That Was The Week, Calmer Heads Prevailing?

The old man of the US, the Dow Jones hit 40,000 which is a milestone but the far more widely watched S&P500 is the biggie. So, while 5,300 is not a number to set the world alight, it’s another ATH for the S&P. However, we expect the inflation number at some point again to put a match under the rocket fuel yet again. Thus being short is not the position one might desire. Mea Culpa.

In other news Kelloggs is closing its Manchester factory and as the highest ever prices bite, people are going with generic brands. And this has not been lost on the supermarkets whose own brands gained favour and market, as the 200% mark up for premium brands no longer makes sense. So, while most of retail is struggling, the supermarkets might be enjoying a revival. DYOR.

Wither the markets? Perhaps the question should be ‘what will derail this melt up?’. So, while recession is always in the distance central banks have a lot of wiggle room, despite the BofE coming in for some rightful criticism. This is troubling: https://markets.ft.com/data/indices/tearsheet/summary?s=UKX.P:FSI

So, the chart shows the P/E of FTSE relative to the S&P has shot up by about 30%. I have mentioned before that we do not welcome or merit US type valuations with triple digit P/E ratios in some cases. To quote Jim Slater the once demonised trader ‘Elephants do not gallop’. FTSE is an obese senile elephant, if we’re making an analogy of elephantine proportions.

Options Expiry and A.I.

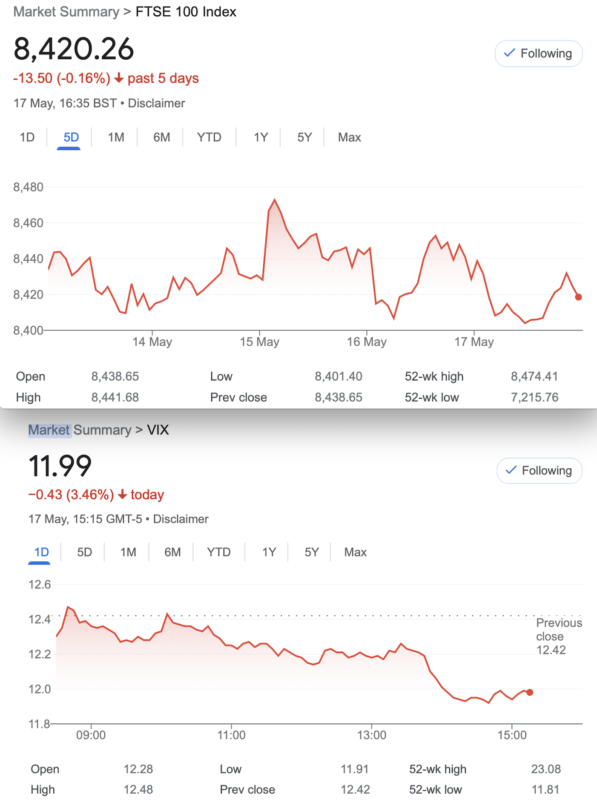

So, as always we hope everyone was safe at the expiry, happening every 3rd Friday of the month. However, this was not a conspicuous triple witch, just the index which expired at 8425 or so, as the week threatened to take my head off! One of my distractions is using generative AI and Google’s Gemini has proved itself a useful resource. Gemini confirmed that all the actions I was taking with my short positions was correct. Gemini also resolved a historical term that I learned 25 years ago, related to Knights of St. John. Another diversion, and as intriguing as UFO ‘research’

Again, in my treasure trove of emails, another position calculator was proffered, but here’s my problem. Plugging in historical trades currently running makes no sense, as you would not choose these trades. Secondly the myriad of possibilities cannot possibly be covered, though ‘ball park’ in my head I’m very well protected to the downside. Simply put, if you are short, say a July 7400 call and the FTSE at July expiry is 7500, you owe 100. Now, factor in some short puts, some ratio spreads, butterflies in various expiry months and every possibility that adjustments will be dynamic, we cannot know the future. I have tried! So if anyone has a programme that can make sense of multiple options positions for the next 4 months, I’d be really interested. Sometimes, in our options world we are isolated, but we’re not team players, trading is not a team sport.

Distraction Trades

ADA was $0.4439 now $0.4839

XRP was $0.5032, now $0.5241 Both had a little blip up, but crypto may not be bulletproof it now transpires. https://arstechnica.com/tech-policy/2024/05/sophisticated-25m-ethereum-heist-took-about-12-seconds-doj-says/

DAX 2 losers, -30×2, 2 no entries, one win +180

UK Gilts were £16.66 now………… £16.66 Ugh! Apparently the Bank of England bought these at a high and are busy selling them at a loss. They hope to turn professional next year.

Legacy Trades 363, 364 and now 365

Trade363 Can we Find something not totally rubbish?

It’s unseasonal but it’s a pitchfork!

Ok so here’s the trade, and everything is wrong about this which might serve us well. We sell one call and 3 puts at the strike which is the value of the ATM straddle subtracted from the ATM (Futures) price, 8256. This gives us nothing much in the call but the put is all extrinsic value, ie if the put options expired today, they’d have no value.

We take in the premiums 271.5+ 50.5×3= 423. The dream is….. the market at 7700- 8300 for June expiry, ideally at exactly 8000!

Last week: 466.5 and 18.5 x3 – not unexpected and those puts seem to be heading towards zero. Loss 0f 43 + those puts

This week: Still a loss, but we soldier on, now it’s 489, from our original credit 423

Trade 364 Back to The Knitting

So, it’s too late to use the May expiry, but June is well within the parameters (<45 days to expiry) and we again choose a ratio spread, which is a firm favourite here. However there’s a twist and a fellow trader has done a lot of homework and come up with the following. Subtract the value of the ATM straddle (8450 for our purposes) gives us ± 8200, and that is where we write the short puts. And for the longs we go 100 points above, giving us 8300/8200 put ratio. Those premiums? 41×2= 82, and 62.5. Earth shattering credit it is not, but it may be in the ballpark for the long spread to produce the goods- a max 100. Risk below 8100. We must endure such horribly, absurdly low prices for now.

This week 48 and 29×2 gives us debit 10. Our original credit was 19.5

Trade 365

Calendar time anyone? You know- sell the near month, buy the far month. We’ll do a simple comparison, between the 1 for 1 and the ratio spread, whereby we have a long spread in the far month.

Here we go: We sell the Jun 8250 put, we buy the 8350/8250 put spread in July. We have theta in our favour with a calendar, we have risk if FTSE drops below 8150, zero risk to the upside

Sorry if it ‘s a rinse and repeat a lot like 364, but as we’ll see the dynamics are different.. Oh, and the prices? Jun 8250 put 37, the July 8350/8250 put spread 88.5-61.5= 27 giving us a small credit of 10. The straight 1 for 1 calendar would cost us 88.5-37= 51.5

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.