That Was The Week Shoppers Proved Resilient Again, US Market High

Supermarkets reported strong sales, the Post Office scandal maintains its justifiable high profile, and the world gets more dangerous. So no surprises, people find money for Xmas, despite all the reports of food bank crises and deprivation. Hard to know the real position but the distribution of wealth is still more skewed to the wealthy.

Perhaps the wider question in the Post Office scandal is how’ inept’ the legal system is, how easy it was to defraud so many good people. And how the appalling behaviour of a few was simply glossed over, to benefit a few. Anyone remember the sub-prime scandal? We were shocked that punishments were non-existent for dodgy bankers, as people lost their lives, their homes and jobs. Rinse and repeat.(?) This time around let’s hope punishments are harsh, we should be better than this. The victims are simply, good people .

Moral outrage aside, and regarding global conflicts, we’re not sufficiently informed to comment, but there seems little hope. We should be better than this too.

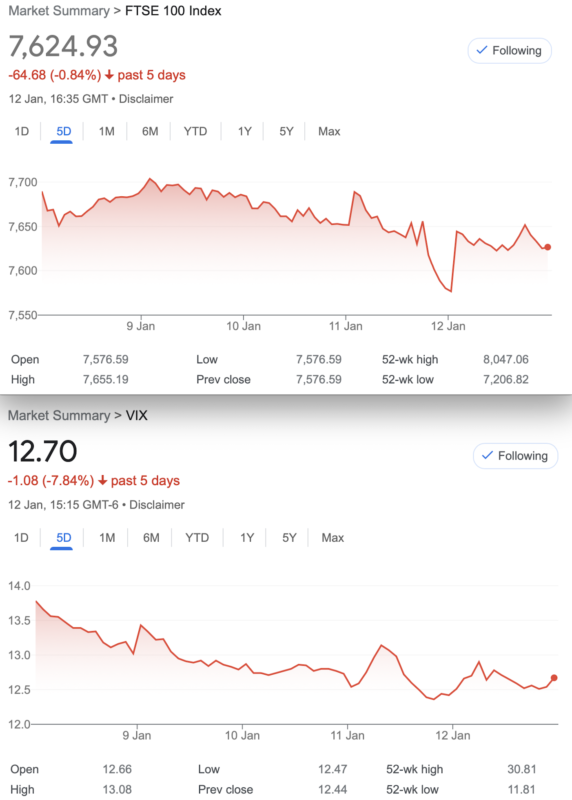

So what’s going on in the markets? VIX shrinks, SPX rises, here’s some sage commentary and charts: https://www.optionstrategist.com/blog/2024/01/weekly-stock-market-commentary-1122024 It’s curious that options activity is bearish against a backdrop of increasing bullishness. Caveat: FTSE is only distantly connected to the coat tails of the SPX these days. And while it’s cheap, the risk free yield is a better prospect. Savings rates may soon drop, but at least cash is ‘safe’. Given the almost opposing views, we’ll find out soon enough how this pans out. We often say that we don’t need to be directional, as options give us, well, options. Finding trades in this environment has been far more challenging, and has been since September. Sentiment drives markets as much as fundamentals. We feel it’s all a bit rosy.

ETF Menace!

This week the SEC decided to agree to a Bitcoin ETF,`actually eleven! Good luck to those punters. And yours truly discovered a covered call ETF – oh wait there’s 263 of them. What happens when everyone wants to sell the same thing? Answers on a postcard to ‘herd mentality and law of diminishing returns’. c/o New York Stock Exchange USA.

We all need investments but sometimes the returns on options trading make it hard, almost farcical, to accept a paltry return of 2-3% from ‘professional managers’. We know we can do so much better. Covered calls have a poor track record, in our estimation. The expense, the limited returns can pan out given the right stock. Yes you could write calls on an index and buy the future, but we have found this to be a ‘clunky’ trade at best. Monitoring these can also be a little gut wrenching. We could test this out- watch this space!

Distraction Trades

ADA was $0.5186 now $0.5505

XRP was $0.56546 now $0.57530 – it’s a curious relationship as ADA and XRP have over time changed places in value.

DAX Miserable week 4 no entries one break even (+30) You could argue the system kept us out of losing trades.

UK Gilts were £17.08 now £17.09 A nothing week

Legacy trades -And 349, Second Trade of 2024

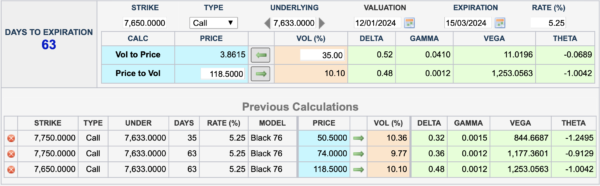

Trade 346 In the Dire Volatility What Can We Do?

We often overlook calls as puts are the go to trade when Vol is in our favour, but now we are faced with the sole weapon in our armoury-theta. So, it’s a calendar trade whereby we sell near month and buy far month. Here we sell the Jan 7800 call for 29.5 but here’s a twist, we will do a level 7800 call in Feb, and also see how we perform with a 7700/7800 long call spread in Feb.

Those prices: Feb 7700 call 92.5, and Feb 7800 call is 57.5. So the spread costs 35, we sell the Jan 7700 call for 29.5 so our trade costs 5.5. (Risk around 7900)

The standard calendar trade- sell Jan buy Feb costs 57.5-29.5= 28

It’s complicated!

So? Jan 7800 call 52.5, the Feb 7800call 103 =50.5 the trade cost us 28 so a small win.

Previous week, the other choice was to buy the Feb7700call 156.5 and sell the 7800call, now 103, gives us 53.5 against the sold Jan 7800 call at 52.5 gives us 1! We paid 5.5.

Last week, Jan 7800 call now 53,5 Feb 7700 call 163, Feb 7800call 105 the level calendar is now 51.5 cost 33.5, so profit 18. The spread credit -5.5.

CORRECTION: Error in initial prices, so the level calendar was 33.5 debit, the jan short/long Feb spread was Debit 10

[ trade 346 initial prices 7800 Jan call 26 7800 Feb 7800call 59.5 Feb7700call 95.5]

Of course being calendar trades we run them

Now: Jan 7800 call 20.5 Feb: 7700call 118, the 7800 call 69.5.

Last week: Standard calendar 69.5-20.5= 49, minus our debit 33.5 gives us 15.5, the variation- the long Feb spread is worth 48.5, Jan call is 20.5, debit to open 10. Gives us 18 (both WINS)

Now: Jan 7800 call, 3.5 Feb 7700 call 70.5, 7800 call 36.5

Standard calendar 33.5 -actually a break even as we paid too much(33.5) for the trade. The spread is now a credit 30, and our cost was 10. We’d take that

Trade 347 Silly Putty, or Silly Put Prices?

Going directional after our cheeky Santa rally combination -we sold the put to buy the call, but this time we go the other way- a risk reversal selling the 7800 call for 26 and buying the 7400 put for 27.5. We pay 1.5 and set ourselves in the ‘brace position’ for a bumpy landing! ( check this out, the call is 7800-7576= 234 points away from the money, the put 7576-7400= 176 ).

However,hose prices were? the 7800 call 52.5 and the woeful 7400 put 10.5 So what’s to do as this is a disaster! It’s such a rubbish trade give seasonality and lack of volatility or any whiff a potential drop. So we can double down or convert our position to a strangle and simply sell a 7600 put for 35

So, last time we looked 7800 call 53.5 7400 put 7.5 7600 put 23.5 -so this is a nothing burger as expected. The puts lost more premium, and in this nothing burger week there was er, nothing to trade.

Thus, the sobering position now, and as we expected, 7800 call 20.5 7400 put 5.5! loss of 15. Had we sold the 7600 put, it’s now 25.

Overall if closed out now we’d lose 1.5 debit plus (15-10= 5). 6.5 –we’d take that loss but we’ll run it for fun. However experience says when these go belly up almost immediately they never go well.

Now- A loss of 1.5 the 7600 put is 26 (sold for 35) Run this options salad to expiry.

Trade 348 – A FlutterBy -Far From a Pretty Trade

Yes it’s that time again, we have not had a butterfly for some time. We go for a big juicy 150 points, with a 7600/7750/7900 put butterfly, we will also get really crazy and try a broken wing put butterfly with strikes 7550/7750/7900. Those prices: 25,86(x2),206, gives us a debit of 59. The broken wing 16.5/ 86(x2), 206= 50.5 and risk of debit plus 50

This is expensive and may be a disaster, in a nutshell because we MUST be right. The journey towards expiry is unlikely to give us a nice exit point.

Now: 270, 126, 26, 13 which means the butterfly is now 270+26 minus 126×2 = 44, it cost us 59. Or, the broken wing ‘fly is 31, and cost 50.5 This week will be interesting! I should mention that an expiry below 7600 makes this worthless, and below 7550 is the worst case scenario for our least loved strategy.

Trade 349 Another Calendar Variation

Here we go again and yes, we consider calls overpriced. We sell February 7750 call and buy the March 7650/7750 call spread. We have a small credit of 6

Overall Delta is 0.20 so we may have to manage this, but note it was too late, in our own experience, to place a Jan expiry trade. Extrinsic premium is woeful. We may look at closing out before Feb expiry.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.