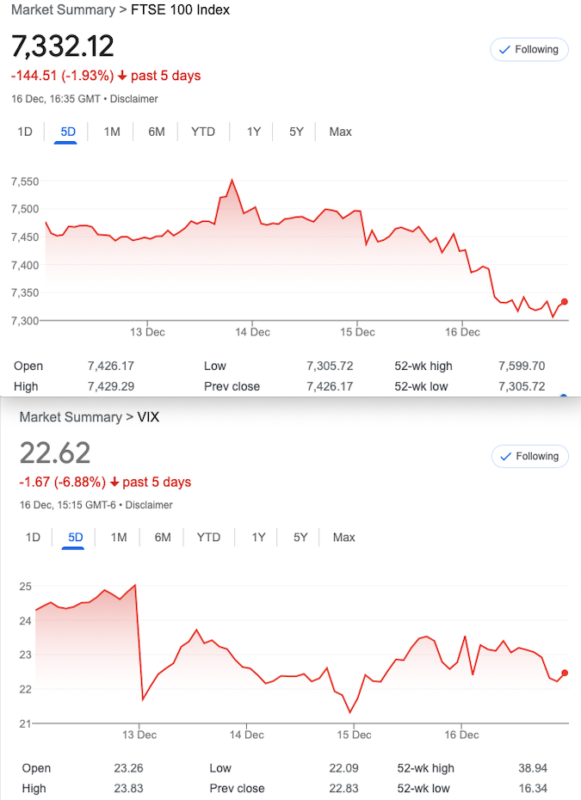

Deliberate Mistake? VIX Down and Indexes Down???

What’s wrong with this picture? S&P 500 down 2.2% this week and yet the VIx is 7% lower. Shouldn’t happen, has happened- in another twisty turny episode of expiry shenanigans. FTSE expired after 18 minutes of auction apparently at 7350. So, a battle royale was playing out at 7400 and open interest told us there were 22,000 puts at 7400 on expiry day. As you all know an option only exists when 2 parties agree to the contract, so who luckily got out of their short puts at around 7400? And who was long the 7400puts and made 50 in the end? We love it! Fisher Black ( Black Scholes Merton) notably had a jaded opinion of PIN risk -look it up.

* Quad witching -quarterlies and monthlies expiring in futures and options

What should have happened this week with VIX?

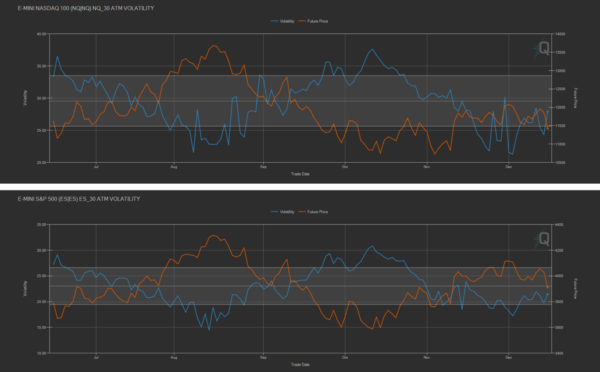

Apologies if it’s not too clear, red=futures price, blue is volatility. However, they are inversely correlated as you’d expect. Time and again in 2022 we have seen this go awry. Why, is anyone’s guess but sometimes people are not willing to pay up ‘big’ to buy protection. However, there are times when people are not willing to sell cheap, or maybe it’s complacency. It can never be perfectly regular.

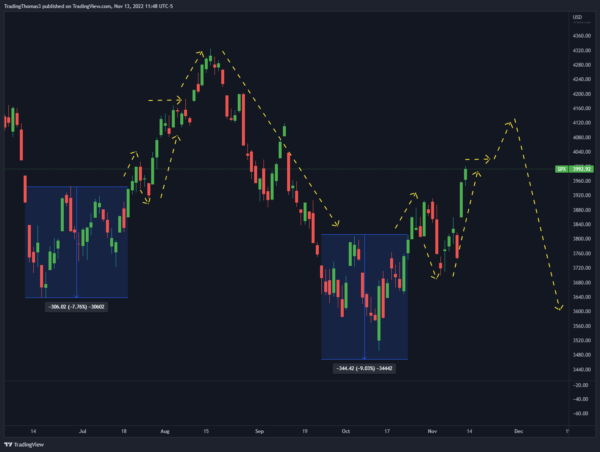

Fortune Telling Time

This chart was created back in November. So, is it predictive or just a piece of frivolous speculation? Whatever our view, it is not a great idea to make such predictions, right or wrong. So while I hold chartists like our friend here in high regard, the future prediction if right, makes the next prediction a lot harder. A million hopefuls will have bet the farm. Thus we come back to following the real money, and being a little nebulous( if that’s possible). In other words we take our view based on the options world view.

Distraction Trades

ADA $0.2636 Despair

XRP $0.3510 Misery!

DAX 3 no entries(missed 400) 1 break even +30 1 win 170

Over the holiday it might be prudent to drop crypto and find some other instruments of torture. Watch this space.

Those Weekly Trades 293 – 296 with Expiry Done and the New 297.

We bought the Dec 7500 call for 58.5 and sold 2 of the 7600 calls for 29(x2)= 58

In anticipation of the Santa rally -we could make the max 100 with FTSE at 7600, we have risk at 7700. We have NO downside risk

Was 88 and 42.5 x2, gave us a credit of 3 this week 113, for the 7500 and for the 7600, 53×2= 7 let’s not get carried away.

Was 53 and 18(x2) which is 17-1/2 =16.5 in profit.

Went out worthless so that 16 was a result. At least it didn’t lose

Trade 294 These Animals Keep Buying the FTSE!

OK so it seems there’s a battle at the top around 7500 and while our call position makes ££££ around there, if it drops, it’d be nice to cover that event too. We need to own some puts. Let’s buy a 7500 put and find a way to pay for it. Let’s go high risk and sell 3 puts to buy one. We will sell the 7250 strike put x3. So we have to pay 88 for the 7500 put and we collect 25.5×3. Our debit therefore is 11.5 with max profit 250. Where’s our risk?

Can you see at 7250 we make 250, but at 7150 the short puts are worth 300 against our now, 350. So we need to ‘get out of Dodge’ if this market gets bearish big time. Break even then is at 7125 So in combination we have these risks: for trade 293 at 7700, and 7125 from trade 294 with potentially big gains in between.

Those prices now: 7500 put= 43 and 7250s= 10.5×3 = 11.5 -watch this fly!

7500 put 71.5 and 7250s 11.5 x3, gave us 37 WIN! We run it too and make 150 WIN WIN WIN

Trade 295 December, Santa rally yadda yadda

Regulars will know we have done ratio calendar straddles a few times but never with much success. Rather than keep such a pristine record sheet of wins, sometimes it’s good to see the warts an’ all moves. We buy 2 of the current month straddles( 7550 put AND call) and SELL the same straddle in January.

Those prices for Dec 7550 call and put 80 and 60 for January: 157 and 122. So 140 x2, and 279 so we pay a penny.

The logic of this is that a sharp move would be of greater benefit to the short term volatility, and therefore any price increases in the near month would be relatively greater than those January prices. Here’s the calculator https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html?utm_source=LINKEDIN_COMPANY

And for fun, check out the gamma and vega -but be aware of the brutal theta. There’s not a lot of hope but it’s fun. Let’s also explore the possibility of doing the reverse trade too.

Dec straddle 32 and 100.5 Jan straddle 105 and 156.5 This is such a bonkers trade and really not recommeded for expiry week, so we close out for tiny credit 3.5 But that’s not all- we run it for fun,though cannot see any possible way to profit now. Perhaps the reverse of this trade is the winner.

On Tuesday this was making 31 at expiry ….. Jan Stradle 38 and 239=277 Dec straddle 200×2= 400 WIN WIN WIN 133

Wow! Did not expect that-it just shows that with big moves this is a killer trade,and the market was looking wobbly

Trade 296 Ding Dong What Could go Wrong?

We no longer have a calendar spread-(we did!)

Here’s something to mull over in the festive season ( yes, pun intended!)

We will buy Jan 7400 put, for 97 and sell the Jan 7000 put for 31, and for the Dec expiry we sell 3x 7300 Dec puts for 16×3

So we have the 400 point wide Jan put spread and sell the 3 of the Dec puts but we still pay …..18

Classic! Our cheeky 3x 7400 puts went out worthless, and the Jan put spread gave us: 145 and 35.5=99.5 Minus our cost 18, we make 81.5.WIN!

We can run this spread too or create a 7400/7000/6600 Butterfly for credit 35.5-13= 22.5 Which gives us ……..

Trade 297 The Widest Butterfly in The Village

So as above we now have banked 4.5 and we will chart the progress of the butterfly. A 400 point wide spread we own for free has to make ££££more. Anyone NOT noticing the power of options yet?