That Was The Week of Crazy Buying, Crazy Selling

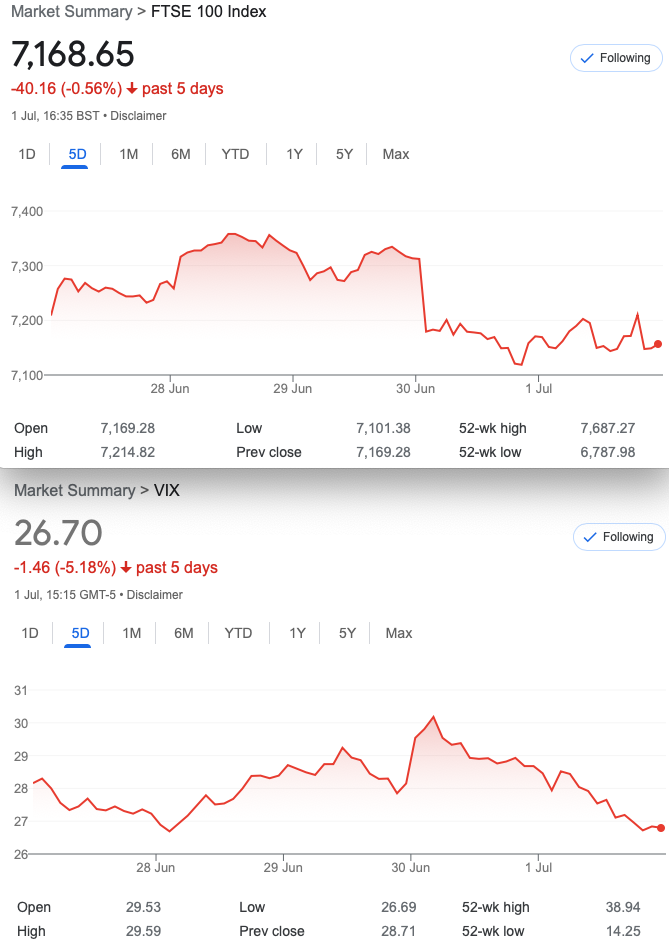

From last Friday’s buying frenzy to the ‘crazy elevator’ effects seen this week the FTSE ends virtually flat. This trader has seen some curious anomalies such as call volatility matching put vol. Call prices must have been bid up massively but we are back to normal with call vol about 60% of put vol. Precisely what you’d expect. Other years may have strayed from this norm too. Greeks( options metrics) have a way of telling us what the market’s expectations are and trading calls at 20% or more vol is highly unusual when put vol is about the same. We’d expect to see put vol around 32%. FTSE’s ensuing buying frenzy in the context of so much bad news was heralded 2 weeks ago. I can think of one trader who didn’t pick up on this. CME’s calculator is such a valuable tool. Other calculators may be available. Meanwhile:

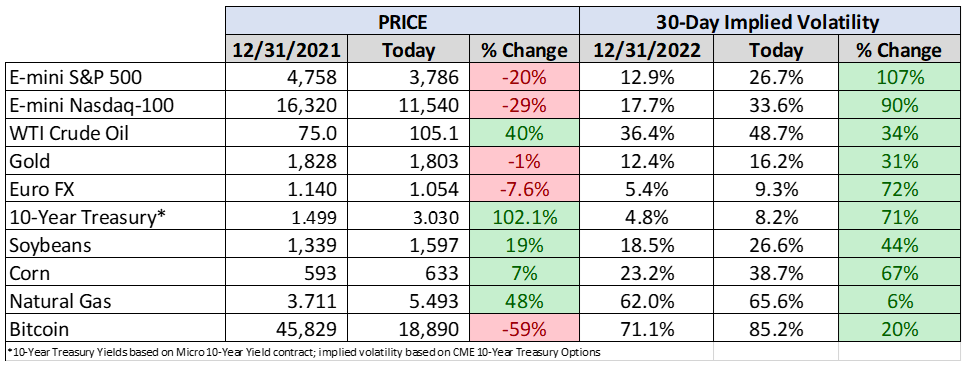

CBOE kindly gave us this week’s graphic as we hit the milestone of Q2 end. First prize goes to volatility and with some humility, this trader says thank you very much. We look back some years to see when Vol was so flat it was just so difficult to take any trades.

The Ugly Years:

Sharp eyed readers will see how 2017 was grim on the vol front. Backtesting confirmed that while my strategies would have yielded 50% profit, it was just too uncomfortable to take those trades. We know vol is mean reverting but any short put strategy worked well as FTSE rose. So currently we are almost spoiled for choice as options prices offer good variety in trade entries. We may, however be better off jumping in, taking the trade and being vigilant and giving ourselves enough wiggle room to adjust. Trading should be mechanical. Trading should be intuitive. Both are true and it’s a combination of factors in sensible proportions that combine to make a good trader. We are all a work in progress, and never stop learning.

Something for the Weekend

A bit of fun – I have no idea about the exit, and of course we can cherry pick, but the principle is interesting: Buy at the close and sell next day. Currently the skew YTD is 70 up days, 58 down days. But you cannot of course control the trade when the market opens down 100 points. However Monday will likely be an up day, so….. What do I know? Don’t do this!

Distraction Trades

Crypto……. oh dear

ADA Cardano $0.4483

XRP Ripple $0.3118

DAX 3 no entries,1 loser 1 win 150. Arguably the strategy makes money but is it an optimal system, or is there something better? While it’s a horrible grind you only need to be at the screen for about an hour from 08:00 am. Where there’s no entry you get the day off.

Legacy Trade, Trade 272 and new Kid 273

It’s been a while, but we never advocate naked trading. Partly naked, this put ratio spread despite the massive rise on Friday offers some value. We buy the 7100 put and sell 2 of the 7000 puts. This gives us a credit of 94.5 and (67.5 x2) = 40. Now to convert this to a butterfly would require the purchase of a 6900 put -currently 49 and to offset the cost, sell a 6700 put 26.5 But this is a course open to us knowing that relationship may remain of similar price, should we need to lower our risk level.

It’s now 36 ( 99 and 67.5×2 ) Barely a change

Trade 273

What do the numbers tell us? Calls are expensive so the market may be mildly bullish -we note the FTSE future, after hours, and US closed up on Friday too. So let’s have exposure both ways with our old friend the Jade Lizard- we sell a call spread and a put. We have no upside risk, because the risk is 50 and the credit is 50.

Our strikes, therefore our call spread: 7300 call for 50 7350 call for 35. Thus our call spread gives us 15, so we need the 6850 put for 35. For once the arithmetic is straightforward. Our risk to the downside is thus at 6800.