That Was The Week What The Actual *************????

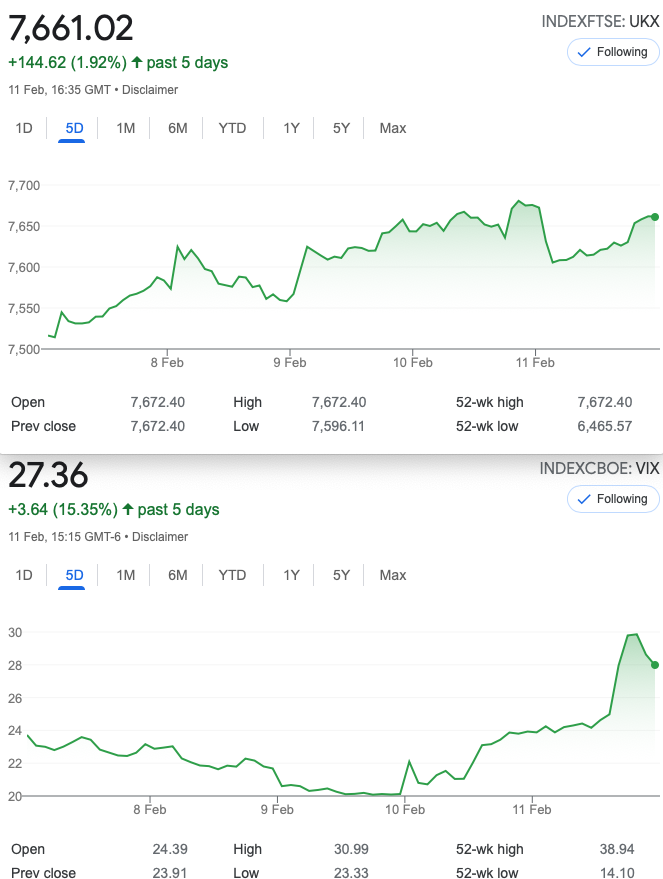

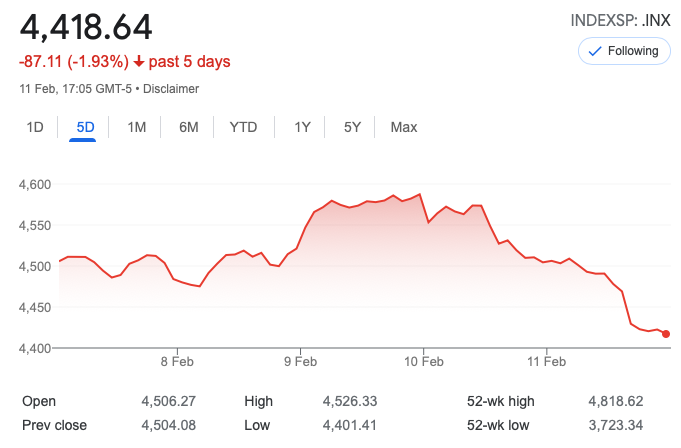

And for comparison here’s the US:

Whilst admittedly I tend towards oversimplification this is really out of wack. See this link for an explanation and long term correlation.

https://www.hl.co.uk/news/articles/archive/how-different-are-the-s-and-p-500-and-ftse-100

We have seen outrageous prices for oil and gas. Petrol, in old money is now ± £6.70 per gallon -so some of those gas guzzlers are costing north of 60p per mile. Whilst I may seem to be a stuck record there is a real disconnect, as inflation is not wage driven, yet prices are soaring. Now even pasta is in the firing line for big inflation. Costs have risen and the end user must pay. However those already enriched due to Covid are unlikely to be concerned that their tagliatelle costs 50% more.

Conflict may be on the cards for no clear reason, but was it ever thus? Our tiny world of options is the tail that is, at times, wagged by the dog. Let’s hope our positions are manageable.

Distraction Trades

ADA Cardano was $1.1550 now $1.0630

XRPUSD $0.77657 BUT…. it was $0.675

So Ripple is feeling the love as our Cardano limps along -who knows the future for Crypto’s?

DAX – a really good week 3 trades 100+ 2 no entries. (note last week saw 2 monster wins, 3 no entries)

Note: the DAX entry method is rarely 100% clear there is always a bit of discretion and the need for sharp reactions. Arguably this could be automated and I’d love to see that algo. I would therefore contend that the market has a ‘character’ and this cannot be quantified. You simply have to bash through the lean times unless you have super smart software that can recognise those intra day changes. Happy to pay ££££ for such a beast with 1,000 trades realistically backtested.

Legacy Trades 251,252,253 and now 254

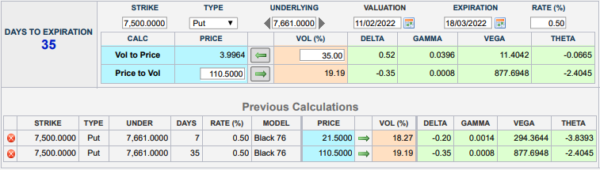

So, we traded with the market’s money and used the Feb 7300 put that we own. Simple choice- the market may take a tumble on Monday based on the futures close, so we could wait, but lets do a put ratio spread at 7500(long) 7400 shortx2

Thus we have the following prices: 137 and 100.5×2. We are now the proud owners of a butterfly. We are bulletproof. Our credit on this trade is 64. We could have sold the 7300 put for 74.(We still bank 64 and buy a pizza!) However this way we could make another 100

2nd to last week: the butterfly was worth only 10 but we run of course to expiry.

Last week: 13– but that is the way with ‘flies until the day before expiry really.

Ugh- now 4.5 ‘Squeaky bum time’ to quote

252 a game of forks- we used March expiry

Hopefully you can see puts and calls at the 7150 strike for March expiry, whereby we sell the call and 3xputs at the same strike roughly below the index minus the straddle- but with some wiggle room. We like have roughly level premium either side 382 for the call and 122×3 (366) for the puts.

We can use the premium to do something interesting too -we take in a whopping 748.

Now? 644– but on Tuesday it was 652. Either way- we’d take a profit of ± 100. In %age terms this is not huge compared to margin required but it is a peach of a trade again. WIN!

496.5 and 46×3= 534.5 WIN MORE! OK- exit or what?

253 Vol has shrunk- what’s to do?

Oh dear- what a quote!

It may be that given the mild moves we’ve seen, that vol is shrinking and the market going nowhere- just an opinion, but what’s to do? It’s a double ratio, buying the straddle and then we ratio the wings of a short iron butterfly. Say WHAAAT??

We bought the 7500 straddle and sell the wingsx2( 7600 calls and 7350 puts ) February prices

Note those prices – we pay 91.5 for the 7500 call and take in 44×2= 88 for selling 2x 7600 calls = 3.5

And the puts -we pay 98 for the 7500 and take in 50.5×2 for selling the 7350 puts = Credit 3.

We have risk at 7200 and 7700 but probably going to make more than the cost of 0.5

175, and 21.5 (196.5) for the straddle: the strangle: 95.5×2 and 9×2. = 209 Small loss currently

254 Normally We’d Look for A Calendar Spread

Front month prices are stupid low on the put side, otherwise we’d look at a put ratio calendar spread

OK- this is nuts but let’s have a play – we BUY 5 Feb 7500 puts 5x 21.5 and sell 1 March 7500 put 110.5 (110.5-107.5)= 3 This trade is known as a backspread and whilst they can bite us bigly, they can be rewarding short term. Price Headley(check him out) is a proponent of this trade, when it makes sense. But does it?

The eagle-eyed among you will spot those deltas and gammas, multiplied by 5. Vega -hugely on our side if we’re right. What if we hang around waiting for a drop? Theta is beyond ugly. Theta is ‘Coyote Ugly’ (look it up!)

So we need this puppy to make coin on Monday. Of course Mr Biden may be able to placate his Russian counterpart, and the market may be off to the Moon again. That would be painful but not ‘blowing up’ painful but we don’t like to feed the beast that bites us.

This morning Trade 254- long 5x Feb 7500 puts short 1x Mar 7500 put did this:

5 x84, 1×195. While the Mar Put doubled our Feb puts quadrupled.

Profit 225, minus the cost, 3. Gives us 222. That’s £2,222 for one round turn of this puppy.