300 Trades 300 Weeks. Our Readers Get Our Thanks, We Hope They have Gained From Our Real World Education.

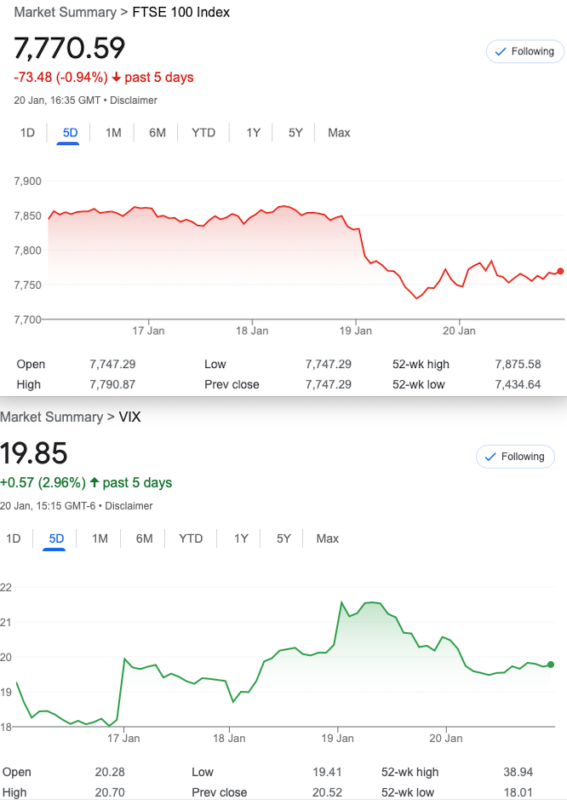

We had the first of the much needed down days, as FTSE continues to defy gravity, and valuation. https://markets.ft.com/data/indices/tearsheet/summary?s=UKX.P:FSI

According to the FT, the FTSE’s valuation has smashed up 30% since mid October. Trusting the FT’s integrity, does this really mean that a few weeks make the FTSE100 worth half a £trillion more? Valuations are made by people selling us something, and yours truly has a problem with it. However do NOT pay any attention to my bearish bias. I have been this way since we got decimal coinage! We can only trade what we see, hence using VIX as a barometer for all markets. VIX, is still in the doldrums. NB. I speak as a retail trader and there may be subtle reasons why FTSE’s P/E is so high

So, 300 trades, and while we don’t count winners and losers as we are not an advisory service, we seem to have done rather well. Cast a critical eye over the content. You will see that despite lack of insider knowledge, with an unhealthy bias, yours truly has selected good trades with a modicum of research. So what’s the secret? An eye on risk primarily. Profits come and exits are discretionary. Given the same trades no doubt many others would do better than us.

Our outcomes may be questioned, and sometimes running trades to expiry does not pay off. Clearly there are many exits en route to the 3rd Fridays, that are better than ours. Some, may be worse!

Distraction Trades

Apologies, but have yet to find another suitable trading vehicle, other activities have taken precedence.

ADA $0.3660 We remain highly skeptical.

XRP $0.41066

DAX 3 no entries one b/e +30, one win 150 Not too shabby, but boring.

Legacy Trades and ….300 We Have a Great Track Record Still. The More We Trade, The Luckier We Get.

Trade 297 The Widest Butterfly in The Village

So as above we now have banked 4.5 and we will chart the progress of the butterfly. A 400 point wide spread butterfly (7400/7000/6600) we own for free has to make ££££more. Anyone NOT noticing the power of options yet?

Those prices were: 67.5 13.5 and 6 So our butterfly is worth 67.5+6 minus 13.5×2= 46.5

Was: 54.5 8.5 and 3.5 =41

Was almost zero. However we ran it as there was nothing to lose. We have nothing to win now, but it cost us nothing. Sad outcome as it was a loser

Trade 298 Is This a New Bull or simply BS?

Calls -our least favourite options! So- let’s try a ratio spread 7600/7700 132.5 and 66.5 x2=133 We are buying one 7600 call and selling two 7700 calls which would benefit from a drop as well as theta working for us, and it ‘only’ costs margin. risk at 7800. What could go wrong?

What could go wrong indeed? Those prices: 255.5 and 158 x2= 316, so our trade was 60.5 underwater

Choices(options)

1. We convert our ratio spread into a butterfly by buying the 7800 call at 72. On its own that makes it an expensive butterfly, but it’s a choice.

2. We pay for the 7800 call by selling something else, more calls at 7850 40.5 7900 20. We then have risk above 7900 and a cost of 11.5

3. We do a calendar spread buying the Jan 7800 call and sell the Feb 8000 call at 75.5 Kicking the can into the long grass. What would a central banker do?

4. Close out the 7600/7700 spread for 100 buy back the 7700 at 158 and sell the 7800 at 72 So we take in 100-(158-72)=24

This is an unhappy trade given our record of reasonable, though quick selection. However it gives us a chance to look at adjustments, and we give up our money very dearly.

Yay! On Thursday we close out: 151 minus (54×2) =43 WIN!

Trade299 Getting our Revenge( Tip of the day: Never ever revenge trade)

We want to have some long exposure to puts as vol is ‘at a low’ but we never buy outright. We buy a put spread, buying the Feb 7900 put selling the 7750 put those prices :180.5 – 117.5 = 63. Then sell the Feb 8100 call at 45.5 to help pay for it. Thus, we have a fair bit of wiggle room if this takes off against us to the upside. Our cost 63-45.5=18.5

Again Thursday was optimum close, with those prices: 186 102.5, 10.5= 73.We paid 18.5, so 54.5 profit WIN! (Of Course we run for fun)*

*Closing price, not actually the low of the day which would have yielded another 20

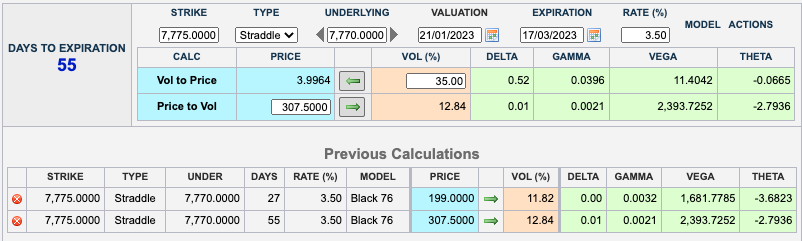

Trade 300 A Milestone, Can we match Past Performance?

Here’s something odd. Open Interest for Feb puts at strike 6000 19,490 and strike 5900 17,208 both strikes seem to be priced at 1.5 so if you were buying a protective put spread technically it costs zero. Thursday: OI at 5900 37,960 so the 6000 puts were created on Friday. I have no idea why these very far OTM puts are trading thus. Not sure if they know something!

OK let’s have a look in this miserable low vol environment. Oh my! Yet again, the odd ratio calendar straddle rears its ugly head. Say whaaaat? It’s a multi leg strategy buying cheap near month(Feb) 7775 straddles for 102+97=199 x3 and paying for this by selling 2(two) March 7775 straddles. 149+158.5=307.5. Straddles are the combination of calls and puts ATM -at-the-money. So we pay 199×3= 597 and take in 307.5×2 =615. Our credit therefore is 18 our risk is that the market goes nowhere, but if those put trades are telling us something we have the advantage.

Note the theta (time decay) works against us x3, and time is not on our side (27 days) against the March lower theta x2, and 55 days to expiry. Not clear about this? Email us: surreyhantstraders@gmail.com