That Was The Week Somebody got Excited about CPI

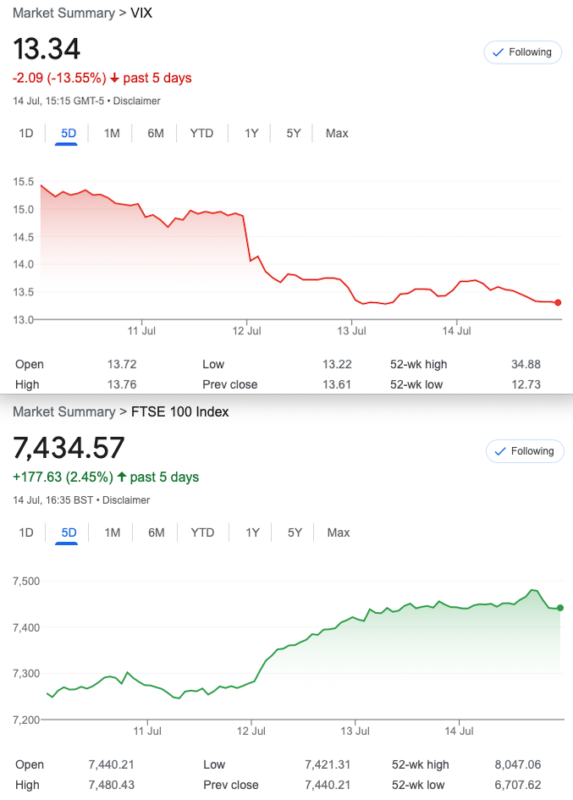

Wednesday saw a big 1.83% rise on Wednesday as the market joined the dots. America’s Federal Reserve, the FED may not have to keep on raising interest rates. Inflation seems to have moderated, and the US’s latest CPI number was 3.0% down from 3.1%. The number and the FED’s next moves may not be as easily interpreted as some believe. Of course the funds that can only buy… buy. VIX is again in the ‘restroom’ and is making our job difficult. I have trawled the options chains each day, near month far month and even very far dated, and found nothing to inspire. When we only have a hammer and the market gives us lemons…… I believe that is the expression.

Yet again the disconnect between £ and FTSE- both rising. That is really not supposed to happen, though I have pointed out often that it’s nonsense. Making our exports cheaper has been irrelevant since we imported far more than we exported. Wasn’t that always the case? America’s aim to inflate away debt with a cheap dollar may be working for them, for now. Our inflation remains stubbornly high yet the £ is rising. The dismal art of economics remains dismal and these tired correlations? Forgive me, but we deserve better. Some of the ‘guff’ from the financial press going back to FTSE at 8000 as a cheap buy? It’s not helpful. FTSE P/E at around 14 would be about fair value according to that long standing metric https://markets.ft.com/data/indices/tearsheet/summary?s=UKX.P:FSI However it ignores so many factors when taken in isolation. You’d buy the S&P 500 with a P/E of 14, however. https://www.macrotrends.net/2577/sp-500-pe-ratio-price-to-earnings-chart

Rant over!

Distraction Trades- Crypto Shocker

ADA $0.3349 up 16.31% from last week- was up >20% yesterday

XRP $0.4841 up 55.24% from last week it hit>60% in a surprise move -what’s going on? https://crypto.news/xrp-trading-volume-skyrockets-amid-favorable-court-decision/

DAX: 3 losers 1 break even +30 1 win +50

Gilts eft: U.K. Gilt UCITS ETF (VGOV) £16.37 was £16.13

Trades 321-325 A few Wins, and Trouble finding Trades

Trade 321 in a flat low vol market- Yikes!

Let’s get spicy in this season of low volumes low volatility and low expectation of actually having a smart trade. Theta is not our friend so we look to take on more risk and sell more options than we buy. Here we sell 2x the near month, July strangle 7400 puts,(24) 7825 calls(24), and we buy one August strangle: 7400 puts (55.5) and 7825 calls (44.5) .Here’s the numbers: 55.5+44.5= 100 and 24+24 (x2)= 96. Our cost therefore is 4

Overall theta was around 1.92 and Deltas, we are not far off neutral. Risk – well it’s going to get ugly outside of our strikes. Hand on heart it’s not ideal but we always remind readers it’s about learning, winning is the cherry on the cake.

July put 7400 56, call 7825 4 August Put 7400 101.5 Call 7825 11.5 Gives us 56+4= 60 x2 =120 for July. August: 101.5+11.5=113. Last week it was in a loss 7

Previous week….peachy July call 3.5 put 22, Aug call 63 and the put 12 Gives us 75-58= 17 our cost was 4 remember. More time to go yet.

Last week week- Ouch! 1 and 157.5 (x2) for July strangle 2 and 207 for August A loss of 316-209= 107 -will the market recover?

This week: July: 7400 put 20 7825 call 0.5. August 7400 put 83.5 7825 call 4.5 July strangle 20+0.5 x2= 41. August 83.5+4.5=88 Our cost was 4 So we have a nice profit 43. We ‘run for fun’ to expiry but we’d take this any day of the week

Trade 322 Some Movement but Volatility Being Supressed

Again we can only use theta in this ludicrously low vol environment. It is a concern but if we take a real plummet, we will at least be able to morph/adjust/roll. The above calculation: https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html?utm_source=LINKEDIN_COMPANY

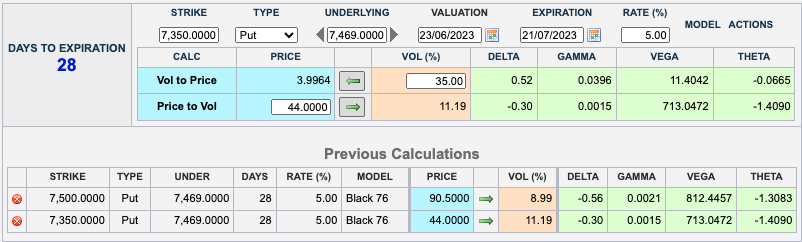

We are doing another old chestnut, the put ratio spread. Buying the 7500 put and selling the 7350 put twice. Cost:90.5-44×2= 2.5 Logic of the trade? We have risk down at 7200, and we may find this trade in profit quite quickly above that level, even if we have a blip up to 7600 or so. Should the FTSE dip lower than 7200 we will adjust, if the market shoots up we have no risk other than our tiny 2.5 debit

Previous week 44 and 16 x 2, we are in profit ( 12 -2.5) =9.5

Last week – 246 and 120×2 We are still in profit and this may line up very well.

This Week: 7500 put– 69 and 7350 put 10.5 (x2) Minus cost to open 2.5 Gives us a profit of 45.5 -again we’d take that but ‘run for fun’

Trade 323 Horrible Trade- Let’s Do it!

We will place the much acclaimed ‘broken wing butterfly’. By way of explanation, the ‘broken’ part comes from the cheaper wing strike being further out, so instead of say 100 point wide 7450/7550/7650 butterfly (using calls here) The 7700 is bought instead of the pricier 7650. I wonder if it makes sense. And will it work?

We buy the 7450 call 131, sell two 7550calls 63.5(x2) and we buy the 7700 call for 13.5 Thus our cost is: 17.5

Note: The 7650 call was only 23.5 so this is bonkers, IMHO!

This week: 9.5 3×2 and 1.5. =5 So as if to confirm our bias against these, the numbers are horrible but we might as well stick with it

Those prices now: 36.5 7.5 1 Remember the ‘body’ 7550 strike is x2. Thus even with this horrible strategy that cost us 17.5 we have 22.5 a tiny profit

Trade 324 Smart Trade? Probably not.

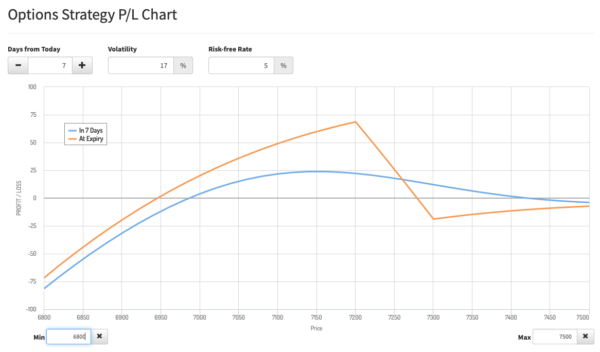

This is a huge ask, but I’ll try a reverse calendar, in the absence of a smart trade! We sell the August 6900 put 40 and buy 7300/ 7200 July put spread 88.5 -45.5= 43 So our cost is 43-40= 3 Logic of the trade? We want to own the Put spread but don’t want to pay for it. The trade makes a profit in various scenarios but there’s always the chance the market will tank, but if our spread hits the max 100, we then have a ‘war chest’ to adjust. Here’s our P&L

Here’s the link to the calculator: https://optioncreator.com/stqx435

NB: the July 7400/7300 spread is 69 and the Aug 7050 is 64 these may be better levels. Now, the spread: 20 and 6=14, the Aug put 19.5 loss 10.5

August 6900 put is now 12.5 the July 7300/7200 put spread is 6 and 2.5 =3.5 Horrible! Our cost was 3 so it’s a loss of 12.

Trade325 An Old Chestnut

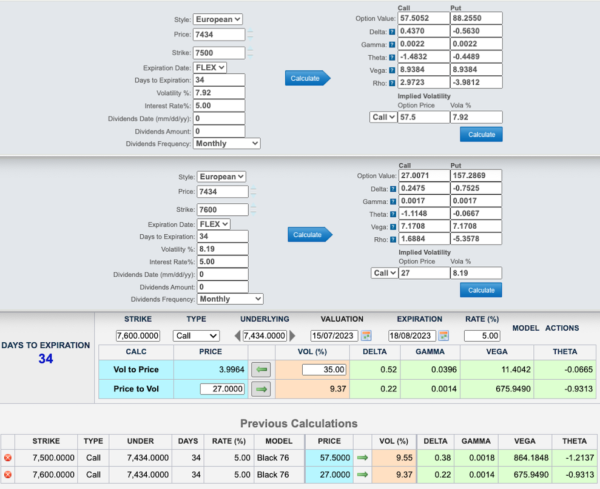

In the absence of fair looking trades we go for a call ratio spread. Thus we have some directional bias and a fair chunk of mitigation if we’re wrong. We buy one August 7500 call for 57.5 and Sell 2x 7600 calls 27 Our cost to enter is thus 3.5 which is cheap as chips, and the logic of the trade? We have theta on our side by selling two calls against the one we bought. Here’s a new take, I have for many yearss used the CME calculator, https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html?utm_source=LINKEDIN_COMPANY but, by chance tried the OIC calculator https://www.optionseducation.org/toolsoptionquotes/optionscalculator.

Some disagreement and while the CME(top one) uses Black Scholes, the OIC may use a variant, I was not able to find out. CME allows us to keep a ton of calculations on screen, while the OIC one is a pain in the rear quarters! We can presume that as we are trading relationships, the Greeks are relatively fairly calculated.

For those new to options:

https://optionsinvesting.co.uk/special-edition-how-options-work-1/

https://optionsinvesting.co.uk/special-edition-how-options-work-2/

https://optionsinvesting.co.uk/how-options-work-page-3/

Contact: surreyhantstraders@gmail.com If there is anything you’d like help with, we all started somewhere and yes, it can be baffling.