That Was The Week The Fed Said’ Cut’ Sometime in 2024

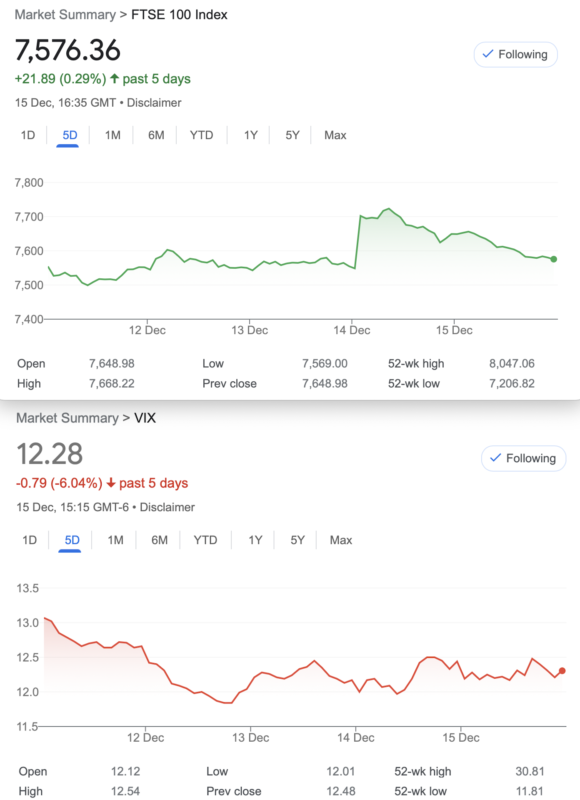

December the 14th is traditionally a day the FTSE goes postal. Meltups lasting weeks tend to happen on that specific day. So, you’d expect a seasoned trader to bear that in mind, would you not? Guilty of the ‘boredom’ trade or inaction for some time, yours truly decided to place a long and short call trade on 13th. With predictable outcome. Self proclaimed wisdom said, go in again, same trade but 10x better premium. Your deeply flawed trader failed at that hurdle too. The above weekly chart says it all. Back to the commentary.

Dovish words from the FED caused US markets to fly on 13th, and our lame old dog FTSE on 14th. This is a well trodden path of course but curiously, FTSE melted almost back to the same level as it started on Thursday. Global market watchers know DAX is hitting all time highs and the US is no laggard either. The US is riding on the back of 7 tech stocks. We know they are nothing like the 1999 tech stocks they must surely be susceptible to fashions. We can surmise, but cannot price that in. Market sentiment is generally priced off options. Currently it is saying ‘to infinity and beyond’.

History Repeating.

So, having been a Gonzo with my own trade, I dug a little deeper. 14th December was only once a down day- in 2017. However every year for 7 years the market has risen 3-5% up to January expiry. January is supposed to be a bellwether for the rest of the year. It’s the journey in between Jan and Dec that is interesting. I have, however in past years placed mildly bullish trades in December, but have never timed the ‘Santa rally’ . Readers may wish to search: Dunning-Krueger Effect.

Small compensation : https://www.cmegroup.com/education/courses.html

CME emailed a link to their tools, but of course they relate to the US market. There was a useful guide to some of the lingo we use, and it is always good to know if using online platforms. Example: RFQ, request for quote, which allows a glimpse into specific options prices, albeit fleeting. Insights and tools available to the American traders through CME are to be envied, though we DO have real time options prices. https://www.ice.com/report/265

Distraction Trades

ADA was $0.6214 now $0.6217

XRP was $0.68194 now$0.6247 Some big rises here, and a role reversal as ADA overtook XRP this week but dropped back a little.

DAX 2 break evens +30, 3 no entries- missed a couple of bangers Thurs and Fri but they were not on our time horizon.

UK Gilts were £16.76 now £17.33 little acorns? Saplings growing ever skyward, we hope.

Legacy Trades and 345, Something For the Season

Legacy Trades, 346 and 347 The New Expiry Month(Year)

As we inherit the long put spread Dec 7450/7350, from trade 342 we could close out or do something more interesting. So, we can sell another 7350 put for 31.5 on its own or as a short spread 7350/7250, as we can buy the 7250 put for 19. So we’d have either a put ratio spread, or the latter, a butterfly with zero risk.

How did that pan out? Our prices 7450- 41 7350- 20 7250- 11 So, our choices, close out the put ratio spread for 1 giving us 32.5 – trade 342 only gave us a tiny profit of 12.5 so we can make a quick 20 or carry on. The butterfly gave us a credit of another 12.5, but we run it as it’s currently worth only 12 and it has zero risk.

Last week: The butterfly is 9.5 the ratio spread gave use an additional 31.5 if it goes to zero we’ve still made £££

Those prices. 7450,7350,7250- 10, 3.5 and 2 it’s all gone a bit lame but we’d taken some juicy premiums. WIN but expiry did nothing more for us.

Trade 344 Magnetic Strikes ( That’s my idea of Sticky!)

So in lean times we need to find something that is cheap and will hopefully keep us out of mischief. It’s a long Dec put spread 7450/7350 41-20= 21 and there are many ways to help pay for it, but we know things are out of wack with puts trading at volatility in single digits. Let’s sell a strangle, yes it’s naked but with mitigation always from the side not under threat. We sell 7250 put for 11 and 7700 call for 11.5. Credit 1.5 overall

So our downside risk is at 7150 but on the upside it’s still 7700 unless we get creative with our long put

2nd Last week: 27-12 for the put spread=15 and the strangle is now 6.5 and 14= 20.5 It’s not looking great.

Last week 7700 call was 6, the 7250 put 2 but our spread 7450/7350 is 6.5. All a bit feeble. Loser but at no cost, we say it’s a DRAW

Trade 345 Do We Buy the BS?

Is a Santa rally on the cards? Let’s say (like those Ancient Alien Theorists)………. yes. We can create a ‘synthetic future’, but we don’t want a brutal delta of 1. So, we sell a 7350 put for 12 and buy a 7700 for 14. We thus have a small debit of 2 and a sold put has positive delta but what do the Greeks tell us? Add those deltas AND that theta! It’s NUTS!

This week – the 7700 call that we own is 6, the 7350 put we sold is 3.5 The waffling FTSE has done us no favours, but we have to do something each week.

BOOM! ![]()

The spread was a dramatic 28-47 so we’d have taken 35 thank you very much! WIN!

Trade 346 In the Dire Volatility What Can We Do?

We often overlook calls as puts are the go to trade when Vol is in our favour, but now we are faced with the sole weapon in our armoury-theta. So, it’s a calendar trade whereby we sell near month and buy far month. Here we sell the Jan 7800 call for 29.5 but here’s a twist, we will do a level 7800 call in Feb, and also see how we perform with a 7700/7800 long call spread in Feb.

Those prices: Feb 7700 call 92.5, and Feb 7800 call is 57.5. So the spread costs 35, we sell the Jan 7700 call for 29.5 so our trade costs 5.5. (Risk around 7900)

The standard calendar trade- sell Jan buy Feb costs 57.5-29.5= 28

Jan 7800 call now 26 Feb 7700 now 95.5 and the Feb 7800 call is 59.5. So: the spread is now worth 36 minus the Jan call at 26, gives us 10, but we did pay 5.5, small win to date. Meanwhile: the regular calendar trade cost 57.5 – 29.5= 28 Now it’s worth 33.5. Of course we run this

Trade 347 Silly Putty, or Silly Put Prices?

Going directional after our cheeky Santa rally combination -we sold the put to buy the call, but this time we go the other way- a risk reversal selling the 7800 call for 26 and buying the 7400 put for 27.5. We pay 1.5 and set ourselves in the ‘brace position’ for a bumpy landing! ( check this out, the call is 7800-7576= 234 points away from the money, the put 7576-7400= 176 )

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.