That Was The Week -All Gloom until ‘Magic Friday’

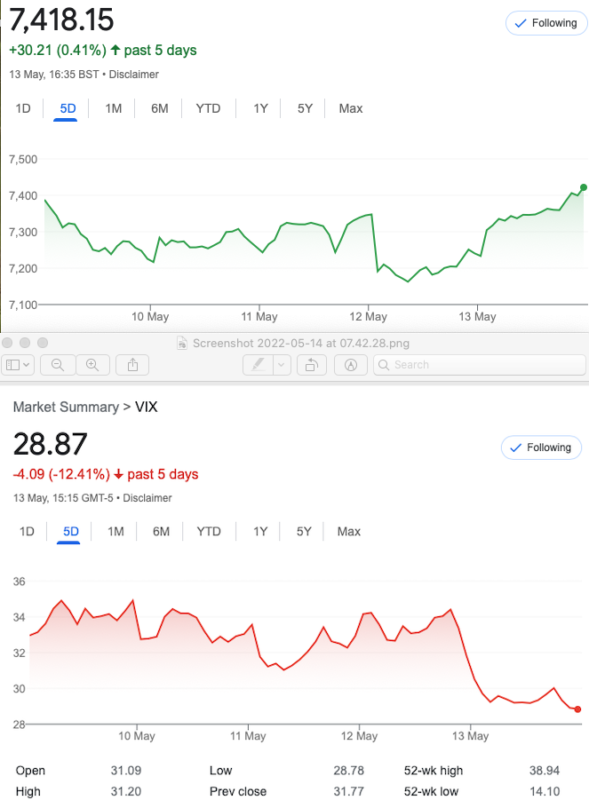

So, the doomsayers and the omen of ill portent Friday 13th failed to cool the ardour of our bizarre index. Quite what fired Friday’s move is a mystery to yours truly. However the week ends more or less flat, which is par for the course. And, next week is expiry which may be quiet as per tradition. We trade what we see but and additional caveat in that nobody seems to know what the heck is going on with VIX. Retail traders have contributed to the volume of trading but in the US, options volumes are up massively, while showing an increase equal to inflation in the UK.

Confession! I missed the first few minutes of an excellent CBOE webinar, the replay of which can be found here: https://www.cboe.com/insights/webinars

As per always a really interesting presentation backed up wit hslides and a quick Q&A. However my question was only answered in another questioner’s enquiry. My question was simply when do you exit? Outrageous question, but the answer came back (bearing in mind this was about short legs ) Gamma tends to go ballistic in the last few days before expiry, so roll.

Portfolio Protection

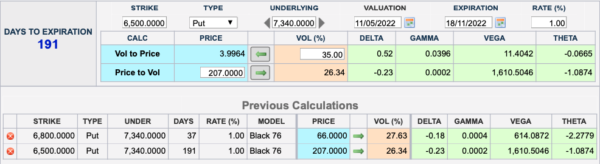

While the presentation was concerned about protection of long (owned) stock market assets, the strategy had not occurred to me before.The strategy is a reverse ratio calendar. Say whaaaat? I hear you say. Well here’s the plan and the idea is to be gamma neutral with no cost/tiny credit. You buy 2-3 long dated puts and sell 1 near month put. And, here’s one I prepared earlier

Hopefully you can see the Jun put has 37 days and gamma is 4. We need to buy 2 Nov 6500 puts, to be gamma neutral. So what’s the deal you ask? You are buying massive delta, massive vega and the idea is that theta is paid for by the selling of the Jun put. We preserve our capital. We have huge insurance against a market drop. Our position currently is losing a bit at the Nov puts are now 183, the jun put 48. So, let’s monitor this for fun.

Distraction Trades

ADA too ugly to mention!

XRPUSD same as ADA!

DAX Not a single entry, as the chart looks like a plate of spaghetti! Thus a major victory as our system kept us out of crazy moves and therefore losses. This is somewhat ‘tongue in cheek’. Other traders may have made out like a banker.

Legacy Trades 263, 264 and 265 May Expiry. 266 Can we cook up a peachy trade?

7550 /7700 call ratio buying one 7550(155) and selling two 7700(73) calls. Debit 155-(73×2) =9.

Risky? Not in the way you think it might be. Max profit 150-9=141 Risk at 7850

Rationale of this trade- market seems to be inching higher despite the headwinds so we could do very well here and the downside risk is maximum of our cost= 9.

2 weeks ago: 99 minus 37×2= 25

Now….it’s 21

Those premiums now 22 and 3.5×2 it’s still in profit but are we convinced? We run of course to expiry

264 Is the Downside Already Being Overstated?

Arguably the top is in-and the worst thing one can do is make a prediction! Hey let’s just take a view and protect the upside by revisiting our old friend the Jade Lizard. It gives a fair bit of downside risk protection, and it’s rock solid to the upside.

Sell : 7600 call 74.5 buy: 7650call 54 gives us 20.5 and sell 7075 put 30.5 Total credit 51

So we have risk at 7025 but no upside risk as our premium = the value of the spread.(OK we get 1 !)

Remember we don’t include commissions as these are pure demonstration trades. We have no interest in bragging rights.

Was 66!

Now 12.5-7= 5.5 for the call spread, and 13.5 for the put = 19 CLOSE OUT– run for fun

265 Double Down, Twice The Fun

So while this may merit some criticism, the logic of the trade and reasons therein have not changed. So we go in again

7600 call 35.5 7650 23.5 7075 put 44 Gave us 66, now as above it’s 19 CLOSE OUT! We take 44 and reduce risk going into expiry

Alternatively(and alongside for fun) we could also try 7500 call 70.5 7550 call 51 and 6950 put 30 = 49.5 Now ( 36.5-22=14.5 and 7.5) =22.

266 Calendar Ratio? Expiry on 20th

Hard to resist given the track record. so, we sell 3x May 7200 puts and buy 1 Jun 7200 put. Thus we have 25.5×3 credit and our cost 117 for jun put. We pay 41.5 and watch this like a hawk. Risk is big theta is huge-would you take this on?