That Was The Week We Saw The Comedy Money Rush In!

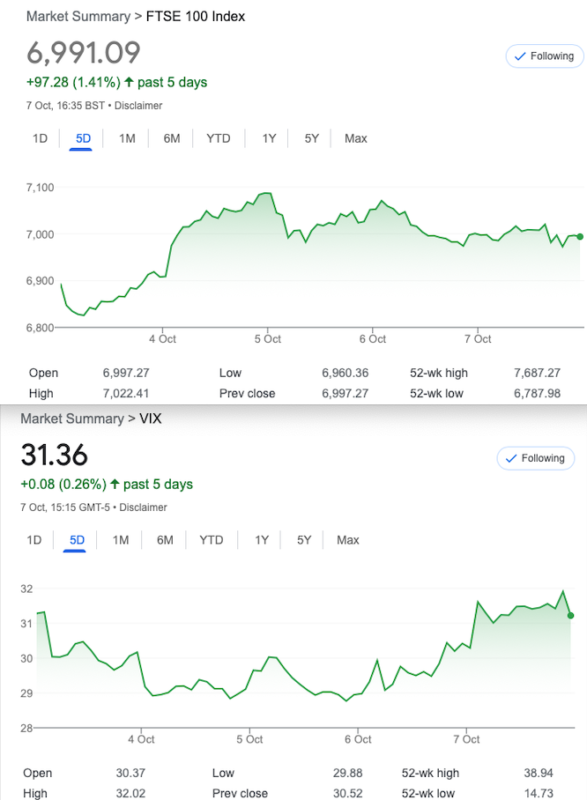

Those little fundies were thinking ooh, look at it go. They were starting to think their buy and hope, ahem, strategy was going to work. Well, the S&P made a lame 1.26% rise on the week. So, they had their brief moments in the sun while Friday saw some brutality to all indices except FTSE. OK apologies for the cynicism, though my ISA is performing as if I’d set fire to best part of five grand!

How Options Work

Sorry if anyone did not wish to receive the first 2 editions of How Options Work, but it is hard for people to grasp the concepts. Imagine the volume of options trading if the majority of people actually did ‘get it’! So it is hoped that small chunks will lead up to the full picture for people new to options. I can still recall my first options experience, with VOD cover call. Zero downside with the options trade, but a bundle of nerves all weekend! (VOD smashed up, my covered call made 14%, VOD made about 80% if memory serves)

Distraction Trades

ADA $0.4249

XRP $0.51932

DAX 3 no entries 1 loser,(stop is 30) 1 win for 300

Not much to say but crypto is no longer on my radar, there is enough to trade without an unquantifiable ‘asset’

Trade 284 One near-the -money, two further out

Let’s take a look at an old staple- the ratio spread. We buy a higher strike put then sell two or more further out-of-the-money puts. As we have a legacy 7200 put from Trade 283 let’s use that and so we have 2 scenarios: We carry on with our free put, and sell 2 of the 6950 puts or we just open this as a new trade 144.5 – (2×73.5) A tiny credit to enter, or we are banking 177 as a continuation of trade 283.

Where’s the risk? We’d get a bit fidgety at 6700 and if the market lifts off again we may bank only a modest profit, but we have 2 lots of time decay versus one.

Last week. Yowser!!!!!

The 6950 puts were now 140 , the 7200 put is 268.5 . So, a loss currently (140×2= 280) Gives a debit 11.5

Cut losses and move on? The eternal question- whither the market? We don’t know but let’s take a pragmatic look, bring on the Greeks:

The Greeks!

Those Deltas 41×2- 64= 18. So at £10 a point for every 1 point the FTSE moves against us, costs £1.80, but that is an oversimplification, gamma, theta and vega will all need to be factored in, so by close of play on monday we may see a little buying coming in. Thus, we may see our position go positive. Rho can chill for the time being! ( Yes I got the interest rate wrong but it’s really academic) Calculator from CME https://www.cmegroup.com/tools-information/quikstrike/options-calculator.html?utm_source=LINKEDIN_COMPANY

Last week: our short 6950 puts were 174 x2, and our long 7200 put is 330. Still seeing a small loss of 18 but we soldier on, and look at how we morphed into 285, and did it fare any better?

Now those prices the 6950 puts are 95 (x2)= 190 and the 7200 put is 238. Giving us a healthy 48 WIN! (but we’ll run it too)

Trade 285, Ladder Time

Juicy premiums, yes, but again let calmer heads prevail and we can connect with Trade 284 by buying the 6700 put which creates a 7200/6950/6700 butterfly. But we don’t want to pay 69.5 for that 6700 put so we will finance it by selling 2x 6500 puts. We take in 80, giving us 11.5 credit. Now our risk is lowered to 6500 but we are in a 2×1 ratio, we are short 2 puts. We could also have looked at a strangle: selling a 7350 call (35.5)and a 6700 put (40) We would have upside risk >7350 but if the market did shoot up again, we could take some profits from the put position. This is going to be fun running to expiry with updates along the way. Hope everyone’s keeping up, but to summarise:

Long 7200 put and 6700 put. Last week: 330 and 88.5 = 418.5 Ouch! shorts were 452 or 5.5 in credit if we had sold a call

Short 6950 put x2,174×2 = 348 6500 putx2 = 52×2 or (or 6500 putx1, 7350callx1) ( 52 and 13 )=65

Losses turned around and now outlongs:7200 put 238 and 6700 put 34.5= 272.5

Shorts: 6950 puts at 95×2 6500 puts at 16.5 x2 = 223 Gives us a credit 48.5 Again we run it but it’s a WIN

Trade286 Playing Safe, FTSE =6893

Assuming margin is an issue then using regular spreads is the way to go. Regular followers will know where this is going. Iron……. Condor! We sell the near month options with strikes nearer the money(the index) and we buy a protective put and call

Here we go: we sell the 7250 call for 25.5 and buy the 7300 call for 18.5 AND we sell the 6700 put 88.5 and buy the 6650 put for 77.5 Mental arithmeticians will know how this pans out. 25.5- 18.5= 7 and 88.5-77.5= 11. 11 plus 7= 18. Our risk therefore is 50-18= 32.

Where is the risk? 7268 and 6682 Anywhere in between gives our max profit 18. There are 14.2 trading days in which to be wrong!

Now: 22, 15 (calls) and 34.5, 28.5(puts) so we have 7, 6 =13. We sold those spreads for 18, we’re on the right side of the crazy.

Trade 287 Stepping up the Volume

Let’s go spicy with a big old calendar spread, selling Oct options, buying Nov options. What can we find?

We’ll do a 2 speed trade -a ratio calendar selling 3 front month buying 1 far month, and…….. doing 2×1

The 6700 put for Oct= 34.5 for Nov= 103.5

a) 3×1 – is zero cost ( there’s alway margin)

b) 2×1 more conservative but it costs us- can you see it? 34.5

It will be informative seeing how the trade unfolds.Typically these have done very well in the past, and we may have the challenge of needing to adjust.