That Was The Week A Horrible Event Took Place

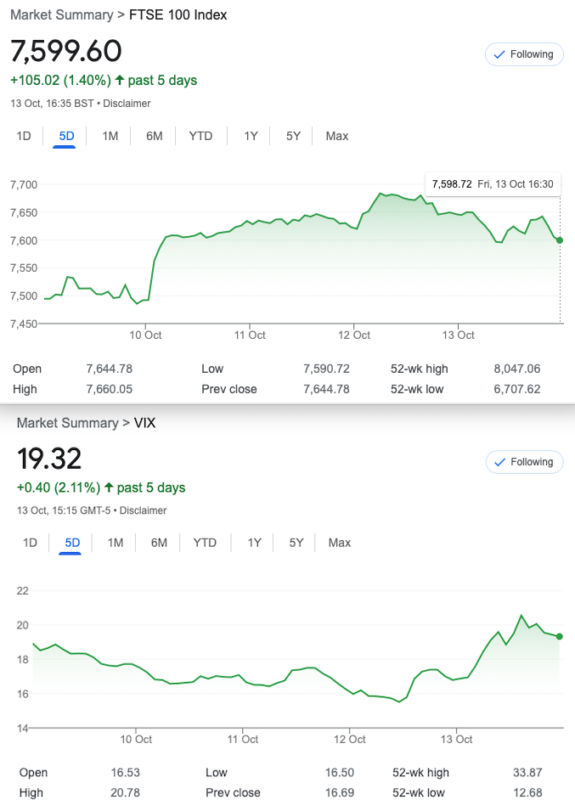

It is not our place to comment on events of such magnitude, but to reflect on the market’s reaction. Silly Tuesday would seem to cover it as an already overbought FTSE screeched skywards. There is a horrible expression attributed to Nathan Rothchild of that mind numbingly wealthy family. It goes thus: “The time to buy is when there’s blood in the streets.” And the reaction to the conflict was precisely that as the greed wagon rolled on in the hope of big fat profits from oil, armaments, pharmaceuticals, and pretty much everything else. Extreme events are contrarian for the markets https://www.investopedia.com/articles/financial-theory/08/contrarian-investing.asp And, in fairness the ‘blood on the streets’ does allude to the bigger picture, it’s not simply literal.

However, as usual yours truly is bearish on the plodding FTSE which has ‘misbehaved’ for some months now. Moreover options volatility has been shockingly low relative to the index’s moves. We recently mentioned the lack of dynamics in the S&P yet FTSE has done some meltups recently with the occasional dip which turns tail halfway through the day. Curiously inflation has not gone away and higher oil as an input cost to just about everything will of course be inflationary. So the vain hope of expecting interest rates to plunge to support a market that is drunk on free money, is probably not a good position. That is my 4pen’orth!

Freebie Education

I was invited to watch this week’s webinar and while they may be a little basic, often there’s a graphic or a little nugget of information we may have missed. So in that respect I try to catch as many webinars as I can, unless the boredom threshold is exceeded: https://event.on24.com/eventRegistration/EventLobbyServlet?target=reg20.jsp&eventid=4329063&sessionid=1&key=577E24B2E4217102434BC8B95948B88B&groupId=4986192&utm_campaign=OctoberWebinar&propid=136&partnerref=spm136&iopid=91180&utm_source=DedEmail&sourcepage=register

I believe the 11th Oct webinar is available on demand and there is a free powerpoint download. And, like us here…. it’s FREE

Distraction Trades

ADA last week $0.2602 now $0.2469

XRP last week $0.52268 now $0.48147 Another dull week in Crypto world, yet I read that Cardano had some kind of accreditation-will follow up

DAX 1 win +120 1 loser -30 3 no entries

UK Gilts were £15.96 now £16.22 A bit of hope, or maybe premature?

Legacy Trades: 333 – 337 and new trade 338

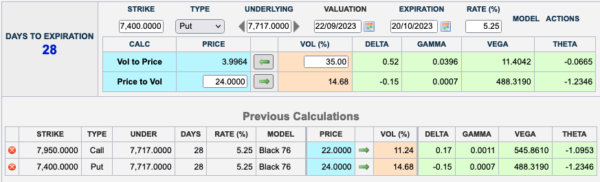

We have a legacy of a long October 7550/7450 put spread, currently worth 13.5

Let’s look at:

1.Convert the trade into a 7750/ 7650/7550 put butterfly. We buy the 7750 put for 98.5, sell TWO 7650 puts 61.5, giving us a credit of 24.5. And magically that buys back our short 7450 put. * Has not performed well but it’s 100% safe and the butterfly has some value: 15 (06Oct)

2. Convert to a put ratio spread by selling another 7450 put, giving us risk down 5% out of the money at 7350, it’s now a credit trade for 28 with a shot at collecting a further 100 if the FTSE takes a tumble. A tad underwater (06Oct)

3. Sell a 7350 put for 16.5, giving us an overall credit of 10 but risk now at 7250, with the chance of a max 100 points extra. Now worth about 16(06Oct)

4. That’s enough! Yes we could do allsorts with calendars, condors et but let’s keep it as simple as your frazzled (this week) author

First week: well the spread is now worth: 52-31 = 21 The abysmal market action has done nothing for us, we need a decent down move that doesn’t melt up one hour later. Our 3 trade choices have done nothing, but this is a game of patience.

The spread was 57.5 and 33 = 24.5 Another nothing week no particular advantage, but we’re in healthy profit

Last week: 103.5 and 57= 46.5 – Close out and be happy, say I. Of course we run to expiry for fun. WIN!

This week: 37 and 15 =22 A step backwards but we run for fun.

Trade 335, Picking Through the Scraps, Staying Neutral.

Honestly this is ‘one ugly market’, to paraphrase Arnie in Predator. Vol is ludicrous, but when we’re given lemons we make lemonade:

An almost delta neutral strangle. Selling the 7950 call and 7400 put. We have risk at 7996 and 7354 and can close out any time within the 28 days to expiry. Boring, steady yet it may get spicy and give us a chance to show adjustment.

So the call is now 8.5 and the put 25 -so far so good…..

Now(06Oct) 1.5 and 41 and another shining example of why I don’t like strangles

Now 1 and 10, we took in 26, so WIN!

Trade 336 Plagiarism or Theft?

Sometimes other people’s work serves us well and again a nod to Liz &Jenny of Tasty Trade for the classic Jade Lizard. A credit trade for ±50 with upside risk capped at 50. Here’s the trade: We sell the 7700/7750 call spread for 67-48=19. We also sell the 7450 put for 33. Maths PhDs will note the credit is 52 ….capitalism run rampant! Our risk managers will note the upside risk capped at 50, downside risk is at 7450 minus the credit, so risk at 7398.

Ouch! now 18.5 and 11.5 = 7 for the call spread and the put….. 57 So we are nursing a loss, but wait…. we are not futures traders we have options, and a credit of 52.

This week: the call spread is 26 and 15, the put is 15, gives us 26 so we’ve made 26 WIN! Of course for fun we run to expiry

Trade337 Time for a Curate’s Egg! When Vol is vile, we improvise

I don’t like these prices for calendar spreads, I don’t like the low volatility. (Amazing that the financial press bang on about volatility when there is none). So we combine a short call for premium, and a put ratio spread for no money. We sell 7700 call for 18.5 and (buy the 7400 and sell 2×7300s) giving us the 7400/7300 put ratio spread for 41 and 20.5(x2). Keen observers will see we only take in premium for the call. Logic of the trade? Should the call come under pressure we can adjust on the put side, should we see downside pressure, we can adjust and have the 18.5 credit to help out. And yes, I still don’t like naked short options…… in isolation.

This week: the call is 26, the put ratio spread is 10- (5×2) = 0. Not sexy is it!

Trade 338, Horrible lack of Vol still

Slim pickings but we still have theta, so here’s what we do, we BUY a November strangle and SELL an Oct strangle, those prices:

Oct 7450 put– 15, 7750 call-15, Nov 7450 put 67, Nov 7750 call 66. This is the most expensive trade ever but we can take in premiums of 30 from the 133, costing us a lofty 103. However the chances of us losing much are small, and the theta of the Nov options will be far less than the Octobers which we hope will expire worthless, or go to almost nothing next Thursday. It’s simple, it could get ugly, but hard to see anything else worth trading. This will not be an explosive winner, however.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.