That Was The Week, Can You Say ‘Resistance’?

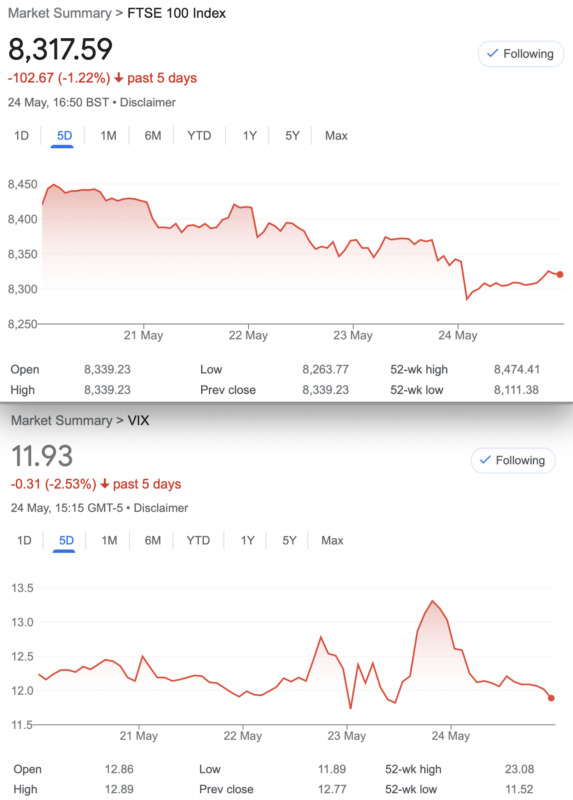

So, Rishi Rich is throwing in the towel, it seems. Or, perhaps a towel was precisely what he needed after a highly bizarre drenching public address outside Number 10. However, this was not an act of defiance, it seems. This was a bit desperate, and a fair few of the old guard will no longer be part of Rishi’s A team. So, how does this affect us, and our instrument of choice, the FTSE100?

Our friends at IG had this: https://www.ig.com/uk/trading-strategies/how-do-uk-general-elections-impactthestock-market–190926

Curiously America’s stock market seems to have the same reactions- muted. However our index is comprised of mostly global companies, and the oil price is more of a market mover than politics, though Liz Truss gave us a nice drop. Thus, we need to keep a bit of a weather eye on the political scene though ultimately it’s business as usual. However the £ may have a bit of a wobble as Labour are not seen as market friendly. Although, allegedly Tony Blair’s first move was to ask the City what they wanted, back in the last century. The US trundles on with the lunacy of the Trump circus, and the horrific survey that showed far more people trusted Mr Trump with the economy, despite the actuality. Biden has done very well in troubled times, and despite the protestations, their economy is doing great.

Trading Stuff

So, having done some adjustment to reduce my own short exposure, the FTSE starts to drop lower. We cannot know the future but we cannot tolerate runaway losses so moderating risk is something we can do by various means. Compare and contrast with stocks or futures, there is nothing like the flexibility, and stocks can get ugly for years, although futures can be bought and sold in multiples of £10 a point. However, in fairness, with spread betting you have the flexibility of trading for pennies a point. This brings us to approaches to trading: Proactive, and/or reactive.

We are proactive when we take positions, typically monthly and basing our positions on what went before is the best we can do. We’re taking a view of the level of risk and the range of market swings we can ‘cope with’. Thus, flipping the perspective to reactive is usually where we are once trades are on, looking a bit ugly and can be uncomfortable. However it is not the same as waking up 5 days a week and knowing that you must place trades afresh, placing stops from here to Sunday. We often run trades for 5– 45 days or so. We may even look ahead 120 days and structure complex trades that give us a huge range. You could make good profits trading once a year.

Why Options?

So, once again, options make us proactive AND reactive, though adjustment may only occur 2-3 times each year. Because the characteristics of options can reward us without doing very much it maybe makes us uncomfortable with investing in ‘sure thing’ stocks. Note to self: Remember Invensys? Bought on a Tuesday on FT recommendation, on Wednesday it was ‘troubled engineering group’ Invensys. (Other stocks may be available, and no shame on the aforementioned). How do other people cope with that? Sit tight and cry? Close out?

Here’s a reminder of strategies you may not see here, but it’s good to know them: https://www.investopedia.com/trading/options-strategies/

Distraction Trades

ADA was $0.4839 now $0.4640

XRP was $0.5241 now $0.5384 A bit of riffling in the wind.

DAX 2 losers -30×2, one win +30, 2 no entries – Just goes to show how hard it is to trade intra daybed the simple strategy has not been a consistent win or loser, just a slow grind of tedium.

UK Gilts were £16.66 now £16.49 NB this is the VAN ETF with a yield of 4.65%

Legacy Trades 363- 365 and new kid 366

Trade363 Can we Find something not totally rubbish?

It’s unseasonal but it’s a pitchfork!

Ok so here’s the trade, and everything is wrong about this which might serve us well. We sell one call and 3 puts at the strike which is the value of the ATM straddle subtracted from the ATM (Futures) price, 8256. This gives us nothing much in the call but the put is all extrinsic value, ie if the put options expired today, they’d have no value.

We take in the premiums 271.5+ 50.5×3= 423. The dream is….. the market at 7700- 8300 for June expiry, ideally at exactly 8000!

Last week: 466.5 and 18.5 x3 – not unexpected and those puts seem to be heading towards zero. Loss 0f 43 + those puts

Last week: Still a loss, but we soldier on, now it’s 489, from our original credit 423

This week: 348+16×3 = 396. PROFIT!

Trade 364 Back to The Knitting

So, it’s too late to use the May expiry, but June is well within the parameters (<45 days to expiry) and we again choose a ratio spread, which is a firm favourite here. However there’s a twist and a fellow trader has done a lot of homework and come up with the following. Subtract the value of the ATM straddle (8450 for our purposes) gives us ± 8200, and that is where we write the short puts. And for the longs we go 100 points above, giving us 8300/8200 put ratio. Those premiums? 41×2= 82, and 62.5. Earth shattering credit it is not, but it may be in the ballpark for the long spread to produce the goods- a max 100. Risk below 8100. We must endure such horribly, absurdly low prices for now.

Last week 48 and 29×2 gives us debit 10. Our original credit was 19.5

This week: 75 and 43 x2= 11, our credit was 19.5 So happy days again, will June play nicely?

Trade 365

Calendar time anyone? You know- sell the near month, buy the far month. We’ll do a simple comparison, between the 1 for 1 and the ratio spread, whereby we have a long spread in the far month.

Here we go: We sell the Jun 8250 put, we buy the 8350/8250 put spread in July. We have theta in our favour with a calendar, we have risk if FTSE drops below 8150, zero risk to the upside

Sorry if it ‘s a rinse and repeat a lot like 364, but as we’ll see the dynamics are different.. Oh, and the prices? Jun 8250 put 37, the July 8350/8250 put spread 88.5-61.5= 27 giving us a small credit of 10. The straight 1 for 1 calendar would cost us 88.5-37= 51.5 CORRECTION!!!!! sell: 8350 jun put 62.5, buy: July 8350 put 88.5= 26

This week we have the debit in June: 57 and credit 38.5 for the July spread 18.5- 10 credit, gives us a loss 8.5

The straight one for one calendar is 127.5 – 97.5 = 30 a small gain from last week as we paid 26

Trade 366 This Takes some Cojones- it’s called a GUTS.

Here’s some fun and the GUTS trade is created as a deep ITM (in-the-money) strangle. We sell the 8000 call and the 8500 put. Think about those strikes and all points in between. At expiry they can only add up to 500. Here’s the kicker we sell those 2 options for…..542.5 So assuming FTSE does not exceed the 2 strikes at 8500 and 8000, we make 42.5* Mind boggling isn’t it!

*It’s known as extrinsic premium (where the 500 is intrinsic).

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.