbing, while not exactly at the money this straddle has call Vol at 13.01% and the put at 9.71% So what’s the take away? Nobody wants to buy puts? Everyone wants to pay too much for calls? It’s a very cheap straddle with an overpriced call. We choose a Tasty Trade Liz and Jennie ‘Big Lizard’. Sell the straddle buy an out of the money call. We buy the 8250 call for 55. Gives us 173-55=118.

Logic of the trade? However, we cannot lose to the upside, and downside is protected down to 8150-118= 8032 We like it!

How did we do? The 8150 straddle is now 105.5+33.5 our long call is 47.5, So: 139-47.5=91.5. We collected 118 in premium sold giving us a profit of 26.5 – I’d close out but we run it. So, why close out? We have max sensitivity at 8150 and a new government, just a thought…..

So from last week we now have the short 8150 straddle 121.5+8.5 the long 8250 call 48 gives us 130-48=82. We took in 118 so, 36 profit (We opted to close out last week, but always run for fun)

Trade 372 Cause for Optimism?

We’ll go very mildly optimistic with a call ratio spread, it ‘s simple carries some risk( ∞ ) yes theoretically the risk is infinite, and FTSE could go to 20,000 if the £ sterling dropped to $0.001. The strikes we chose are long 8200, short x2 at 8300, this then gives us risk at 8400 -figured out why? The prices 73,29×2 = 15 debit. And logic of the trade- we may see moderate rise, or we may see a lack of confidence in a yet untested chancellor, to the downside we can only lose max 15, to the upside we could make 100, the value of the spread, so effectively 85 nett. It’s a tad spicy and not altogether a peachy trade but we can adjust/close out any time.

This week 8200 call is 80.5 the two 8300 calls are 26.5. =27.5 (we paid 15) Small profit again we will run this.

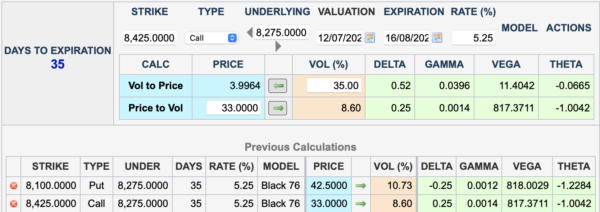

Trade 373 A Challenge Hotly Debated

We are told that the risk profile for a covered call v short put is the same. Now this is usually based on stocks,(which can be assigned/exercised early) not an index but we thought it’d be interesting to check this out. So, we buy a future and sell a call and in isolation from this we sell a put Eagle eyed traders know that expiry for July looms next week, so we go with August options. The future, at best guess : 8275 at cash close on Friday. We choose similar deltas giving us:

So as you can see, the short call would give us a credit of 33. Buying a future carries margin costs. The Put 42.5. This may not be a fair test but it’s a demonstration and gives us short Put risk to the downside if the future drops below 8100-42.5= 8057.5. The covered call gives us a modest 33 credit, so downside risk 8242. Upside risk? You get called away at 8425, plus you have the 33 call credit. The short Put credits you with 42.5

We could sell twice as many calls or puts, and will monitor that idea too.

Caveat: we really do not like mixing a long/short underlying with options. All our winning trades have been based on pure options. Buckle up!

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.