When You Need Some Levity

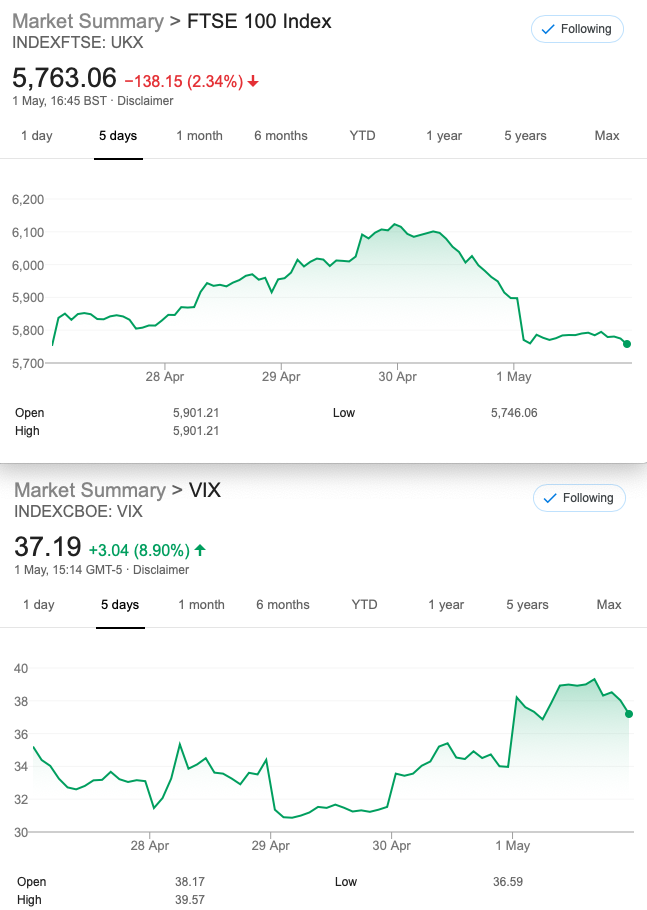

I was hoping to find a clown car image to sum up this week’s market activity. The ‘clown car’ concept comes from the illusion that 1 clown gets in and about 15 clowns get out. So we have clown car financing. The funny money. The IOU our grandkids don’t need, and didn’t ask for. Swinging from 5728-6151 gives us actually a 7% range. Even dafter. However, rumour of Gilead’s miracle cure seemed to have fuelled this nonsense, though they manage a straight face when they tell us the stockmarket looks forward 12-18 months. So while these moves are typical bullmarket irrationality, they can be traded. However we deem the market too crazy as yet. And it’s far from over.

Trading This Much Madness? How?

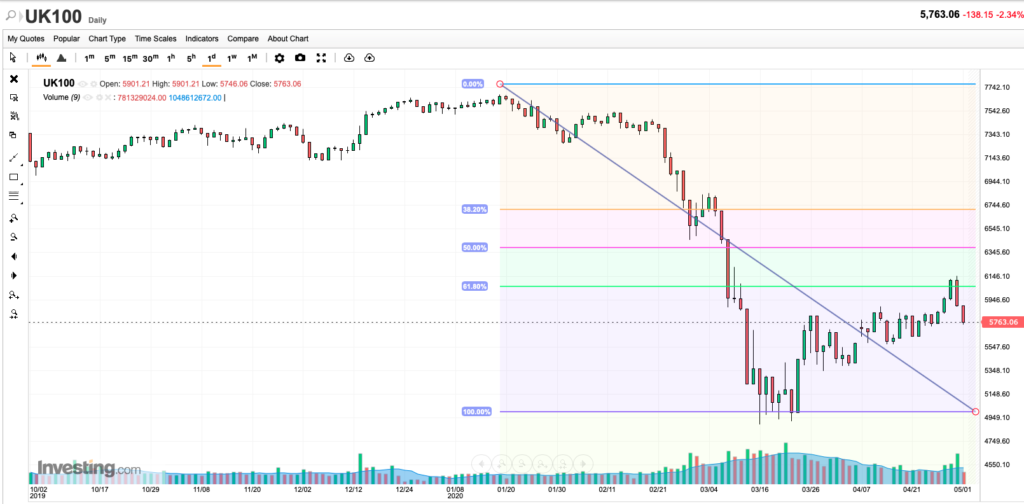

Did we mention a key resistance level ? So, this seemed to be around 5840 but once this was breached, this idiot had no answers. Until this trader’s memory jogged back to the days of pivots and Fib levels. We reckon the 61.8% level as the most powerful, and sure enough the FTSE turned and came back to reality. So 20:20 vision with hindsight etc, and I’ll admit I was late to the party, having no ‘skin in the game’ currently. So, this was a gift to the chartists, the TA hawks. And well done to any who captured any part of the move.

Legacy Lunacy

Trade 0.6 The 3×1 call ratio spread. 5800 184.5 6000 (96 x3)= 288. Credit 103.5

Could have closed out for 56 on Tuesday or hung on for: 142, – (62×3)= 44. So we had a credit of 103.5-44=59.5. We’d have taken Tuesday’s 56 credit.

Friday morning this was…. 118 and 38×3= Credit 4 Giving us a monster 107.5 Reward. Wanna hang on for more? 102- (31.5×3)=7.5 at close of play. Can we do even better? BIIIIG WIN

Trade 0.7

Thus 3 weeks to expiry put us in the ‘grey zone’ which was a pain.

FTSE 5752

![]()

We went nuts with risk and sold the ATM call and put- a straddle. 168.5+180.5= 349 credit.

Then……. 289 to close? WIN Well, that looked peachy as the market went nuts and came back to value this at about 300. Bear in mind the call side went to 400

However, we will run these to expiry for fun.(Remember we are not in the market due to the random nature of the exogenous events)

Trade 0.8

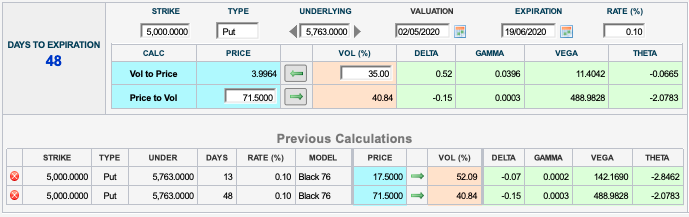

All hail the return of the BS (Black- Scholes) Calculator- it works on Google but not on Safari brower. CME’s response is awaited, but Safari is probably at fault.

Hope the image is clear. After the success of our call 3×1, we are doing a calendar ratio selling 3 May 5000 puts and buying 1 June 5000 put 71.5-(17.5×3). You do the maths*- theta is great but Vega? So, remember those May puts can only go to zero, but could come back to bite us

*Debit 19 –I’m a really soft touch aren’t I? Theta = 2.8462 x3- 2.0783= 6.46 Yuge, Bigly.

And finally- never ever accept that this was sarcasm and please retweet, copy to every corner of the ‘net. We need this!

https://twitter.com/sarahcpr/status/1253474772702429189?s=20

Debit 19 -close out for 30 -it’s that easy. Every week.

May 5000 put 13×3= 39 Jun 5000 put=69.