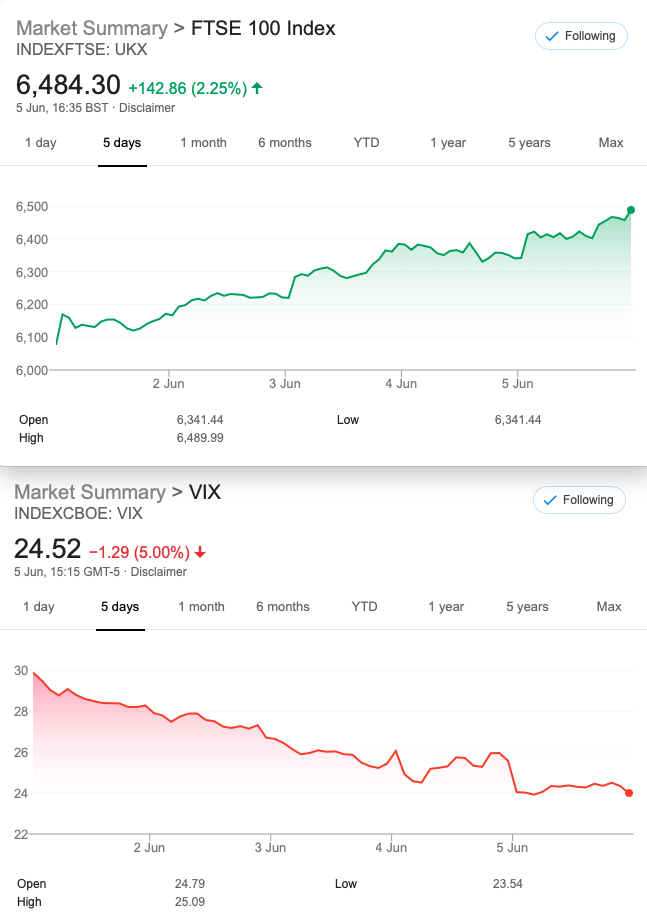

That Was The Week – Record Weekly Rise -Almost

Since 2009, this numptie has found 4 other weekly rises of >5%. The biggest we found, November 2011 +7.51%. Much of our trading is predicated on a sideways markets, which is what happens most of the time. Since May 15 low of 5741 we see a rise of 13%….. in 14 trading days. Is this ‘irrational exuberance’ misplaced? We saw commodites rise, sterling rose, gold dropped so in part this makes sense. Personally I would like to see a bit of downside, but hope is not a strategy!

I’ll continue the theme of stats here out of curiosity, since Jan 2010 the market has risen 19.79% . Buy-and -holders have thus not seen a great return, absent dividends. However the 10yr average is 6500 just about where we are now.

Being On The Ball

Sometimes it’s hard to make any kind of sense and it’s with regret that this trader dipped toes in the market even with an almighty cushion of being 12% out-of-the -money. So, for us retail traders when’s the best time? Observers of events of today that are playing out with no fixed end, will gain no insights, it seems. We have no sense of normality. However, we saw the UK government, for the first time ever, sold bonds with a negative yield. https://www.cityam.com/uk-sells-bond-with-negative-yield-for-first-time-ever/ Capital will of course have to be repaid but such lending seems unreal. Central banks shall we say, created too much money chasing too few opportunities? Foodbanks and other noble causes may disagree.

Dodgy Random Trades

Glencore: 160/170 July call spread 6.5-3.5=3 Now 7.5 though the naked 160 call now 24.5 The stock up >20%

BP 320/330 July call spread 11-7.25=3.75 Now 47.25-39 =8.5 naked call now 47.25 The stock up 18.48%

Let’s not pretend this is anything more than random stock picking in one of the biggest rises in FTSE history. Robin Hood traders must be delirious with joy.

Legacy Trades and 174

Trade 171

We sold the 5800 straddle(put & call) and BOUGHT the outer wings, the 5650put and 5950call. Horrible -now 144 on the call side and 3 on the puts -sold for total 134. Loser but don’t think we need worry about the puts,so we’d take a hit of 10

Trade 172

We sold near month June 5600 put, buying July 5600 put but… we also sold the July 5100 put. Debit 113.5-(49+58.5)= 6. Last week the Jun 5600 put was 42, July 5600 put 96.5, the 5100 put was 40. So the spread was worth 56.5, our liability for the Jun put was 42, so we had a credit of 14.5, but…we paid 6. We get 8.5! We run this. Now 9.5 -ugh!

Trade 173

We went deeper with 5800 jun/july put calendar, and again selling 500 points below: the 5300 July put. The numbers thus: 139-56.5 for July spread= 82.5, minus the short Jun put at 71. This was a cheeky 11.5 debit. Now 14.5 -double ugh!

Trade174

Theta play- ‘something for the weekend’ lazy strangle- selling both the 6400 put 83.5 and the 6550 call also 83.5.

Why???? Some years ago another options trader suggested that theta works its magic over the weekend. Let’s see!