To explain if anyone is not familiar with this concept.

A calendar or time spread

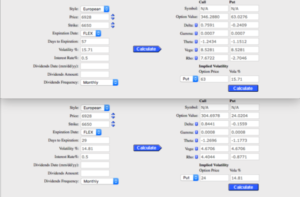

is a method of trading options that takes advantage of the increased time decay of the front, or near month. In this case the October Put, by selling it for 24, and buying the far month, the November put for 63, so this trade cost 39. Why would you do it? Because you think that the market might drop, but stay around 6650(the strike price)* in the next few weeks. Assume on 21st October the market is at 6650- the near month put that you have sold expires for 0,and the November options might be worth 120- pure speculation. You could lose a maximum of 39, if the market smashes up, and November put goes to nothing. The market could crash to 6300, and you might break even-it’s just an idea and to be honest not one of my favourites. The flexibility in these, allows all sorts of adjustments,and ways to lock in a break even or a profit.

We will monitor this one-but I don’t like it and the prices are, for me, a bit ugly. I would expect to trade this nearer the expiry on 21st October when theta(time decay) is much higher for the sold put. In the above calculations there is not much in it -see theta -1.1773 for the October put,and -1.1512 for the November, but I have other concerns about this trade that are more complicated. I should add that I rarely like to pay for an options trade- I usually take in a credit. In time we hope to make the options calculations more understandable, as these are,by necessity, far removed from typical shares analysis and balance sheets.

Options pricing is fiendishly complex

fortunately we don’t have to do the maths, we have ….

It takes a bit of understanding and we will walk through a calculation at some point.

*Strike price= the price at which an options buyer can buy/sell, or an options seller has to buy/sell at. As PUTs confer the right to sell, if FTSE =6600 at expiry, and the strike price is 6650, this PUT option is worth 50. In our case the put option is sold so if FTSE = 6600 at expiry,the short option is negative 50,in other words,we have to buy it back. But….. you own the November PUT which is now worth 170….. Happy Days you just made 300%. Remember a CALL is the right to buy, a PUT is the right to sell, and you can not only buy these, but sell them too. So, a sold call means you sold the right to someone else to buy at that price- say you sold a CALL with strike price of 6600 and FTSE now is 6650, you must buy the FTSE at 6650-6600=50 minus whatever you sold it for.

It will become second nature, in time,but it’s not a conversation to have after a few pints at the pub.

Curiously as this trade has gained from today’s movement and in light of recent reserach courtesy of Tasty Trade,this trade made 50-so if you had closed out you would have made the expected 25% return.

Thus- a trade I don’t like has shown that when the profit is there for the taking, grab it with both hands. This trade may go on to make 100, but over time these only have alimited success rate so you might be happy with 25%.

This trade is now worth about 35-so taking that 25% profit was a smart move-we’ll keep an eye on this until expiry